Understanding Laser Tattoo Removal and Why More People Are Choosing It

Other |

2026-06-03 08:27:32

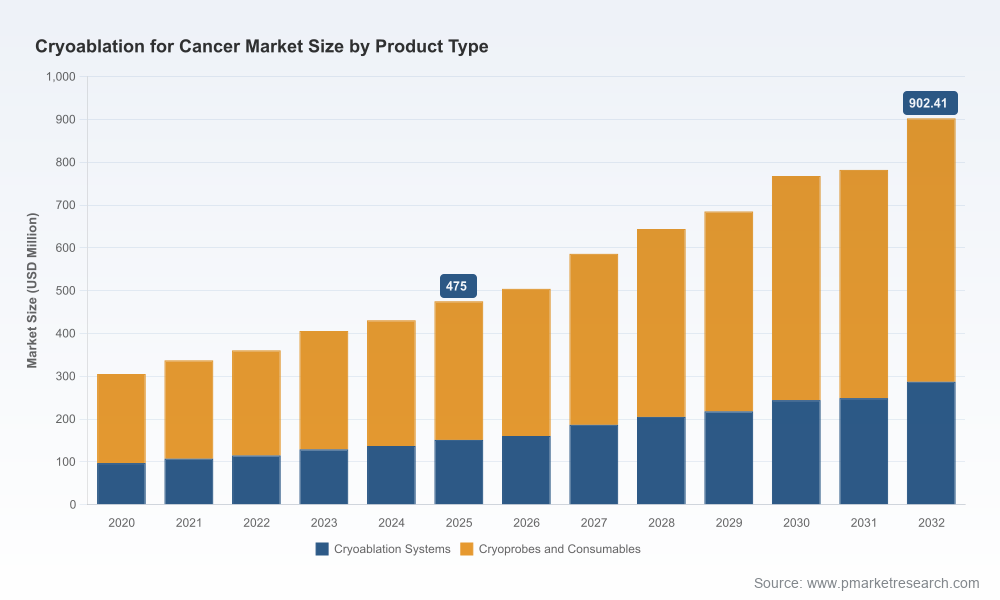

PW Consulting’s new market study on Cryoablation For Cancer offers a focused, practice-oriented briefing designed to inform boardrooms, corporate development teams, health-system strategy groups and investors planning moves in 2026. The global market reached approximately USD 475 million in our 2025 base year and—supported by sustained clinical adoption, coding momentum and capital investment—is modeled to grow at a 9.42% compound annual growth rate through the 2026–2032 forecast period, reaching roughly USD 902 million by 2032. This release is a strategic “trailer”: it surfaces the signals and strategic implications you need to act in 2026 while deliberately withholding the full, granular segment tables to drive readers to the full report for executable numbers and supplier-by-supplier detail.

Cryoablation For Cancer Market

Fast-moving evidence and regulatory events are realigning the clinical pathway for cryoablation—raising questions about which indications will become commercially meaningful in the next 24 months.

Cryoablation For Cancer Market

Reimbursement and coding updates are creating immediate revenue pathways for early adopters, but they require proactive payer strategy and clinical program design to capture value.

Cryoablation For Cancer Market

Capital intensity, combined with a concentrated competitive landscape, means procurement and partnership choices made today will determine who captures durable share as the market scales.

Evidence and guideline momentum: Recent regulatory and guideline developments (including a 2025 De Novo marketing authorization for a liquid‑nitrogen cryoablation system and a March 2026 guideline update recommending cryoablation as an option for selected patients with biologically low‑risk early‑stage breast cancer) materially change the adoption calculus for certain outpatient and ASCs-focused clinical pathways.

Reimbursement architecture: New CPT and HCPCS coding activity has begun to create clearer facility-level reimbursement for selected procedures. For example, certain post‑procedural pathways tied to cryoablation have an approximate facility fee in the low single‑thousands (as published for a recent low‑risk breast cancer pathway), and interventional probes are recognized under HCPCS coding that allows inclusion in ablation procedure payments—both of which affect provider economics and case mix decisions.

Capital and operating economics: Leading cryoablation platforms are capital purchases with material upfront costs; advanced units fall in the mid‑six‑figure range and require careful disposable‑and‑maintenance modeling. At the same time, hospital capital expenditure pressures are high—facilities reported elevated CapEx-to-depreciation ratios in FY24—making flexible financing, rental, and service models commercially important.

Competitive concentration and route to scale: The market exhibits a high degree of concentration among a few large medtech incumbents and specialist device innovators, creating both barriers and acquisition opportunities for entrants. Our concentration analysis shows the top vendors control a substantial share of commercial activity, reinforcing the importance of partner selection or niche specialization.

