PW Consulting Releases Strategic Brief: Navigating the Global AIDS Therapeutics Market — Critical Intelligence for 2026 Decision-Making

PW Consulting today publishes a strategic companion to our full Acquired Immunodeficiency Syndrome Market report (base year 2025, historical window 2020–2025, forecast 2026–2032). The abbreviated release below synthesizes the report’s highest‑value insights for senior leaders shaping portfolios, access strategies, and partnerships in 2026 — while deliberately withholding the granular segmentation tables and line‑level forecasts that sit behind our models. Organizations that require the complete datasets and scenario models should refer to the full report.

Acquired Immunodeficiency Syndrome Market

Executive summary: why 2026 is a pivot year

The global market for HIV therapeutics continues to expand, with PW Consulting’s base‑case model placing the industry at a substantial USD Million scale in 2025 and projecting a steady compound annual growth rate (CAGR) of 5.42% across the 2026–2032 forecast window. Our top‑line forecast is consistent with ongoing product lifecycle transitions (long‑acting injectables, next‑generation single‑tablet regimens), accelerating adoption in treatment programs, and sustained public‑sector procurement for low‑ and middle‑income countries (LMICs).

Acquired Immunodeficiency Syndrome Market

What makes 2026 distinct is the convergence of three forces that materially re‑shape competitive and access dynamics:

Acquired Immunodeficiency Syndrome Market

- Rapid clinical and regulatory movement on long‑acting and novel oral regimens, changing switching and prevention paradigms;

- Near‑term generic production and voluntary licensing initiatives that will broaden procurement options in LMICs; and

- A concentrated supplier structure at the top of the market that magnifies strategic impact from a handful of product and access decisions.

What the full report delivers — practical contents for action

PW Consulting’s full market study is built to be operational for commercial, access, and corporate development teams. Key deliverables include:

- Robust market sizing and revenue forecasts (global and country‑level) for 2026–2032 with sensitivity scenarios tied to differing adoption curves of long‑acting and simplified oral regimens;

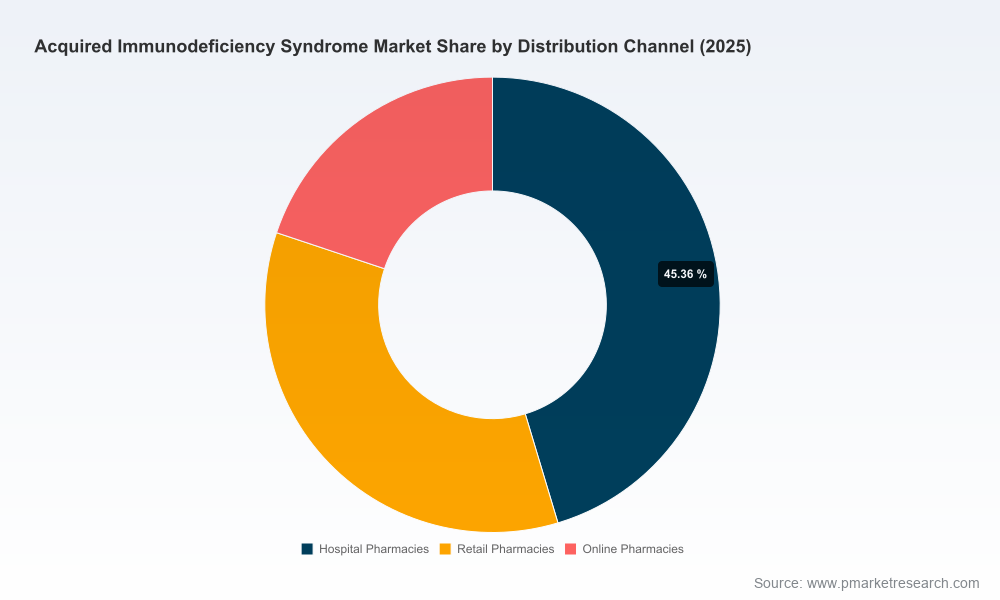

- Commercial segmentation and channel analysis — hospital, retail and digital distribution pathways — with go‑to‑market levers mapped to customer archetypes;

- Competitive benchmarking for leading innovators, originators and major generic suppliers, combining product portfolios, pipeline timing, and go‑to‑market posture;

- Strategic access and pricing intelligence focused on public procurement mechanisms, tiered pricing pathways, and likely tender dynamics in LMIC programs;

- Regulatory and reimbursement trackers for key jurisdictions, with milestone calendars that feed into launch readiness; and

- Decision support tools — scenario models and M&A / partnership playbooks — enabling teams to stress‑test investment, licensing, and capacity decisions under multiple uptake scenarios.

Competitive landscape — strategic takeaways for incumbents and challengers

The market remains top‑heavy: aggregated market concentration metrics indicate that the leading few firms capture the large majority of market revenues, creating high strategic leverage for firms that can shape prescribing standards and access agreements.

- Incumbent innovators (Gilead Sciences, ViiV Healthcare, Merck & Co.) — These firms drive the product innovation frontier. Recent clinical and regulatory milestones illustrate how product cadence can rapidly impact competitive positioning: late‑stage single‑tablet and long‑acting combinations are demonstrating switching advantages, and regulatory approvals of next‑generation oral regimens are reshaping maintenance therapy choices. For incumbents, priority actions in 2026 include accelerating label expansions, locking in co‑formulation IP pathways, and optimizing commercial models (private vs. public tender) by product modality.

