Why Is Flow Wrap for Wipes Market Growing in Hygiene Packaging Industry?

Networking |

2026-05-22 12:52:06

PW Consulting’s forthcoming Filter Pump Market report synthesizes five years of historical observation (2020–2025) with a multi-scenario forecast (2026–2032) to deliver decision-grade intelligence for 2026 corporate planning cycles. The industry sits on a steady expansion path: our base-year assessment pegs global revenue at USD 1,485.2 Million in 2025, with a compound annual growth rate (CAGR) of 5.65% across the 2026–2032 forecast window. Under a central scenario, the market is modeled to cross roughly USD 2.18 billion by 2032, reflecting sustained demand driven by energy-efficiency retrofits, regulatory tightening, and technology-driven product differentiation.

Filter Pump Market

Timing-sensitive capital allocation: 2026 is a pivotal year for pump OEMs, system integrators, and downstream buyers to align CAPEX and R&D plans with evolving energy-efficiency standards and a market that rewards variable-speed and smart-capable units.

Filter Pump Market

Portfolio prioritization: With mid-term CAGR in the mid-single digits, firms must balance volume-driven growth plays against margin-accretive moves (e.g., smart controls, service contracts).

Filter Pump Market

M&A and partnership windows: Market concentration is moderate — the top three players hold a notable share, while the top five account for just over half the market — creating tactical opportunities for bolt-on acquisitions and strategic alliances to secure distribution or specialist technology.

Regulatory arbitrage and product roadmaps: National and state-level energy rules now materially affect product viability; firms that anticipate standards and embed compliance into product lifecycles will preserve time-to-market advantages.

To establish context without disclosing the granular splits reserved for the full report, PW Consulting summarizes key macro datapoints informing our conclusions: the global filter pump market reached USD 1,485.2 Million in 2025 and is projected to grow at a 5.65% CAGR through 2032, reaching approximately USD 2,182.65 Million under our central forecast. Market concentration metrics indicate a competitive but consolidating landscape: the three largest suppliers control a meaningful portion of value, and the top five firms together command just over half of the market. These macro anchors frame all downstream scenario analysis in the report.

Regulatory momentum and energy economics: Mandatory efficiency thresholds (for instance, Dedicated Purpose Pool Pump energy rules and regional variable-speed motor requirements) are accelerating replacement cycles and creating pull for high-efficiency, variable-speed platforms. Equipment that reduces operating expense through smart flow management is increasingly a procurement differentiator.

Technology and systems convergence: Pumps are transitioning from isolated hardware items to nodes within connected filtration ecosystems. Integrations with automation platforms and the adoption of smart controls enable performance-based warranties, energy-monitoring services, and aftermarket revenue streams.

Channel fragmentation vs. consolidation: While established OEMs maintain advantages in brand and distribution, there is measurable room for niche specialists and low-cost providers in specific channels (e.g., above-ground residential pools, corrosive industrial processes). Commercial buyers are demanding more turnkey system solutions rather than component-only offerings.

Service and lifecycle economics: Buyers increasingly evaluate total cost of ownership — installation, energy consumption, maintenance intervals, and disposal/recycling. Pumps that reduce life-cycle energy use or simplify maintenance can command premium pricing and longer-term contracts.

Prioritize efficiency-first product roadmaps. Manufacturers should fast-track variable-speed and smart-control variants, and embed modularity to allow field upgrades as standards evolve. This protects installed-base value and supports aftermarket services.

Reconfigure go-to-market by channel. Distinguish channel strategies for residential retrofit, commercial pools, and industrial filtration — each requires differentiated pricing, warranty, and installation support packages. In 2026, channel-tailored pilot programs will yield disproportionate returns.

Monetize data and maintenance. Develop subscription-ready offerings (monitoring, predictive maintenance, consumable replacement) to shift some revenue from one-time sales to recurring streams and to improve lifetime margin.

Accelerate compliance-led innovation. Use regulatory timelines as a product development compass. Investing in pre-compliance models and third-party testing reduces time-to-certification and protects access to regulated markets.

Assess acquisition targets for capability gaps. Prioritize bolt-on acquisitions that add corrosion-resistant materials expertise, smart controls IP, or regional distribution where incumbents have weak coverage.

The sector features a mixed composition of specialist manufacturers, global OEMs with diversified water portfolios, and value-focused consumer brands. Leading firms exemplify distinct strategic archetypes:

Specialist, high-performance suppliers — e.g., Filter Pump Industries (Finish Thompson division) — compete on corrosion-resistant materials, chemically compatible designs, and application-specific filtration solutions for metal finishing and aggressive media. Their value proposition is reliability in demanding environments and domestic manufacturing credentials.

Market-leading pool system OEMs — notably Pentair and Hayward — are leveraging variable-speed platforms, integrated automation, and brand strength across retail and contractor channels. Recent product awards and catalogue launches underscore their emphasis on efficiency and portfolio refresh cycles.

Value and channel specialists — firms such as Intex and Bestway — target the above-ground residential segment with sand-filter combos and price-driven product bundles, creating volume pressure at the entry level.

Industrial and water-technology incumbents — including Grundfos, Xylem, Parker Hannifin, and Donaldson — bring deep expertise in energy-efficient drives, system integration, and aftermarket services for industrial and municipal filtration. Their strategic advantage lies in cross-selling to broader water and process portfolios.