Technology differentiation: MRI‑visible systems, multi‑needle platforms, and liquid‑nitrogen versus cryogen gases remain key product differentiators. The clinical and workflow implications of imaging integration and probe architecture are core variables in procurement decisions.

Proprietary market model (2020–2032) with scenario runs—base, conservative and accelerated—allowing you to stress test price, reimbursement and adoption curves. The model is delivered in an interactive workbook so you can plug in your own assumptions.

Buyers’ playbook for 2026 procurement: Capital vs subscription analysis, disposable and maintenance line‑item templates, clinical throughput case studies and hospital ROI calculators.

Reimbursement roadmap: Coding timelines, payer engagement templates, and a revenue capture planner tied to CPT/HCPCS pathways plus shortlists for coding advocacy priorities.

Competitive benchmarking and supplier scorecards: Strategy, go‑to‑market strengths, clinical evidence base, regulatory status and partnership suitability (note: supplier scores and selective financial proxies are in the full report).

Clinical evidence and regulatory tracker: Ongoing and upcoming trials, delta analysis of pivotal endpoints, and regulatory milestones that will de‑risk commercialization programs.

M&A and partnership playbook: Valuation frameworks tailored to cryo devices, probes/consumables and service providers; integration risk checklists and 12‑month playbooks for roll‑ups and strategic alliances.

Go‑to‑market playbooks for incumbents, innovators and ASCs—covering direct sales, distributor models, and integrated service contracts.

Primary research appendix: Interview notes from payers, procurement executives, interventional radiologists and surgical oncologists that informed adoption curves and clinical pathway assumptions.

Large medtech incumbents (global platforms): Companies with broad portfolios bring distribution scale, purchasing relationships and capital muscle. Their strategic play is to integrate cryo into existing oncology and surgical device franchises, pursue imaging integration and offer bundled capital + disposable contracts that make adoption administratively simple for health systems.

Specialist innovators: Smaller firms have concentrated clinical evidence and regulatory wins in niche indications and often use single‑indication reimbursement wins to gain a beachhead. Recent regulatory clearance and planned post‑market trials demonstrate a pathway from niche authorization to broader label expansion—worthy of close competitive monitoring.

Regional distributors and service providers: These players are attractive acquisition targets for both scaling consumables and gaining local customer intimacy—especially in geographies where direct sales are inefficient.

Strategic interplay: Expect intensified M&A and licensing activity around probes and consumable platforms, given the consumables’ recurring revenue profile and lower implementation friction versus capital equipment.

Regulatory and guideline momentum: The combination of a 2025 marketing authorization for a liquid‑nitrogen system focused on a narrow breast‑cancer population, a March 2026 guideline update recommending cryoablation as an option in selected low‑risk early breast cancer, and an FDA‑cleared post‑marketing study design scheduled to enroll across multiple U.S. sites creates a near‑term evidence window that will define the next wave of adoption.

Reimbursement and coding: Early facility reimbursement and established HCPCS coding for probes change the provider economics equation; aggressive payor playbooks and outcomes collection will accelerate coverage expansion if real‑world performance matches trial endpoints.

For global incumbents: Prioritize service‑led commercial models and accelerate evidence generation in comparative effectiveness—leave little room for niche innovators to define clinical standards in high‑value settings.

For challengers and device innovators: Target fast‑path indications with clear coding/reimbursement, design pragmatic trials that support outpatient adoption, and pursue distributor partnerships to bridge the sales footprint gap.

For health systems and ASCs: Use the report’s ROI templates to evaluate lease vs buy and to model case-mix uplift tied to minimally invasive oncology services; negotiate bundled pricing that ties disposables to utilization guarantees.

For investors and PE sponsors: Look for roll‑up opportunities in probes/consumables and service providers; value creation will come from combining clinical scale with centralized consumables procurement and aftermarket services.

Use this briefing to set a 90‑day listening agenda (stakeholder interviews, proof‑of‑concept site selection, and reimbursement advocacy steps).

Purchase the full report to access the interactive forecasting model, granular segmentation and geography tables, supplier scorecards, and downloadable procurement templates—these are intentionally withheld here to preserve the report’s commercial utility.

PW Consulting’s Cryoablation For Cancer Market study is built to convert market intelligence into boardroom action. If you are evaluating product investment, partnership, or acquisition choices in 2026, this report provides the model inputs, evidence map and go‑to‑market playbooks you need to move from hypothesis to execution. Visit PW Consulting’s report page to access the full dataset, interactive model and supplier appendices.

For detailed analysis of this topic, please visit the official page:Cryoablation For Cancer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com