Functional Bio-based Chemicals Market Set to Hit USD 18.5 Million by 2034 at 7.5% CAGR

Other |

2026-06-16 12:20:16

PW Consulting’s latest market study on the global Climbing Equipment Market is designed as a practical strategic toolkit for leadership teams planning for 2026 and beyond. Built on a refreshed base-year of 2025 and a rigorous 2026–2032 forecast horizon, the report synthesizes commercial, regulatory, and supply-chain dynamics into actionable implications for product, channel, and M&A decisions. At the macro level, the market has demonstrated sustained expansion through the first half of the decade and enters 2026 projecting a mid-single-digit compound annual growth rate (CAGR) of 6.8%—an important baseline for sizing investments and modelling returns.

Climbing Equipment Market

Market momentum meets structural disruption: After steady revenue growth to the 2025 base year, the market enters a phase where product innovation, standards changes, and raw-material volatility drive outsized differentiation. That makes 2026 the pivotal year for repositioning portfolios and securing supply chains.

Climbing Equipment Market

Regulatory inflection points are active: Industry-wide safety standard revisions and high-profile recalls have increased both compliance costs and reputational risk, making proactive compliance strategies a competitive advantage rather than a compliance cost center.

Climbing Equipment Market

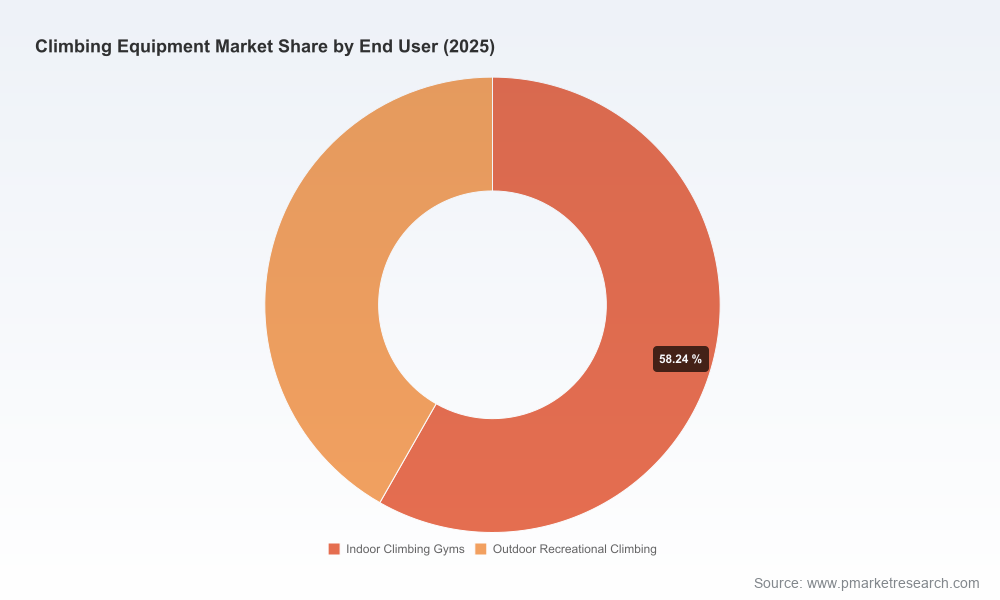

Customer segmentation is evolving: Indoor gym ecosystems, outdoor recreation, and technical alpine users are each following distinct trajectories. Winning in 2026 will depend on tailored value propositions rather than broad-brush product plays.

Clear growth trajectory: Our market model records multi-year expansion through 2025 and a forecast trajectory that supports investment pacing for product R&D, channel expansion, and targeted acquisitive growth.

Fragmented competitive structure: Market concentration metrics indicate a market where the top few players hold material share but leave ample room for nimble challengers and regional specialists to scale—creating opportunities for both organic growth and consolidation plays.

Margin pressure levers identified: The report quantifies upstream cost pressures such as tariff-driven metal price impacts and recent raw-material-driven retail price inflation among entry-level participants—critical inputs when stress-testing margins under different price pass-through scenarios.

Scenario-based demand forecasting: Multiple demand scenarios for 2026–2032 that allow commercial teams to stress-test product launches, channel investments, and pricing strategies against alternative recovery, premiumization, and adoption pathways.

Supply-chain risk heatmap: Granular supplier and input-risk mapping—highlighting single-source metal components, rope-fiber dependencies, and logistics pinch points—paired with mitigation playbooks (dual-sourcing, hedging, nearshoring, inventory policy adjustments).

Regulatory & safety compliance playbook: A stepwise approach to incorporate recent and pending standard revisions into product development, testing, and labeling processes—reducing time-to-market for compliant SKUs and avoiding recall exposure.