Recent industry movements emphasize these dynamics: Pentair’s product recognitions and catalogue refreshes signal ongoing investment in variable-speed technologies; Hayward’s integration of new variable-speed lines with automation highlights the pivot to smart systems; and Finish Thompson’s prior acquisition of a specialist pump producer illustrates consolidation aimed at expanding corrosion-resistant offerings.

Energy-efficiency standards: Federally and regionally mandated efficiency thresholds are reshaping allowable product specifications and end-user economics. Products that demonstrably lower energy consumption — in some cases by orders of magnitude compared to legacy single-speed designs — will capture procurement preference.

Motor and drive innovation: Advances in power electronics and variable-speed drives are enabling finer hydraulic control, quieter operation, and improved reliability. Firms that control motor-packaging and firmware integration will extract higher margins from services and warranties.

Data interoperability: Standardized APIs and control protocols are emerging as a competitive battleground. Ecosystem players that enable third-party integrations without sacrificing control over the user experience will benefit from platform effects.

The complete report delivers operationally actionable modules designed for commercial and technical leaders:

Robust market-sizing and forecast models with scenario analysis (central, conservative, and upside cases) and sensitivity testing tied to regulatory timelines and energy-price drivers.

Channel and go-to-market playbooks, including recommended distributor incentive structures, retrofit promotion tactics, and pilot program templates for energy-service models.

Comprehensive competitive profiles and capability matrices for key suppliers, with M&A screening criteria and a prioritized list of acquisition targets by strategic fit.

Product roadmap stress tests that map R&D investments to margin outcomes and market-share trajectories across plausible regulatory and commodity-cost scenarios.

Procurement and specification templates for large buyers to standardize TCO assessments, performance warranties, and service-level agreements.

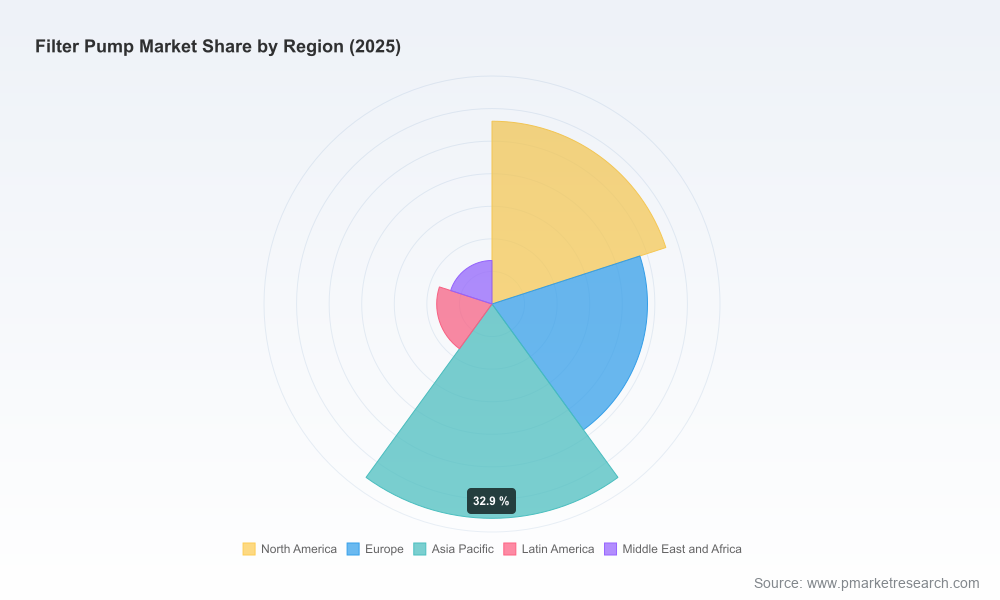

PW Consulting deliberately omits granular regional and application-level splits in this public summary to preserve the strategic value of the full dataset. The full report includes the detailed segmentation breakdowns, price curves, and model outputs that inform vendor selection, pricing strategies, and M&A valuations.

For product leaders: finalize high-efficiency variants and test connected-control prototypes with pilot customers; align certification timelines with regulatory milestones.

For commercial teams: launch targeted retrofit campaigns in channels showing highest near-term replacement potential; bundle service contracts to capture recurring revenue.

For corporate development: run diligence on adjacent-materials and controls firms flagged in our acquisition framework; prioritize targets that accelerate compliance or open strategic channels.

For investors and boards: use our scenario outputs to stress-test valuations against tightening efficiency standards and to size acquisition synergies conservatively.

This briefing is a trailer: it demonstrates PW Consulting’s methodology and highlights the strategic questions every executive must answer in 2026. For the comprehensive datasets, sensitivity models, and granular segmentation required to execute on the recommendations above, please access the full Filter Pump Market report and supporting Excel models at our report page. The full deliverable is designed to be directly incorporated into 2026 budgeting, R&D planning, and M&A screening processes.

PW Consulting remains available for bespoke advisory engagements, scenario workshops, and due-diligence support to convert the insights in this report into executable 2026 strategies.

For detailed analysis of this topic, please visit the official page:Filter Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com