- Large diversified pharma and protease‑specialists (Johnson & Johnson, Bristol‑Myers Squibb, AbbVie, Boehringer Ingelheim, Roche) — These players retain strategic relevance through legacy antiretroviral portfolios and diagnostic linkages. Their near‑term value lies in lifecycle management and in serving niche therapeutic needs (e.g., salvage therapy, treatment for co‑morbid patients). Strategic focus should be on partnership-led approaches that connect their assets to new regimens and diagnostics.

- Generics and high‑volume suppliers (Cipla, Viatris, Teva, Aurobindo, Dr. Reddy’s, Hetero, Emcure) — The supply landscape for LMICs is poised to broaden as voluntary licensing and tech‑transfer efforts ramp. Generic entrants are set to be decisive for price and procurement outcomes. Manufacturers should prioritize manufacturing scale‑up timelines, assurance of quality (including WHO prequalification), and flexible supply‑chain solutions that de‑risk tenders for donors and national programs.

For all cohorts, our analysis highlights three tactical priorities: (1) align regulatory timelines with procurement cycles to capture early tender windows; (2) design pricing and access propositions that reflect differentiated willingness‑to‑pay across payer segments; and (3) keep clinical differentiation tangible to prescribers — i.e., invest in real‑world evidence and head‑to‑head switch data that support label and guideline inclusion.

Recent clinical, regulatory and access developments shaping 2026 strategies

- Regulatory approvals and filings in 2025–2026 have shifted the product mix for both treatment and prevention, with several long‑acting and novel oral regimens gaining regulatory momentum. These milestones materially affect launch sequencing and revenue ramps.

- High‑profile clinical readouts in early 2026 reinforced the case for new combination regimens in maintenance therapy, altering switch‑study dynamics and the calculus for guideline adoption.

- Access partnerships and voluntary licensing agreements announced over the past 18 months have created credible pathways for affordable generic supplies in many LMICs. Procurement offices and donors are already re‑tooling tenders to accommodate injectable prevention options and simplified maintenance regimens.

PW Consulting’s full report contains a compact, dated milestone map that links these events to expected procurement cycles and guideline revision timelines so teams can set landing zones for negotiations and launch sequencing.

Market dynamics and access environment

Global HIV program dynamics continue to be defined by near‑universal adoption of “treat all” principles and progressive alignment around WHO‑preferred regimens. Program scale remains large: tens of millions receive antiretroviral therapy and a substantial share of those on treatment have reached viral suppression. Yet gaps persist — new infections continue to occur, and prevention scale remains a strategic priority for donors and national programs.

What this means for 2026 decisions:

- Payers and ministries will increasingly prioritize regimens that combine efficacy, simplified dosing, and favorable procurement economics. Manufacturers must present a clear value case that balances clinical advantage with total cost of ownership;

- Donor‑led procurements will favor suppliers offering predictable manufacturing scale, transparent tech transfer, and demonstrated cost containment strategies;

- Diagnostics and linkage to care will be critical ancillary markets — providing cross‑sell and retention opportunities for companies that can integrate testing and treatment pathways.

Strategic recommendations for 2026 (prioritized)

- Portfolio owners: update program economics using PW Consulting’s scenario models that explicitly map variant adoption curves for long‑acting vs. oral regimens; reallocate field resources to early‑adopter geographies and payer segments that anchor long‑term uptake.

- Commercial leaders: design differentiated contracting suites (volume tiers, outcome‑linked clauses, time‑limited launch rebates) that anticipate tender evaluation criteria and procurement cadence.

- Access teams: accelerate voluntary license negotiations and prepare tech‑transfer playbooks — early engagement with major procurers and donors is now table stakes for capturing LMIC demand shifts.

- M&A and BD executives: prioritize bolt‑on assets that accelerate time‑to‑market for long‑acting formulations or strengthen supply reliability for public tender channels; pre‑emptive alliances can be material value creators given the market’s concentration dynamics.

What PW Consulting’s models reveal — and what we withhold here

Our full analytical suite quantifies upside and downside revenue paths under alternative adoption rates, pricing concessions, and launch delays. We also map country‑level elasticities and channel‑specific uptake timing. To preserve the utility of this press overview as a strategic “trailer,” we have intentionally omitted granular regional and application splits, per‑company revenue lines, and unit‑price assumptions — all of which are provided in the complete report and spreadsheet deliverables.

Next steps: how to use this intelligence in Q2–Q4 2026 planning

- Request the full report and extract the scenario module relevant to your product class to generate board‑level briefings on market exposure and upside opportunities;

- Use our competitive playbook to map likely competitor responses to your 2026 launches or tender bids and to stress‑test partnership strategies with generic manufacturers and diagnostics providers;

- Engage PW Consulting for a condensed workshop to convert model outputs into a 90‑day commercialization & access action plan tailored to your organization’s risk tolerance and market priorities.

PW Consulting’s Acquired Immunodeficiency Syndrome Market study is engineered for executives who must make consequential 2026 choices with imperfect information. It provides defensible forecasts (base year 2025), a transparent 2026–2032 modeling framework with a 5.42% CAGR baseline, and decision‑grade intelligence on competitive moves, access evolutions, and procurement rhythms.

To receive the full report, the accompanying datasets, and an executive briefing, please visit our publication page or contact a PW Consulting industry lead. The comprehensive version includes the withheld segment tables, country forecasts, and a customizable scenario workbook that many clients use directly in tender planning and BD negotiations.

For detailed analysis of this topic, please visit the official page:Acquired Immunodeficiency Syndrome Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com