Headlight Control Module Market Forecast: Technology Advancements and Future Opportunities Through 2034

Technology |

2026-06-19 13:18:11

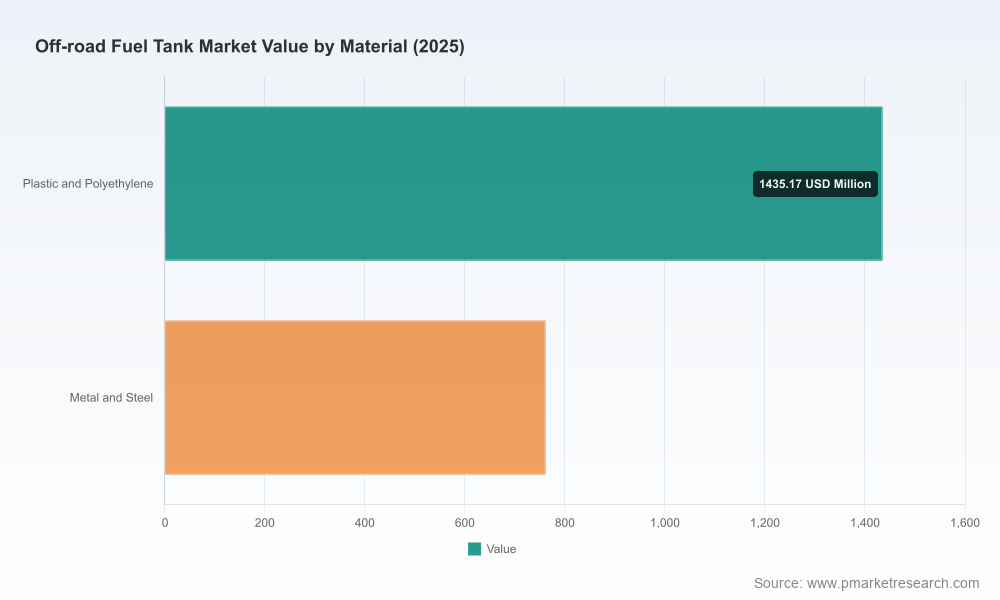

As capital allocation rounds intensify and equipment OEMs reset portfolios for the next business cycle, PW Consulting’s new Off Road Fuel Tank Market study offers a concise yet potent strategic playbook for executives planning through 2026. Using 2025 as the analytical base year, our market model shows the industry at roughly USD 2,196.8 Million in 2025 and tracking to a materially larger opportunity by the end of the forecast window. The market grows at a compound annual growth rate (CAGR) of 5.48% across our 2026–2032 forecast, underscoring steady expansion even as cost and regulatory pressures reshape supplier economics. This release is a “trailer” — it highlights the most actionable implications and decision levers for 2026 while directing readers to the full report for transaction-grade detail, model access, and supplier scorecards.

Off Road Fuel Tank Market

Material cost volatility. Between February 2025 and February 2026, aluminum mill shapes and steel mill products moved sharply higher — a dynamic that is compressing margins on metal fuel tanks and prompting manufacturers to reassess material strategies.

Off Road Fuel Tank Market

Plastics supply and pricing inflection. HDPE pricing and new capacity dynamics through 2025 are changing the relative economics of polymer-based tanks, accelerating investment in multi-layer and low-permeation designs that meet tighter evaporative standards.

Off Road Fuel Tank Market

Regulatory tightening. Ongoing EPA and CARB enforcement of evaporative emissions for small off-road equipment, together with Phase 3 heavy-duty greenhouse gas rules covering related operations, are forcing earlier-than-expected product redesigns and verification costs.

Aftermarket and operational resiliency. Demand for auxiliary and high-capacity refuelling solutions in remote operations (mining, construction camps, long-haul site logistics) continues to create attractive niches for aftermarket specialists.

Transparent market sizing and a reproducible forecasting model covering 2020–2032, with scenario overlays for commodity shocks, regulatory acceleration, and electric/hybrid equipment adoption.

Supply-chain heatmaps mapping raw-material exposure, cross-border sourcing risks, and buyer power by production technology (blow molding, rotational molding, metal fabrication, welded assemblies).

Material cost-sensitivity and margin pressure simulations that quantify breakpoint outcomes for metal vs. polymer strategies without requiring bespoke modelling.

Regulatory impact assessment with certification roadmaps and product-level design checklists aligned to EPA/CARB and heavy-vehicle GHG requirements.

Vendor benchmarking and strategic supplier shortlists, including capability matrices, time-to-market estimates, and integration risk scores for potential M&A or partnership targets.

Commercial playbooks for OEM negotiations, aftermarket channel expansion, and pricing architecture incorporating pass-through mechanisms and value-based contracts.

M&A and CapEx prioritization frameworks that connect strategic objectives to projected ROI over the forecast period.

