Understanding the Intrinsic and Monetary Value of the Geospatial Analytics Market

Other |

2026-06-30 07:29:04

PW Consulting’s latest market study on Zellweger Spectrum Disorders (ZSD) synthesizes clinical, commercial, and technology signals into a single, decision-ready framework for life sciences executives, payers, diagnostic providers, and specialty care organizations. In an environment where treatment options remain limited and cutting‑edge genetic approaches are rapidly maturing, our analysis translates macro trajectories into concrete strategic levers. The report’s baseline shows a market that expanded steadily through the first half of the decade and, using a 2025 base year, is projected to grow at a compound annual growth rate (CAGR) of 6.72% through 2032 — reflecting both incremental commercial expansion of existing adjunctive therapies and the disruptive potential of emerging genetic modalities.

Zellweger Spectrum Disorders Market

Historic momentum. From 2020 through 2025 the market demonstrated consistent expansion as diagnostic uptake improved and supportive care practices became more standardized. The market size rose from the low hundreds of millions (USD, revenue unit: Million) in 2020 to an estimated figure for 2025 that sets the base for our forward-looking modelling.

Zellweger Spectrum Disorders Market

Forward outlook. Our 2026–2032 forecast embeds a 6.72% CAGR that captures continued uptake of adjunctive therapies, increasing diagnosis rates through broader genetic testing access, and plausible near‑term adoption of advanced therapeutics in clinical development. By 2032 projected market value materially exceeds the 2025 base, reflecting both volume and value drivers.

Zellweger Spectrum Disorders Market

Strategic implication. A mid‑single-digit CAGR with notable upside from technology leaps (gene editing/gene therapy) creates an ideal planning horizon for platform investments, early payer engagement, and partnerships between diagnostics and therapeutics providers.

The ZSD landscape is characterized by a combination of entrenched supportive care paradigms and nascent disruptive science. Key contextual points that informed our analysis include:

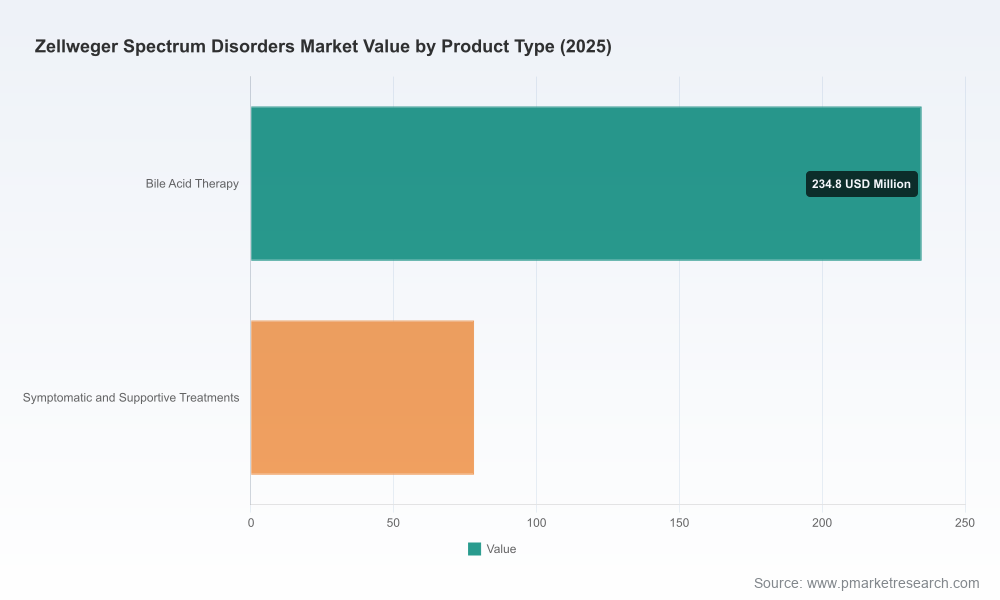

Treatment landscape: CHOLBAM (cholic acid) remains the only FDA‑approved adjunctive therapy addressing hepatic manifestations in eligible patients since its approval in 2015. Clinical guidance updates through 2025 have reaffirmed its role in managing liver disease manifestations, preserving its place in treatment pathways.

Unmet needs: There are currently no approved disease‑modifying therapies that correct the root peroxisome biogenesis defect or that have demonstrated efficacy across extra‑hepatic manifestations. This maintains a large addressable unmet need that attracts R&D and venture capital focus.

Diagnostics and patient identification: Wider availability of genetic panels and expanded newborn screening pilots are driving earlier diagnosis and care coordination. Diagnostic laboratories and platform vendors are therefore strategic gatekeepers for patient identification and trial recruitment.

Regulatory and reimbursement context: Reimbursement remains fragmented for supportive interventions, and payer strategies will be pivotal for high‑cost or one‑time therapies. Early payer dialogue and real‑world evidence generation are high‑priority tactical moves.

