Lithium Salts Market Forecast by Grade, Application, and Region

Health |

2026-06-01 11:02:44

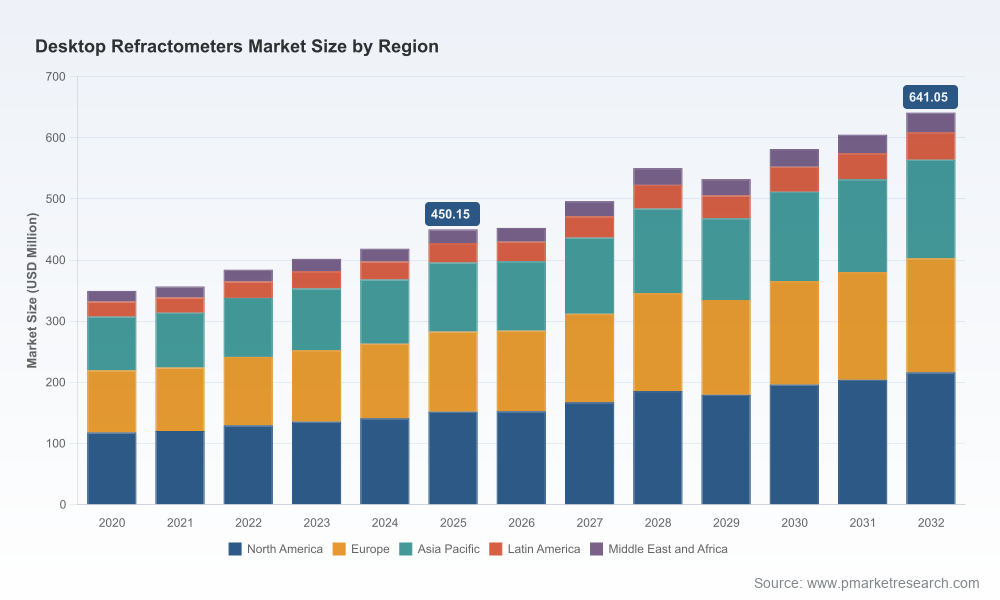

PW Consulting’s new market research preview on Desktop Refractometers synthesizes five years of historical patterns (2020–2025) with a forward-looking forecast horizon (2026–2032) to deliver a concise, decision-ready narrative for executives preparing plans for 2026. The global market reached approximately USD 450.2 Million in our base year (2025) and is projected to expand at a compound annual growth rate (CAGR) of 5.18% through the forecast horizon, reflecting steady demand driven by clinical, pharmaceutical, food & beverage, and industrial quality-control applications. This briefing outlines the strategic implications of that trajectory, highlights competitive pivots we see shaping the sector, and describes the types of operational intelligence contained in the full report—while intentionally withholding detailed breakdowns to preserve the value of the paid dataset.

Desktop Refractometers Market

Timing of capital allocation: With mid-single-digit CAGR and model-year volatility across 2026–2032, capital planning should prioritize modular investments (scale-up of digital platforms, retrofit service capabilities) over large single-line equipment bets.

Desktop Refractometers Market

Product roadmaps and compliance windows: Clinical and laboratory buyers are increasingly driven by regulatory compliance and integration readiness (laboratory information systems, calibration traceability). Meeting ISO 15189:2022 expectations and aligning product firmware and documentation to lab accreditation cycles will accelerate procurement conversion.

Desktop Refractometers Market

Go-to-market elasticity: The desktop refractometer purchase decision remains sensitive to service network density and software integration. Vendors that package device+analytics+maintenance will capture higher lifetime value than product-only sellers.

M&A and partnership signals: Moderate market concentration—where the three largest players account for a meaningful share of revenue and the top five account for more than half—creates attractive pockets for consolidation, tuck-ins, and distribution partnerships that can scale installed-base services quickly.

Regulatory alignment and lab accreditation: Desktop refractometers intended for clinical settings must fit within evolving quality frameworks; ISO 15189:2022 has become a gating factor for purchasing at hospital networks and accredited labs. Vendors that pre-certify their devices and provide compliant documentation gain preferential procurement access.

Reimbursement and clinical workflow: In some healthcare settings, refractometry is embedded within reimbursable test codes, which affects buying cycles and device utilization rates. Understanding how devices intersect with outpatient and hospital billing can change the sales cadence for clinical-targeted instruments.

Supply-chain inputs and unit economics: High-durability optical components (notably sapphire prisms and precision temperature-control assemblies) are key cost drivers and procurement bottlenecks. Manufacturers should model component scarcity and supplier concentration into lead-time and price-sensitivity scenarios.

Use-case boundary conditions: Desktop models are primarily designed for laboratory and research applications; regulatory and safety guidance restricts their use for direct patient contact without appropriate encapsulation and protocols. This affects product labeling, aftermarket accessories, and service obligations.

The market shows a blend of specialty instrument makers and broader analytical-technology companies. Our competitive mapping focuses on product differentiation, route-to-market, and adjacent-service capabilities rather than raw revenue splits.

