PW Consulting Releases Strategic Briefing on the Fertility ELISA Test Kit Market: What 2026 Decision‑Makers Need to Know

PW Consulting today publishes a strategic industry briefing extracted from its forthcoming Fertility ELISA Test Kit Market report — a practical, decision‑oriented companion for executives planning investments, product launches, regulatory strategies and M&A in 2026. Built on a proprietary dataset spanning 2020–2025 and a scenario‑driven forecast for 2026–2032, the briefing synthesizes market dynamics that will materially influence commercial outcomes in the next 12–36 months.

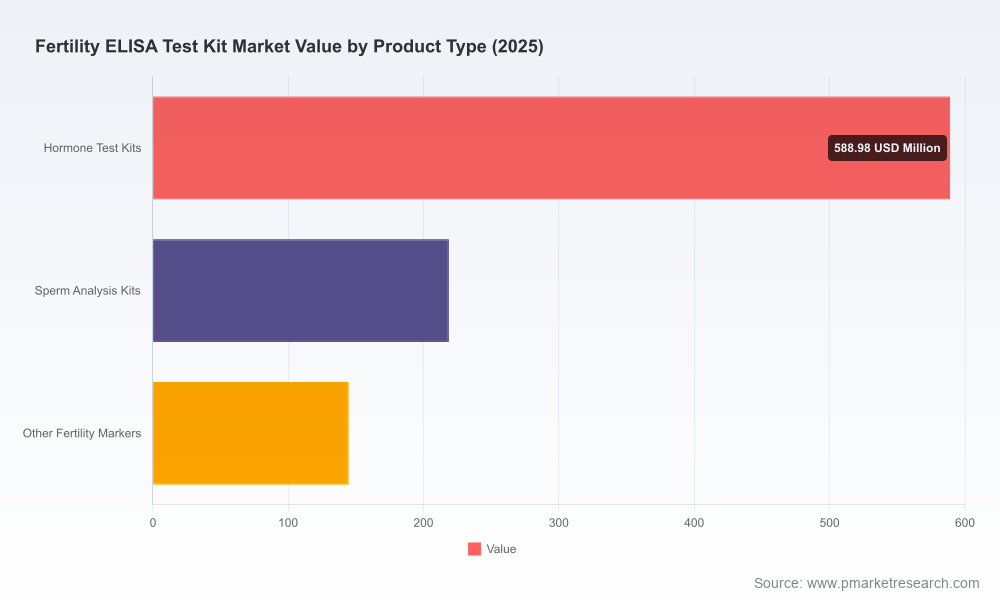

Fertility Elisa Test Kit Market

Market at a glance: growth backdrop and concentration

The fertility ELISA test kit market demonstrated steady expansion during the historical window, rising from just over USD 700 million in 2020 to roughly USD 952.5 million in 2025. Our base‑case forecast shows continued expansion through the 2026–2032 period at a compound annual growth rate (CAGR) of 6.12%, with total market value projected to surpass USD 1.44 billion by 2032. These topline metrics frame a market that is large enough to support both scale players and nimble specialists, yet sufficiently dynamic to reward targeted innovation.

Fertility Elisa Test Kit Market

Market concentration metrics underline that leadership is meaningful but not prohibitive: the top three firms account for a material share of sales while the five largest vendors together hold just over half of market revenues, indicating room for differentiated entrants and carve‑out opportunities for focused clinical or geographic strategies.

Fertility Elisa Test Kit Market

Why this briefing matters to 2026 enterprise decisions

- Rapidly moving regulatory and reimbursement expectations (see dynamics below) will shape go‑to‑market timing and clinical evidence investments. Knowing the pace and cost of regulatory routes is now a table‑stakes decision for product roadmaps.

- Moderate market concentration means strategic M&A and bolt‑on acquisitions remain practical ways to accelerate channel access and laboratory validation footprints — but value creation depends on precise diligence against assay performance, manufacturing quality systems, and regulatory dossiers.

- The forecast horizon (2026–2032) requires companies to reconcile near‑term commercialization with multi‑year platform investments (assay panels, automation compatibility, digital reporting) to capture growth pockets and protect margin under pricing pressure.

What the full report provides (practical deliverables)

This briefing is a distilled sample of the full deliverable. The comprehensive report includes operationally actionable content designed for strategy teams, product leads, commercial heads and corporate development groups, including:

- Detailed market sizing and demand models with historical trends (2020–2025) and scenario forecasts (2026–2032) that power sensitivity testing for price, uptake and regulatory timing.

- Segmented market maps (product, end‑user and geographies) coupled with adoption curves and high‑probability TAM/SAM/SOM deliverables. (Note: the public briefing intentionally omits the granular segment tables found in the full report to protect proprietary modeling.)

- Competitive landscaping with functional profiles, positioning matrices and product comparators for major suppliers and emerging challengers; a practical playbook for differentiation and partnership evaluation.

- Regulatory and reimbursement playbooks that translate standards (e.g., FDA clearance pathways, CE processes and ISO 13485 requirements) into operational timelines, typical evidence packages and estimated resource needs.

- Go‑to‑market plans tailored by channel (clinical labs, fertility clinics, hospital networks, research institutes), including sample contracting term frameworks, validation milestone maps, and pilot study templates.

