Acids and Nutrients in Poultry Nutrition Market: Size, Share, and Future Growth

Other |

2026-04-13 04:08:06

PW Consulting’s latest Aircraft Interior Lighting Market report (base year 2025, forecast 2026–2032) provides a timely, decision-grade perspective for organizations that must convert lighting innovation into competitive advantage. The global market has expanded from roughly USD 1.03 billion in 2020 to USD 1.45 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 6.85% through our 2026–2032 forecast horizon. By 2026 PW Consulting estimates the market will exceed USD 1.54 billion and is set on an upward trajectory toward the USD 2.3+ billion range by 2032. These headline dynamics make 2026 a critical planning year for procurement, product roadmapping, retrofit strategies and M&A activity.

Aircraft Interior Lighting Market

Demand alignment: A combination of narrowbody fleet renewals, growing regional air traffic, and expanding business aviation deployments is increasing the addressable opportunity for cabin interior upgrades and new-build specifications. This demand is not uniform — it is driven by different timelines for OEM deliveries versus retrofit cycles — making scenario-based planning essential.

Aircraft Interior Lighting Market

Technology maturation: LED architectures have already displaced many legacy systems; OLED and advanced LED panel technologies are transitioning from demonstration to early adoption. These technologies deliver measurable benefits — energy efficiency, weight savings and service-life improvements (technical lifetimes often quoted in excess of 100,000 hours) — which directly affect operating costs and lifecycle economics.

Aircraft Interior Lighting Market

Human factors and passenger experience: Human‑centric lighting and chronobiology-aligned systems are moving from marketing differentiator to operational value, with airlines and OEMs prioritizing solutions that mitigate jet lag and enhance comfort during longer sectors.

Regulatory and certification pressures: EASA CS‑25, FAA TSO and SAE standards continue to define performance and safety baselines for cabin and emergency lighting. Certification timelines and test requirements are a key gating factor for market rollout and retrofit approvals.

Designed as a practical toolkit for 2026 decision-making, the report blends market science with hands-on operational guidance. Key deliverables include:

Robust market model and scenarios — top-line market sizing, growth trajectories and sensitivity analysis for a range of demand and price environments across our 2026–2032 forecast period.

Executive playbooks — procurement levers, retrofit prioritization matrices, and a supplier selection framework that translates product attributes (weight, power draw, CRI, maintainability, certification status) into TCO-led choices.

Technology adoption roadmap — comparative analysis of LED, OLED and hybrid systems, including lifecycle cost drivers, technology readiness levels and likely adoption windows by platform type.

Regulatory & certification matrix — mapping of EASA/FAA/SAE requirements, common certification bottlenecks and mitigations that compress time-to-entry.

Supplier benchmarking — qualitative and quantitative profiles of incumbent and emerging suppliers, capability heatmaps, and a go-to-market matrix for OEMs, MROs and retrofit specialists.

Financial tools — downloadable ROI and payback calculators for retrofit cases, plus scenario P&L and CAPEX planning aids that support board-level investment approval.

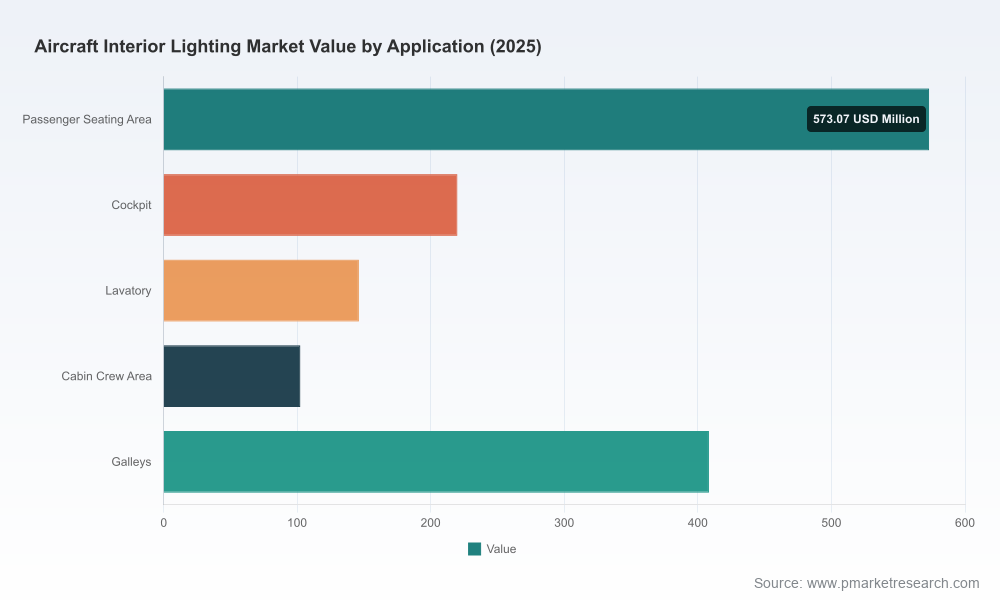

To preserve strategic value for subscribing clients, detailed breakdowns by region, application and type (the granular splits and node-level forecasts) remain accessible in the full report and associated data workbook.

