Multi-Junction Gallium Arsenide (GaAs) Solar Cells Market: 2026 Strategic Outlook

Executive summary

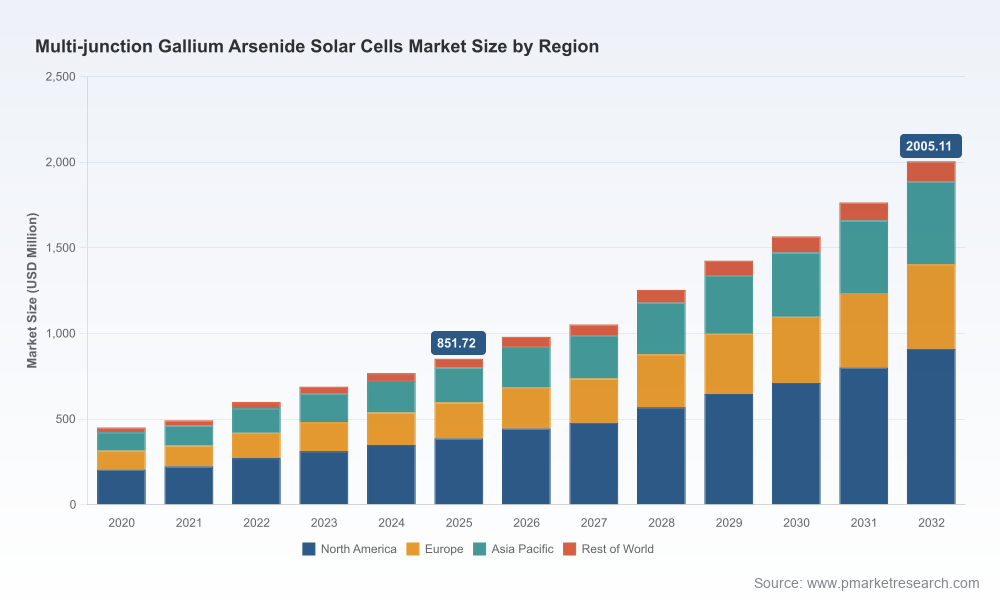

PW Consulting’s latest market study on Multi-Junction Gallium Arsenide (GaAs) Solar Cells provides a forward-looking roadmap for executive decision-makers preparing for 2026. Built on a historic baseline (2020–2025) with a 2025 base year and a seven-year forecast to 2032, the report quantifies a robust expansion pathway: the global market more than doubled from the early 2020s and is projected to continue growing at a compound annual growth rate (CAGR) of 13.01% through 2032. By 2025 the market sits in the high hundreds of millions (USD, revenue unit: Million), with the model projecting a near-doubling by 2032 under our base case scenario.

Multi Junction Gallium Arsenide Solar Cells Market

For boards, strategy teams, procurement leads and R&D chiefs, the report translates this macro momentum into pragmatic actions: where to underwrite capacity; which supplier capabilities to qualify; how to structure long‑lead procurement and inventory policies; and what technology bets to make when high-efficiency, radiation‑tolerant PV is becoming mission‑critical across space, high‑concentration terrestrial systems and advanced aerospace platforms.

Multi Junction Gallium Arsenide Solar Cells Market

Why this matters for 2026 decision cycles

- Accelerating demand vector: Growth drivers remain concentrated in satellite constellations, concentrated photovoltaic (CPV) pilots and high‑end aerospace systems. Rising launch activity and demand for higher power‑to‑mass ratios are shortening specification and procurement cycles; buyers must move from ad‑hoc single‑mission purchases to multi‑mission supplier strategies.

- Technology premium: Multi‑junction GaAs cells sustain a premium valuation where efficiency and radiation hardness directly translate to mission margin. Breakthroughs in triple‑junction and higher‑junction designs are reshaping lifecycle cost curves — requiring procurement to balance upfront cost with delivered energy and lifetime performance.

- Consolidated supplier landscape: The top tier of manufacturers controls a large share of the market, increasing counterparty risk but also simplifying strategic sourcing for qualified, flight‑proven suppliers. This concentration creates both barriers for newcomers and opportunities for focused niche entrants that can offer differentiated value (e.g., ultra‑light flexible panels, epitaxial lift‑off processes).

- Supply chain and geopolitics: Raw‑material concentration and evolving trade policy are no longer theoretical risks. Gallium unit values and concentrated upstream production make sourcing strategy and inventory planning programmatic priorities for 2026.

Report content — what PW Consulting delivers to support 2026 decisions

The full report blends proprietary market modeling with actionable toolsets designed for immediate operational use. Key components include:

Multi Junction Gallium Arsenide Solar Cells Market

- Comprehensive market sizing and scenario‑based forecasts (base case, accelerated adoption, downside constrained), including sensitivity analysis by adoption trigger (LEO constellation orders, CPV commercial pilots, UAV and specialty aerospace procurements).

- Supply‑chain mapping from wafer and substrate supply through epitaxial growth, cell fabrication (including IMM and ELO routes), assembly and panel integration — with lead‑time, capacity and bottleneck diagnostics.

- Technology deep‑dives assessing TRLs (Technology Readiness Levels), efficiency roadmaps, radiation performance profiles and mass/power tradeoffs across multi‑junction architectures.

- Supplier scorecards and a procurement playbook: vendor validation checklists, qualification timelines, contract templates (including performance‑based clauses and IP considerations), and recommended test matrices for radiation and thermal cycling.

- Raw material risk matrix: gallium sourcing scenarios, price‑shock modeling, inventory hedging strategies and circular‑materials opportunities (recovery/recycling pathways).