- Manufacturing and quality audits templates focused on ELISA‑specific critical control points, supplier risk matrices and capacity planning checklists for scale‑up.

- M&A and valuation toolkits (deal comparables, revenue multiples, synergy checklists and integration risk matrices) crafted for buyers and sellers in this market.

- Source transparency: primary interviews with lab directors, IVF clinic directors, regulatory consultants and senior commercial managers, plus method notes for our forecasting approach.

Competitive landscape — what separates winners from followers

Our analysis focuses on capability stacks and go‑to‑market vectors rather than static product lists. Four representative companies illustrate the prevailing strategic archetypes:

- Ansh Labs (Webster, TX, USA) — Specialized immunoassay expertise with AMH ELISA offerings built on proprietary monoclonal antibodies. Strengths: deep technical IP in reproductive markers, targeted clinical positioning for ovarian reserve and IVF outcome assessment. Strategic levers: convert research‑use recognition into broader clinical claims via focused validation studies and regulatory filings.

- DRG International (Springfield, NJ, USA) — Broad ELISA portfolio including competitive steroid and estradiol assays used in fertility workflows. Strengths: extensive assay breadth and established lab channel relationships. Strategic levers: emphasize clinical utility data for high‑impact use cases (ovulation induction monitoring, IVF cycle management) and optimize manufacturing scale economics.

- Monobind (Lake Forest, CA, USA) — Multi‑menu IVD supplier producing AccuBind ELISA kits across endocrine and reproductive panels. Strengths: diversified product mix and distribution footprint. Strategic levers: integrate assay kits with digital result management and lab automation to defend against commoditization.

- Sure Bio‑Tech (USA) Co., Ltd. (Burlingame / Escondido; operations in HK and mainland China) — Export‑oriented supplier with CE and quality system credentials catering to international labs. Strengths: cost‑competitive manufacturing and regulatory compliance for export markets. Strategic levers: pursue strategic partnerships with regional distributors and invest in clinical evidence to access higher‑margin clinical channels.

Across these archetypes, winning strategies converge on several themes: demonstrable analytical performance (sensitivity, specificity), clinical validation that ties assay results to meaningful care pathways, regulatory clearance that supports commercial claims, and service models that reduce lab friction (validated reagents, QC programs, automation compatibility).

Regulatory and reimbursement dynamics that should shape 2026 plans

- Regulatory: ELISA kits for fertility hormones — notably AMH and other reproductive markers — are subject to jurisdictional regulatory pathways. Strategic decisions should be built around realistic timelines for FDA clearance or de novo authorization where a test’s intended use requires it, and CE marking trajectories for European market entry.

- Quality systems: ISO 13485 adherence is a practical prerequisite for medical device manufacturing and distribution in most target markets; investments in quality management pay off during audits and commercial scaling.

- Reimbursement: fertility hormone assays commonly fall under broader clinical laboratory coding structures rather than discrete fertility‑specific codes. This reality increases the importance of demonstrating economic and clinical utility to secure favourable lab adoption and billing practices.

Priority strategic plays for 2026

Based on our modeling and primary interviews, PW Consulting recommends executives consider the following prioritized actions for the coming 12–18 months:

- Accelerate clinically meaningful differentiation: invest selectively in head‑to‑head validation, utility studies tied to treatment pathways and real‑world evidence generation that supports higher value positioning.

- Lock‑in regulatory strategy early: choose the optimal first‑market clearance route (CE vs. FDA) based on time‑to‑value and the intended commercial channel. Build dossier timelines into commercial launch plans to avoid downstream delays.

- Operationalize ISO 13485 and supplier quality programs: these are not optional if you aim for hospital and diagnostic laboratory channels where procurement cycles favour certified vendors.

- Align pricing with evidence: use the report’s pricing sensitivity module to simulate reimbursement scenarios and protect margins against commoditization in high‑volume segments.

- Use M&A strategically: acquire niche assay IP or lab validation assets to accelerate market access rather than relying solely on organic rollouts; our M&A toolkit in the full report quantifies accretion scenarios.

How PW Consulting’s analysis supports deal teams and product leaders

For corporate development teams, the report contains valuation comparables, diligence checklists specific to ELISA reagent and kit businesses, and integration playbooks that quantify synergy levers. For product and commercialization teams, it supplies validation study templates, regulatory submission roadmaps and channel launch checklists that align with typical laboratory procurement timelines.

Importantly, the full dataset includes granular segmentation and an interactive financial model used to derive our forecasts. In this briefing we intentionally withhold core subsegment tables and exact split metrics to preserve model integrity and drive stakeholders to the full deliverable, where those datasets can be licensed or obtained with consulting support.

Next steps and access

Executives and investors preparing 2026 strategies will find the full Fertility ELISA Test Kit Market report immediately actionable. It pairs the high‑level forecasts cited here with the ground‑level segment data, competitor scorecards, regulatory timelines, and executable playbooks required to convert market insight into commercial outcomes.

To request the complete report, bespoke workshops or a custom model walk‑through, visit PW Consulting’s market research portal or contact our industry practice. The full report unlocks the segmented data tables, valuation models and primary interview transcripts omitted from this briefing under our “trailer” release approach.

PW Consulting — translating diagnostic market data into operational strategies for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Fertility Elisa Test Kit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com