The market shows a moderate level of concentration: established OEM-focused manufacturers and specialized aftermarket players both command meaningful share, creating a mix of competitive pressures and partnership opportunities. Below we synthesize public profiles and strategic implications for nine leading players featured in our analysis.

IFH Group — Strong in custom metal and stainless-steel fabrication for heavy off-highway applications. Strategic implication: IFH’s steel capability remains core where structural robustness and large-capacity tanks are required; however, hedging steel-price exposure and selective polymer partnerships will be necessary to defend margins.

Standard Technologies — OEM-facing supplier with hardened designs for harsh environments. Strategic implication: leverage deep OEM relationships to co-develop lighter, certified solutions that meet evolving permeation standards while protecting aftersales streams.

Agri-Industrial Plastics — High-volume blow molder with EPA/CARB-compliant multi-layer HDPE tanks. Strategic implication: well positioned to capture share where permeation regulation favors multilayer plastics; consider capacity deals and long-term resin contracts to lock input cost advantages.

Elkamet — European plastics tank specialist meeting stringent regional safety standards. Strategic implication: EU-compliant design and regulatory know-how are differentiators for suppliers targeting transnational OEM programs and export markets subject to strict certification regimes.

Transfer Flow, Inc. — Aftermarket specialist in auxiliary and replacement systems. Strategic implication: aftermarket players will be a primary channel for extended-range and field-service solutions; OEMs and suppliers should evaluate channel partnerships to capture aftermarket lifetime revenue.

TITAN Fuel Tanks — Polymer innovation with military-grade cross-linked materials. Strategic implication: polymer technology leadership provides a defensible premium position for off-road enthusiasts and extreme-use cases; consider white-label or co-branding to enter adjacent commercial equipment segments.

Niece Equipment — Niche provider for very large-capacity refuelling trucks and beds. Strategic implication: scale specialists can command project-level pricing; opportunities exist for modular product lines and service contracts that turn single sales into recurring revenue.

Harmon Racing Cells — Safety-focused fuel cells and bladders for racing and extreme off-road. Strategic implication: safety certification and niche engineering are high-margin adjacencies—OEMs seeking to upgrade product safety can partner for tech transfer.

Extreme Tanks — Custom aluminum and stainless steel fabricator for racers and industrial use. Strategic implication: custom shops offer speed-to-market for prototype and low-volume programs; larger suppliers should maintain relationships for niche or high-spec contracts.

Adopt layered procurement tactics: a mix of long-term resin and metal contracts, option clauses for volume swings, and indexed pricing to preserve margins during commodity spikes.

Accelerate material substitution pilots where technical equivalence is achievable: polymerization and multi-layer HDPE approaches can reduce structural-metal content and lower cost exposure to steel/aluminum cycles.

Implement design-for-cost programs that prioritize modularity and commonality across product lines to lower unit costs and shorten lead times.

Build supplier flexibility: qualify at least two suppliers per critical input and consider regional dual-sourcing to mitigate logistics and tariff risk.

Comply early and cost-effectively with permeation and evaporative limits by investing in multi-layer and barrier technologies; early movers reduce retrofit and warranty risk.

Embed lifecycle greenhouse gas assessments in product development to align with heavy-duty Phase 3 and corporate sustainability targets — this will increasingly influence procurement decisions by large equipment buyers.

Plan certification timelines and test budgets into product launch schedules; regulatory lag is an operational risk that can delay revenue capture.

Prioritize a “material-flex” roadmap: balance polymer and metal lines, allocate R&D to multi-layer HDPE and permeation barriers, and create a timeline for staged substitution where cost-effective.

Lock in critical resin or mill capacity through off-take or strategic equity relationships to stabilize COGS in a volatile metal-pricing environment.

Expand aftermarket and service offerings to capture higher-margin, lower-capex revenue streams that are less commodity-sensitive.

Target tuck-in acquisitions that add polymer capabilities, certification expertise, or large-capacity manufacturing to fill portfolio gaps quickly.

Enhance commercial agreements with pass-through mechanisms and indexed escalators tied to transparent commodity indices to preserve margins without alienating customers.

This article is crafted as a strategic preview intended to inform board-level and executive planning for 2026. The full PW Consulting Off Road Fuel Tank Market report contains the granular models, supplier scorecards, unit-cost breakdowns, and deal-structuring templates necessary to act. Subscribers receive editable financial models, scenario dashboards, and access to analyst briefings to fast-track decision-making. For teams executing procurement, product strategy, M&A screening, or investor diligence, the full report converts the qualitative direction above into executable roadmaps and transaction-ready outputs.

Contact PW Consulting to schedule a briefing and obtain the full dataset and advisory engagement options. Treat this piece as a directional roadmap — the tactical levers you deploy next quarter will set competitive positioning for the rest of the decade.

For detailed analysis of this topic, please visit the official page:Off Road Fuel Tank Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com