Elevating Safety Standards: A Practical Guide to Work at Height Permits

Other |

2026-04-16 07:28:49

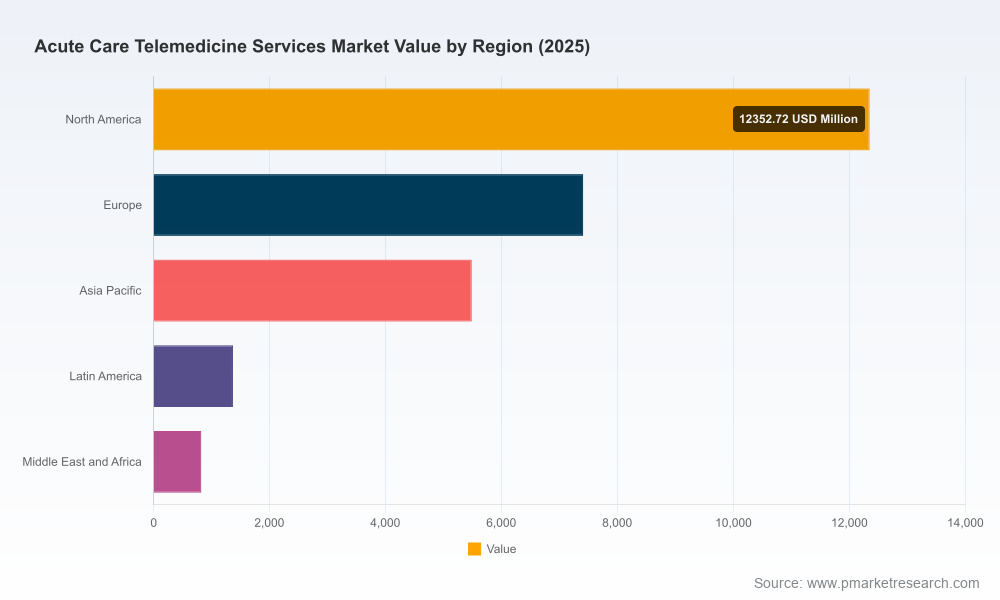

PW Consulting’s new market study on Acute Care Telemedicine Services (base year 2025; historical analysis 2020–2025; forecast 2026–2032) delivers a data-driven strategic toolkit designed for health system executives, digital health investors, and policy makers preparing decisions in 2026. The market is on an accelerated trajectory, expanding from its mid‑2020s scale into a multi‑decade growth runway. Our modeled baseline indicates a robust compound annual growth rate (CAGR) of 14.82% across the 2026–2032 forecast window, with the global market moving from the 2025 baseline into a substantially larger revenue pool by 2032. This briefing highlights the report’s strategic value while preserving the full granularity for subscribers to the complete study.

Acute Care Telemedicine Services Market

Timing and momentum: As acute care telemedicine matures from episodic pilots into hospital‑wide programs, 2026 will be a pivot year where early adopters scale, and laggards decide between build, partner, or buy. Our analysis quantifies where operating leverage and clinical ROI begin to crystallize across typical deployment horizons.

Acute Care Telemedicine Services Market

Investment clarity: Investors evaluating platform companies, command‑center operators, or clinical service providers need realistic revenue and margin expectations grounded in adoption curves and reimbursement scenarios. The report aligns bottom‑line modeling with regulatory and labor cost assumptions most relevant to 2026 capital allocation.

Acute Care Telemedicine Services Market

Operational playbooks: Hospital systems and regional networks require actionable roadmaps — from clinical workflows to technology architecture and procurement specifications — that reduce time to break‑even. Our deliverables translate market signals into operational levers with estimated payback ranges and risk buffers.

Using a 2025 base and a seven‑year forecast horizon (2026–2032), our model projects sustained double‑digit growth at a 14.82% CAGR. Practically, this means the acute care telemedicine ecosystem will expand rapidly in absolute terms and in complexity: more service models, diverse delivery architectures, and increasing vendor density across clinical domains such as neurology, critical care, emergency medicine, and behavioral health.

For strategic planning, that growth profile implies three near‑term realities: (1) first‑mover scale advantages for organizations that aggregate demand across multiple facilities; (2) premium pricing windows for high‑acuity clinical services where clinician scarcity is acute; and (3) an intensifying competitive landscape where differentiation shifts from basic connectivity to clinical outcomes, integration depth, and service guarantees.

The acute care telemedicine field is populated by specialist service operators, clinical networks, and digital platform vendors. Key incumbents in our coverage universe include Access TeleCare, Eagle Telemedicine, Avera eCare, Teladoc Health (InTouch Health), Amwell (Converge), and Sound Physicians. Each represents a different strategic archetype:

Access TeleCare (Dallas) emphasizes specialty breadth and 24/7 acute coverage across neurology, psychiatry, critical care, hospital medicine, and ED support — a multi‑specialty operator model that targets integrated hospital contracts.

Eagle Telemedicine (Leawood) focuses on hospitalist and intensivist services tailored to rural and critical access hospitals, highlighting the cost‑effectiveness play in underserved geographies.

Avera eCare (Sioux Falls) operates at large scale, offering command‑center oversight and extensive inpatient coordination across hundreds of facilities — an exemplar of centralized clinical operations delivering system‑level throughput benefits.