The aircraft interior lighting market shows a moderate level of concentration: the top three suppliers account for a substantial portion of industry revenue, and the top five consolidate an even larger share. This structure creates a market where tier-1 incumbents, specialist integrators and nimble OEM partners each have distinct strategic roles. Our qualitative assessment of leading players highlights where capability and go-to-market strength sit today:

Collins Aerospace (RTX) — a broad-scope systems integrator with deep platform-level relationships across commercial, business and military segments. Strengths include comprehensive LED interior/exterior portfolios and advanced panel technologies that integrate into avionics and cabin management systems.

Diehl Aviation — long-tenured leader in cabin lighting with proven system-level integration for major OEM platforms. Their focus on human-centric and integrated cabin solutions keeps them close to OEM spec processes.

Safran Cabin — strong in high-CRI illumination and retrofit-friendly modules, with particular traction in galley and lavatory illumination where serviceability and compliance matter most.

Astronics Corporation — differentiation through passenger-experience lighting (ambient, Nuancia RGBW) and an emphasis on cross-platform compatibility for business and commercial markets.

STG Aerospace (Heads Up Technologies) — specialist in full LED cabin lighting and plug‑and‑play retrofit systems, with offerings aimed at compressing retrofit cycle time and STC complexity.

SCHOTT AG, Luminator Aerospace, Bruce Aerospace, Aircraft Lighting International and American Bright LED — together they represent an ecosystem of niche innovators and trusted suppliers focusing on decorative finishes, STC portfolios, PMA capabilities and customized module manufacturing.

Recent industry activity at trade shows and certification events (for example, product showcases at AIX 2026 and FAA approvals in late 2025) confirms two dynamics: suppliers continue to compete on lighting quality and human-centric features, while certification and retrofit readiness increasingly determine who wins airline retrofit programs.

LED remains the baseline for most new specifications and retrofits due to proven reliability, service life and operating cost advantages. Transitioning to advanced LEDs and OLED panels enables richer color control, lower power draw and new form-factors for cabin architecture.

Human-centric lighting — dynamic intensity and spectral tuning — is no longer experimental. Airlines are asking for systems that support wellness use cases and offer content management via cabin management systems; procurement teams must therefore evaluate not only hardware performance but software integration and data APIs.

Emergency and path-marking systems continue to be a compliance anchor. Photoluminescent and LED-based path solutions offer different certification profiles and lifecycle costs; optimal choices depend on platform mission and retrofit constraints.

Supply chain and materials: LED chips, driver electronics and specialized optics are sourcing constraints that can influence lead times and cost volatility. Buyers should evaluate multi-sourcing strategies and consider strategic inventory for long lead items.

Compliance with EASA CS‑25, FAA TSO and SAE standards is non‑negotiable. Certification complexity imposes calendar and cost exposure that directly affects procurement timing. For example, industry benchmarks indicate that a comprehensive LED upgrade package for a typical regional aircraft — including installation — can sit in the low tens of thousands of USD range for many operators (a ballpark that should be validated against platform-specific STC paths). Early engagement with certification authorities and inclusion of certification cost/time assumptions into business cases materially reduces program risk.

Prioritize retrofit-readiness in new specifications: insist on modular, STC-friendly designs and supplier collaboration on installation kits to shorten out-of-service time for MROs.

Lock in technology roadmaps with suppliers: negotiate milestone-based R&D commitments (controls, API exposure, firmware security) to protect future upgrade paths and ancillary revenue streams.

Embed certification into procurement contracts: allocate cost and schedule risk for certification explicitly and use staged payments tied to certification milestones.

Adopt scenario-based capital planning: use scenario models to test sensitivity to delivery delays, price erosion and differing retrofit penetration rates — PW Consulting’s financial tools are designed for exactly this use.

Consider horizontal consolidation for capability gaps: target acquisitions or JV partnerships to secure specialized optics, software or STC portfolios rather than building them from scratch.

For procurement leaders, OEM program managers and M&A teams, the full PW Consulting Aircraft Interior Lighting Market report provides the granular visibility required to translate the 2026 market opportunity into executable programs. Subscribers receive the full data workbook with regional and application-level breakdowns, detailed supplier scorecards, ROI calculators and a certification risk register. These materials are purpose-built to shorten decision cycles and reduce execution risk.

To access the complete report, interactive models and supplier benchmarking datasets, please visit the PW Consulting publication page for the Aircraft Interior Lighting Market report. The full package contains the granular splits, STC and PMA profiles, and platform-level retrofit case studies that we intentionally reserve for subscribers and licensed clients.

PW Consulting — advising leaders who must turn lighting innovation into strategic advantage.

For detailed analysis of this topic, please visit the official page:Aircraft Interior Lighting Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com