Signs You Might Need a Glucose Drip at Home

Health |

2026-06-10 15:16:47

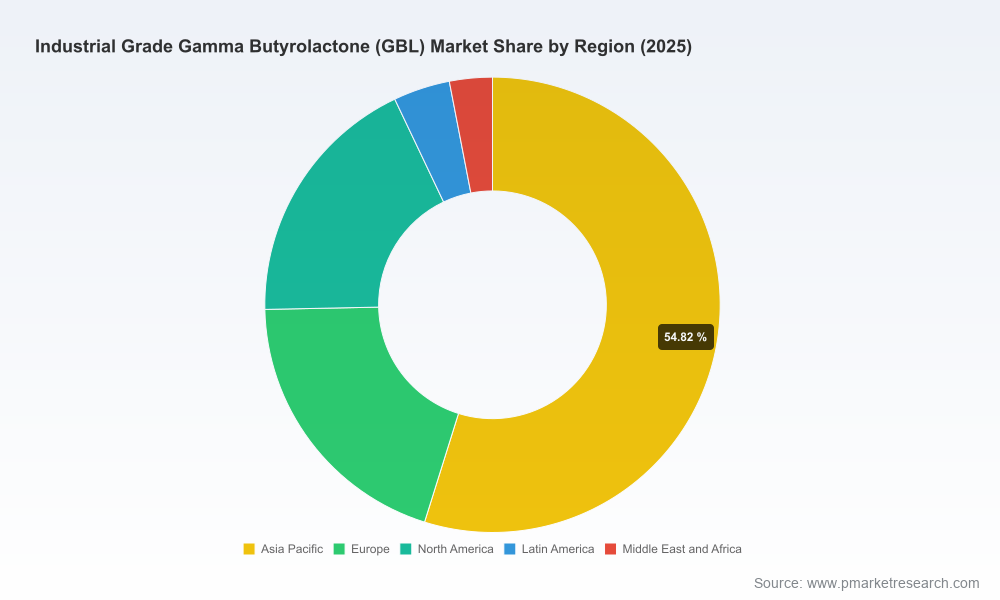

The global industrial-grade gamma-butyrolactone (GBL) market is transitioning from a commodity-style supply environment into a differentiated, risk-managed value chain that increasingly rewards scale, feedstock integration, and product stewardship. Our latest PW Consulting market study — base year 2025 — places the global market at approximately USD 4,435.2 Million and models a steady compound annual growth rate (CAGR) of 5.48% across the 2026–2032 forecast window, driving the market toward a multi-billion dollar landscape by 2032. This preview outlines why those figures matter for 2026 corporate strategy, what operational and commercial decisions they should accelerate, and how senior leaders can convert market visibility into defensible advantage without waiting for full published subsegment detail.

Industrial Grade Gamma Butyrolactone Gbl Market

Several forces combine to make 2026 a pivotal year for GBL strategy. First, the market’s macro trajectory — measured growth from the mid-2020s into the early 2030s — validates continued strategic investment in higher-purity and specialty grades that command stable margins. Second, upstream feedstock dynamics remain the single most immediate lever for cost and capacity decisions. Our analysis shows that 1,4-butanediol (BDO) prices and regional spreads are tight but stable in early 2026, reflecting limited short-term elasticity in the BDO-GBL conversion chain and the sensitivity of profit pools to modest feedstock moves.

Industrial Grade Gamma Butyrolactone Gbl Market

Regulatory and compliance pressures are also intensifying. Notable developments include targeted exemptions in China for certain formulated products containing GBL (which reshape trade and inventory handling for formulators) and enduring classification frameworks in the United States and European Union that require strict industrial controls and registration. These regulatory vectors create both barriers and opportunities: they raise the cost of noncompliant supply while enhancing the relative value of proven, audited suppliers with traceable stewardship programs.

Industrial Grade Gamma Butyrolactone Gbl Market

The GBL market displays moderate concentration: three global leaders account for just under half of identified market throughput, and the top five approach two-thirds — a structure which creates both bargaining power and opportunity for mid-sized specialists. Leading global producers combine several strategic advantages: integrated BDO-to-GBL routes, specialty-grade production capability, and established relationships into electronics, pharmaceuticals, and advanced materials supply chains.

Representative profiles of active strategic players (report contains extended firm profiles and capability maps):

Recent corporate moves in 2024–2026 — from capacity additions to timely pricing actions and public sustainability disclosures — indicate an industry balancing incremental supply growth with disciplined commercial governance. For buyers and investors, this means near-term visibility on availability but continued upside for differentiated, audited supply chains.

Below are high-conviction calls that PW Consulting’s analysis supports for 2026 planning cycles:

Our full report is intentionally practical. Key deliverables we supply to boardrooms and commercial teams include:

We intentionally withhold granular subsegment allocations and proprietary split tables in this preview to preserve the actionable core of the report for subscribing clients. Those subsegment insights — covering regional demand, application-specific volumes, and purity-grade economics — are the parts of the study that materially change deal outcomes and procurement strategy; they are available through the full report package.

The market’s projected trajectory, combined with feedstock sensitivity and an evolving regulatory environment, creates a narrow window in 2026 to secure advantaged supply, lock in differentiated margins, and de-risk growth through disciplined contracts and compliance programs. Firms that make timely decisions on feedstock sourcing, purity-positioning, and stewardship investments will both reduce volatility and capture outsized returns as demand continues to shift toward higher-value industrial applications.

PW Consulting’s Industrial-Grade GBL Market report is designed for C-suite, strategy, procurement, and corporate development teams that need to translate chemical-market intelligence into executable moves this year. The full study includes the complete data tables, regional and application-level modeling, supplier maps, and the playbooks described above. Contact our research desk to access the full report package and request a tailored briefing for your executive team.

For detailed analysis of this topic, please visit the official page:Industrial Grade Gamma Butyrolactone Gbl Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com