Atago Co., Ltd. (Tokyo, Japan) — A long-standing market leader with a broad set of desktop models optimized for clinical, food, and industrial use. Recent launches emphasize user experience (enhanced touch interfaces) and expanded measurement scales for clinical specimen types. Strategic advantage: strong brand recognition in targeted verticals and rapid product iteration cadence.

Rudolph Research Analytical (New Jersey, USA) — Focused on laboratory-grade instruments with an emphasis on compliance and temperature-controlled models. Recent certification updates reinforce suitability for regulated environments. Strategic advantage: depth in laboratory and pharmaceutical specifications, enabling premium pricing for compliant models.

Anton Paar GmbH (Graz, Austria) — Positions multi-wavelength and high-end research instrumentation to the pharmaceutical and chemical sectors. Active trade-show visibility and technical demonstrations support enterprise adoption among QC labs. Strategic advantage: technological differentiation and strong R&D signal.

Mettler Toledo (Greifensee, Switzerland) — Integrates refractometry into a broader portfolio of lab instruments, enabling cross-sell into existing installed bases. Strategic advantage: global service footprint and established trust in clinical and pharmaceutical procurement.

Schmidt + Haensch (Berlin, Germany) — Boutique engineering focus on laboratory-grade refractometers used in diagnostic and beverage testing. Strategic advantage: niche specialization and customer intimacy in select verticals.

Bellingham + Stanley (Xylem Analytics, UK) — Offers industrial and clinical desktop models emphasizing robustness and accuracy for process control environments. Strategic advantage: access to industrial distribution channels and after-sales service networks.

Across the cohort, we observe three convergent strategies that matter for 2026 planning: (1) product-service bundling (device + software + scheduled calibration), (2) compliance-first positioning for clinical markets, and (3) incremental digitalization (cloud-enabled data capture, instrument lifecycle analytics). Companies that combine two or more of these levers are best positioned to accelerate share growth in the near term.

PW Consulting’s full Desktop Refractometers Market report is structured to move from insight to action. Highlights include:

Market sizing and scenario-based forecasts that translate macro demand into tactical procurement volumes for 2026–2028 planning cycles.

Product and ASP benchmarking frameworks designed for pricing teams to stress-test new model introductions without eroding installed-base margins.

Segmentation intelligence (by type, application, and region) presented with actionable channel strategies for enterprise, clinical, and industrial buyers. Note: detailed numerical splits are part of the paid dataset to protect commercial value.

Supply-chain risk dashboards, including single-supplier exposures for critical optical components and heat-mapped lead-time scenarios.

Regulatory and reimbursement playbooks—how ISO 15189 alignment and test-code interactions alter procurement windows and total cost of ownership.

Competitive profiles with capability matrices, go-to-market playbooks, and prioritized partnership/M&A targets for roll-up strategies.

Customer journey maps and procurement triggers across hospital labs, pharmaceutical QC, food & beverage testing, and research institutions—designed to inform targeted sales messaging and pilot programs.

Implementation checklists for post-sale activities (installation, calibration, qualification) to reduce onboarding time and increase retention.

Product Management: Prioritize modular designs that enable incremental upgrades to measurement scales, temperature control, and connectivity. Plan firmware and documentation releases timed to accreditation cycles.

Sales & Marketing: Reframe offers around bundled uptime guarantees and data integrity rather than headline specs alone. Emphasize compliance and integration readiness when selling into hospital networks.

Operations & Supply Chain: Hedge key optical component suppliers, establish second-source agreements, and build buffer strategies for seasonal demand spikes.

Corporate Development: Target tuck-ins that add service capacity, regional distribution, or complementary assay capabilities to accelerate installed-base monetization.

Consider this document a strategic trailer: it surfaces the directional forces shaping supplier economics, buyer behavior, and competitive moves, and it identifies the practical levers leaders must pull in 2026. For teams building budgets, the message is clear—invest early in compliance, field service, and data enablement to capture disproportionate value from a market growing at a steady mid-single-digit rate.

If your priority is executable, revenue-impacting detail—exact regional demand curves, application-level adoption thresholds, ASP bands, and a ranked list of acquisition targets—the full PW Consulting Desktop Refractometers Market report contains those granular datasets, models, and templates. The report also includes downloadable tools to stress-test your internal scenarios against our base, optimistic, and conservative demand paths.

Executive briefing: Schedule a one-hour strategy session with our authors to review the forecast scenarios and discuss tailored implications for your product or procurement roadmap.

Custom analysis: Commission a bespoke module (e.g., M&A target screening or distribution strategy) that uses our primary data and proprietary models to produce prioritized action lists.

Report access: Access to the complete dataset and the report’s annexes is available via PW Consulting’s publications portal for teams that require the full numerical segmentation and modeled financials.

PW Consulting’s Desktop Refractometers Market preview is intended to sharpen executive focus for 2026 planning. The market’s steady growth, regulatory complexity, and component-driven cost structure create clear winners and laggards. Organizations that align product development, compliance readiness, and service-led commercial models will convert forecasted market expansion into sustainable margin and share gains.

For detailed analysis of this topic, please visit the official page:Desktop Refractometers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com