April 2026 — Preclinical gene editing: A high‑profile preclinical report demonstrated base editing correction of the common PEX1‑p.G843D mutation in a mouse model, restoring peroxisomal function and normalizing liver pathology while eliminating toxic metabolites. This result elevates the probability that mutation‑specific editing approaches advance to IND‑enabling studies sooner than previously anticipated.

January 2026 — Commercial momentum for CHOLBAM: The incumbent commercial provider reported continued growth for cholic acid in its labeled adjunctive indication, underscoring steady demand where hepatic manifestations are present.

November 2025 — Clinical guidance reaffirmation: Clinical guidelines and specialty references have reiterated cholic acid’s role as adjunctive therapy for liver manifestations, which supports persistent utilization as diagnostics find more affected individuals.

The segment is led by a mix of specialty pharmaceutical manufacturers, diagnostic laboratories, and platform suppliers. The strategic posture of these players influences market structure, access pathways, and partnership opportunities:

Specialty therapeutics: Mirum Pharmaceuticals (CHOLBAM) is the incumbent commercial presence for adjunctive hepatic therapy and serves as the de facto commercial benchmark for liver‑directed management in ZSD. Its trajectory provides a near‑term revenue reference and a commercial playbook for rare‑disease specialty products.

Genetic diagnostics: Companies such as Invitae and GeneDx are central to case ascertainment through targeted panels and exome‑based diagnostics. Their lab networks and payer contracting strategies materially influence diagnostic lead generation and trial recruitment timelines.

Platform suppliers and CRO/diagnostic partners: PerkinElmer, Thermo Fisher Scientific, and CENTOGENE provide instruments, reagents, and end‑to‑end diagnostic services that underpin testing scale‑up and quality assurance — critical for both clinical care and pivotal trials.

Strategic read: The market is concentrated among a limited set of specialized providers in both therapeutics and diagnostics, making targeted partnerships, licensing arrangements, and co‑development agreements high‑impact routes to market entry.

Our full report is designed as an operational toolkit for 2026 planning cycles. It contains:

Executive dashboards that translate macro projections into revenue scenarios under alternative adoption and pricing assumptions, enabling financial planning for pipeline products and commercial expansions.

Commercial playbooks for therapeutic incumbents and entrants, covering go‑to‑market sequencing, key opinion leader (KOL) engagement, specialty pharmacy strategies, and contracting levers for rare disease formularies.

Diagnostics integration roadmaps that align genomic testing scale‑up with clinical workflows, newborn screening pilots, and payer reimbursement pathways — including vendor selection criteria and lab network models.

Clinical development blueprints that outline practical designs for early‑phase gene editing and gene therapy studies, recommended biomarkers, surrogate endpoints for hepatic and extra‑hepatic outcomes, and registries to accelerate evidence generation.

Manufacturing and COGS sensitivity analyses that quantify how different production approaches (centralized viral vector manufacturing vs. emerging in‑house editing platforms) alter commercial economics and payer value propositions.

Stakeholder maps and patient journey analytics that identify friction points across diagnosis, referral, and long‑term management — with prioritized interventions to improve enrollment and adherence.

Prioritize diagnostics partnerships. Early identification is the linchpin of both supportive care optimization and trial recruitment. Therapeutic developers and payers should collaborate with leading genetic labs to create bundled testing pathways and case management pilots.

Develop phased payer engagement plans. For enterprise budgets, structure evidence generation around payer needs: short‑term real‑world outcomes for hepatic endpoints and longer‑term registries for extra‑hepatic effects. Value‑based contracts should be designed with clear, measurable hepatic and functional endpoints.

Hedge technology risk while funding innovation. Given the promising preclinical gene editing results, create flexible portfolio approaches that maintain investment in incremental improvements to supportive care while allocating discovery capital to mutation‑targeted and platform approaches.

Design registries and natural history studies now. A high‑quality, longitudinal data asset materially accelerates both regulatory discussions and payer acceptance. Cross‑industry consortia can be effective mechanisms to distribute cost and broaden data representativeness.

Plan manufacturing and commercial scalability concurrently. Prepare modular manufacturing pathways and specialty distribution strategies that can scale in step with clinical milestones to avoid supply bottlenecks and pricing pressure at launch.

Consistent with the “trailer” principle, this release surfaces the strategic implications and high‑level market metrics executives need to prioritize 2026 planning without disclosing sensitive segmentation tables and granular regional or product‑level figures that are reserved for our full report. The full analysis contains detailed country‑ and channel‑level forecasts, payer mixes, and modeled uptake curves for multiple launch scenarios — essential inputs for tactical budget allocation and partnership negotiations.

For boards, corporate development teams, and strategy functions preparing 2026 budgets and pipeline prioritization, the PW Consulting Zellweger Spectrum Disorders Market report is engineered to move you from hypothesis to executable plan. The full report includes the proprietary segmentation, modeled scenarios, and playbooks referenced here — available through our report portal. Contact PW Consulting to schedule a briefing or to obtain the detailed market model and tailored advisory engagements.

For detailed analysis of this topic, please visit the official page:Zellweger Spectrum Disorders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com