Go-to-market (GTM) playbooks by end-use: Practical GTM templates for indoor gym partnerships, premium technical channels, and direct-to-consumer initiatives—each with recommended KPIs, channel economics, and promotional cadences.

Value capture and pricing sensitivity tools: Monte Carlo–style modules that quantify margin outcomes across pricing, cost, and volume sensitivities—a particularly relevant tool given recent price inflation in entry-level equipment.

M&A target screening and integration checklist: A prioritized list of capability targets (e.g., niche hardware specialists, rope manufacturers with proprietary testing, digital-training platforms) accompanied by integration playbooks focused on preserving brand authenticity and operational synergies.

Product roadmap implications: Design-and-innovation recommendations that incorporate evolving safety standards, sustainability expectations, and shifts toward lightweight, high-performance materials.

The report profiles the market’s established manufacturers and emerging challengers, assessing each on product breadth, brand equity, channel strength, and innovation cadence. Notable incumbents covered include well-known global names that span hardware, ropes, footwear, and technical apparel. Each company profile in the report contains practical intelligence: core strengths, strategic vulnerabilities, recent product and corporate moves, and potential strategic trajectories for 2026.

Brands with comprehensive hardware portfolios typically compete on safety credentials and distribution breadth—advantages in professional and technical segments.

Manufacturers focused on ropes and technical textiles are increasingly defining competitive advantage through proprietary fiber blends, in-house testing, and certification traceability—areas our scenario analysis treats as defensible moats versus pure price competition.

Footwear and apparel leaders are leaning into premiumization and lifestyle positioning, leveraging brand equity to sustain pricing power even as entry-level price sensitivity increases.

Standards and safety updates: Revisions to several key industry safety standards over the past 18 months have raised the bar for helmets, energy-absorbing systems, and load-sharing devices. For manufacturers, this creates both compliance cost and product differentiation opportunities when navigated proactively.

High-profile recalls: Recent recalls related to material degradation in harnesses and isolated batches of ropes have amplified the reputational and legal risk of inadequate testing protocols—reinforcing the strategic value of rigorous lifecycle testing and transparent traceability.

Product innovation cycle: Numerous spring and winter product launches across established players emphasize modular accessories, eco-conscious materials, and gym-focused training aids—signals that product ecosystems are expanding beyond classic hard goods into recurring-purchase consumables and services.

Cost volatility: Tariff shifts on steel and aluminum in certain markets, combined with raw-material-driven price rises seen in recent years, require firms to re-evaluate sourcing geographies, pricing governance, and product bill-of-material designs.

Reassess portfolio fit by segment: Given diverging end-user behavior, product portfolios should be rationalized to focus R&D spend on higher-growth, higher-margin segments while establishing cost-efficient SKUs for mass-market channels.

Invest in compliance as a market moat: Treat compliance and testing capability as strategic assets—investments here reduce recall risk, shorten certification lag, and create premium positioning in safety-sensitive channels.

Lock in resilient sourcing: Develop multi-tier supplier networks for metal hardware and rope fibers, and model inventory strategies that balance working capital with service-level expectations across seasonal demand curves.

Monetize adjacent ecosystems: Leverage brand credibility to create recurring-revenue touchpoints (training subscriptions, consumables, route-setting services for gyms) that smooth seasonality and increase customer lifetime value.

Pursue bolt-on M&A selectively: Target acquisitions that provide tested capability gaps—material science labs, proprietary rope manufacturing, or digital training platforms—over undifferentiated revenue scale.

Designed for executive teams, the report combines a defensible market baseline with tactical modules that translate market signals into concrete actions. It is especially useful for:

Heads of Strategy and Corporate Development sizing acquisition math and integration risk.

Product leaders setting two- to five-year roadmaps aligned to regulatory timelines and customer willingness to pay.

Commercial leaders refining channel mix between specialty retail, gyms, and DTC to optimize margins and customer acquisition costs.

Supply-chain and procurement leaders designing resilient, cost-effective sourcing strategies in the face of tariff and material shocks.

This release delivers a distilled preview of the substantive insights our full report contains. To preserve the competitive integrity of the market’s segment-level allocations and detailed financial models, the full dataset, segmentation granularity, and downloadable scenario tools are published exclusively in the complete report. PW Consulting invites decision-makers seeking executable, quantitative support for 2026 planning to review the full offering and to schedule a tailored briefing where we can map the model to your organization’s balance sheet and strategy targets.

PW Consulting’s Climbing Equipment Market report translates growth forecasts, regulatory shifts, and competitive movements into practical actions—so that leadership teams can move from uncertainty to a prioritized set of initiatives with clear commercial impact in 2026.

For detailed analysis of this topic, please visit the official page:Climbing Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com