Teladoc Health and Amwell combine platform capabilities with clinical services, enabling system integrators to bundle tele‑ICU, tele‑stroke, and ED physician support with enterprise‑grade platforms and third‑party integrations.

Sound Physicians integrates tele‑hospitalist and tele‑ICU into broader acute management programs, demonstrating the hybrid model of onsite clinician networks plus virtual augmentation.

Recent corporate moves underscore the competitive dynamics. For example, Access TeleCare’s rebranding signaled broader specialty ambitions, Eagle Telemedicine’s regional expansion reflects a strategy of deepening market penetration in defined geographies, and Avera eCare’s new partnerships highlight collaboration as the fast path to rural scale. Across the market, we observe consolidation tendencies alongside targeted partnerships between platform vendors and clinical operators.

The sector shows moderate concentration at the top, with leading firms holding meaningful but not dominant shares of the market. This structure fosters differentiated competition: national platform vendors strive for enterprise contracts and interoperability wins, while regional clinical operators emphasize bespoke service levels and local reimbursement navigation. For buyers, this mix creates opportunities to combine best‑in‑class technology with locally trusted clinical partners.

Reimbursement: Policy clarity around parity for select acute telemedicine services has materially reduced commercial uncertainty. Recent CMS provisions have supported reimbursement parity for certain acute care codes through the near term, but the permanence and scope of those policies remain a core sensitivity for 2026 planning.

Licensure and interstate practice: Interstate delivery requires either state‑by‑state licensure or participation in compact arrangements. Organizations planning cross‑state scale must budget for licensure complexity and lead times tied to credentialing workflows.

Technical standards and clinical quality: Platforms must meet minimum bandwidth, video resolution, and data‑security standards to support acute decision‑making. Clinical governance — including accreditation by The Joint Commission for telehealth programs delivering acute services — is increasingly a procurement prerequisite.

Labor cost pressure: Specialist shortages, especially in rural markets, are pushing staffing cost inflation in the range identified by federal workforce reports. This trend elevates the value of efficient scheduling, cross‑coverage models, and skills mix optimization embedded in telemedicine staffing plans.

To support rapid, confidence‑based decision making in 2026, our full report includes the following operational modules (high‑level summary here; subscribers receive detailed templates and models):

Market sizing and scenario models: Baseline and sensitivity scenarios reflecting alternative reimbursement regimes, licensure harmonization timelines, and adoption speed across hospital types.

Go‑to‑market roadmaps: Provider and vendor GTM playbooks for enterprise sales, channel partnerships, and rural deployment strategies — including contract templates and expected KPIs across implementation phases.

Technology and integration checklists: Procurement specifications for platforms, interoperability requirements with EHRs, security and compliance criteria, and operational SLAs tied to clinical outcome measures.

Clinical integration playbooks: Protocols for tele‑ICU, tele‑stroke, tele‑ED, and tele‑behavioral health workflows; training curricula; and staffing rosters optimized for 24/7 coverage.

Vendor due diligence frameworks and scorecards: Comparative assessment across technology, clinical capability, scale, business model, and contractual risk — designed to shorten vendor selection cycles.

M&A and partnership pipeline: Identification of acquisition targets and partnership archetypes, with deal economics models and integration risk matrices tailored to buyers looking to accelerate scale.

ROI and business case templates: Facility‑level and system‑level models that map clinical throughput, avoided transfers, length‑of‑stay impacts, and net financial returns under multiple adoption assumptions.

Policy reversal or reimbursement contraction that reduces per‑encounter economics for high‑acuity remote services.

Slow interstate licensure reform delaying cross‑jurisdiction scale and increasing operational friction.

Persistent clinician shortages pushing labor costs above modeled levels, compressing margins unless offset by automation or task reallocation.

Fragmented integration between telemedicine platforms and hospital EHRs leading to clinician workflow friction and suboptimal adoption.

We have seen three primary use cases emerge from early access clients:

Systems executing rapid scale: Large health systems use the report’s implementation playbooks and ROI templates to justify capital allocations and to structure enterprise‑wide telemedicine contracts in 2026.

Vendors refining product roadmaps: Platform and clinical service vendors apply the competitive scorecards and technical checklists to prioritize integrations and to align product‑market fit with buyer procurement priorities.

Investors and M&A teams stress‑testing deals: Private equity and corporate development teams use scenario models to stress‑test valuations under alternative policy and labor cost assumptions before deploying dry powder.

This press briefing has highlighted the strategic contours of a market poised for accelerated growth and operational complexity. PW Consulting’s full Acute Care Telemedicine Services Market report contains the granular regional and service‑line splits, vendor scorecards, contract language examples, and downloadable financial models that executives and investors need to finalize 2026 plans. Our “teaser” approach here demonstrates the report’s tactical depth while preserving proprietary segmentation and scenario tables for licensed subscribers.

For organizations preparing strategic choices in 2026 — whether accelerating deployment, sizing investments, or structuring go‑to‑market partnerships — the full study is designed to convert market opportunity into executable programs with quantified risk controls and implementation milestones.

Contact PW Consulting to request the full report, bespoke briefings, or custom scenario runs aligned with your portfolio or system footprint. Our team stands ready to translate market momentum into decisive, measurable action.

For detailed analysis of this topic, please visit the official page:Acute Care Telemedicine Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com