- Regulatory and trade scenario planning: tariff impact simulations, export control stress tests, and recommended jurisdictional strategies for manufacturing and procurement.

- M&A and partnership mapping highlighting logical combinations — from vertical integration plays to small‑cap technology acquisitions that accelerate mass‑to‑power improvement.

- An Excel‑based model delivered with the report that allows clients to run bespoke scenarios using their own input assumptions for unit demand, contract yields and price curves.

Competitive landscape — strategic profiles and implications

The market is shaped by a set of established specialist manufacturers and a handful of technically advanced newcomers. Our qualitative analysis of leading suppliers highlights three strategic archetypes:

- Flight‑proven integrators: Companies with deep heritage in space missions (extensive flight heritage, prime contractor relationships and conservative qualification processes). These players are the default choice for high‑reliability satellite programs where procurement cycles emphasize pedigree and risk minimization.

- Technology‑specialist innovators: Companies advancing novel fabrication techniques (e.g., epitaxial lift‑off, inverted metamorphic structures, thin‑film GaAs variants) that deliver improved power‑to‑mass ratios and flexible form factors — attractive for small‑sat and UAV applications.

- System‑level providers and integrators: Suppliers that offer cells alongside system‑level panels and balance‑of‑system integration, simplifying supply chains for constellation operators and terrestrial CPV module manufacturers.

Representative implications drawn from company profiles and recent R&D news:

- Spectrolab’s long flight heritage and very high AM0 efficiencies keep it as the preferred supplier for large prime contractors seeking predictable performance and certification pathways.

- European specialists with strong CPV and space relationships continue to serve regional demand and prime OEMs; partnerships with these suppliers are strategic for operators targeting European programs and civil space contracts.

- EMCORE’s recent reported efficiency milestone underscores the ongoing efficiency arms race; for procurement teams, such announcements signal when device‑level improvements will materially affect system sizing and total cost of ownership.

- MicroLink, Alta Devices and similar innovators present opportunities for integrators looking to shave grams from platform mass budgets through ELO and thin‑film architectures — but these choices often require adapted qualification pathways and longer development milestones.

- Consolidation metrics show the top three to five firms controlling a dominant share of the market; this changes competitive negotiation dynamics and elevates the strategic value of long‑term offtake agreements and co‑development partnerships.

Raw materials, policy and trade: near‑term shocks and mid‑term realignments

Two supply‑side facts underpin the 2026 risk profile. First, unit values for primary inputs rose materially in 2025, tightening margin envelopes for cell manufacturers and increasing the importance of material efficiency and recycling. Second, upstream production remains geographically concentrated, creating vulnerability to policy shifts.

Policy developments in late 2024 and 2025 — including temporary export relaxations and tariff adjustments — have created a window of pricing and sourcing volatility. In parallel, public R&D funding (notably U.S. Department of Energy initiatives) is accelerating efforts to reduce manufacturing costs and to develop alternative concentration and integration methods for III‑V photovoltaics.

Strategic responses recommended in the report for 2026 include diversified sourcing agreements, conditional inventory accumulation, material substitution pilots where feasible, and engagement with government programs to secure supportive funding and tariff carve‑outs for critical equipment.

Actionable strategies for CFOs, CTOs and procurement leaders in 2026

- Implement a two‑tier procurement strategy: secure a baseline of flight‑proven capacity with long‑lead contracts, while reserving a portion of deployment for higher‑risk, higher‑reward technologies that can materially improve energy density.

- Prioritize supplier qualification across three dimensions — performance, supply‑chain resilience and IP exposure — and price contracts to reflect lifecycle energy delivered, not just unit price.

- Invest in in‑house or partnered qualification capabilities (thermal, radiation, and mechanical testing) to shorten supplier‑validation timelines and to increase negotiating leverage.

- Build scenario models that integrate raw‑material price shocks, trade policy variations and technology substitution timelines; use these models to stress test project IRRs and procurement burn rates.

- Explore strategic partnerships or minority investments in innovative cell fabricators that bring differentiated mass or performance advantages for your mission set.

Why PW Consulting’s market study is decision‑ready for 2026

Our report is designed as an executable intelligence product — not just a forecast. It combines market‑level growth metrics, trade and raw‑material intelligence, supplier benchmarking and executable procurement templates. This is the toolset teams will use to convert the macro opportunity (a market expanding at ~13% CAGR) into defensible, risk‑aware procurement and R&D roadmaps for 2026.

In keeping with the “trailer” principle that guides our public communications, this briefing outlines the strategic contours and operational implications without disclosing the detailed segmentation tables and contract‑level metrics that form the core of the model. The full report contains proprietary breakdowns by application, region and cell architecture, supplier‑level shares, detailed cost curves and an interactive model you can use to stress test bespoke program scenarios.

Next steps

Organizations preparing budgets, procurement schedules and technology investment plans for 2026 should prioritize a rapid review of three items we cover in the full study: (1) supplier qualification and long‑lead contracting templates, (2) raw‑material exposure and inventory policy options, and (3) targeted technology pilots that balance risk and mission payoff. Access to the complete dataset and modeling workbook will enable teams to convert market forecasts into executable 2026 commitments with quantified upside and downside cases.

To obtain the full Multi Junction Gallium Arsenide Solar Cells Market report — including the detailed segmentation, supplier scorecards and the Excel scenario model — please visit the PW Consulting report page or contact your PW Consulting account representative. The granular insights and tools within the report are specifically tailored to inform 2026 capital allocation, procurement and technology roadmaps.

For detailed analysis of this topic, please visit the official page:Multi Junction Gallium Arsenide Solar Cells Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com