Calcium Gluconate Market in Japan to Achieve USD 6.43 Billion by 2036

Food |

2026-04-24 16:49:59

PW Consulting’s new Macrocell Baseband Unit Market report (base year 2025) delivers an evidence-driven, decision-ready roadmap for executives preparing capital, vendor, and technology strategies for 2026 and beyond. Drawing on an analysis of historical performance (2020–2025) and a detailed forecast through 2032, the study shows the market expanding at a steady compound annual growth rate (CAGR) of 5.23%. Total market revenue, measured in USD Million, rose from a multi-billion base in 2020 to approximately USD 9,720 Million in 2025 and is forecast to reach roughly USD 13,900 Million by 2032—figures that materially affect procurement timing, architecture choices, and partner selection.

Macrocell Baseband Unit Market

Macrocell baseband units remain the backbone of outdoor cellular coverage. The next 18–36 months will determine which operators and vendors capture the high-value macro upgrades tied to 5G-Advanced, spectrum refarming and macro densification. Our report translates market momentum into operational implications: where to accelerate capex, when to pilot cloud-native topologies, and how to mitigate regulatory and supply-chain risks that can compress availability windows and erode margin.

Macrocell Baseband Unit Market

Historical context: The market demonstrates resilient expansion across the 2020–2025 period, reflecting major macrocell refresh cycles, 5G rollouts and early 5G-Advanced pilots.

Macrocell Baseband Unit Market

Near-term inflection: The market is forecast to rise in 2026 (base year-adjusted projection) as operators convert pilot programs into commercial macrocell upgrades and mid-band spectrum allocations come online.

Medium-term runway: From 2026 through 2032, PW Consulting projects the market to grow at a 5.23% CAGR, reaching the low tens of billions (USD Million units aggregated) by 2032—implying sustained procurement opportunities and continuous product evolution.

Technology drivers: 3GPP Release 18 crystallizes enhancements for 5G-Advanced baseband processing, accelerating demand for units that support advanced massive MIMO, enhanced carrier aggregation and tighter cloud integration. Operators that delay migration risk falling behind on spectral efficiency and latency-sensitive services.

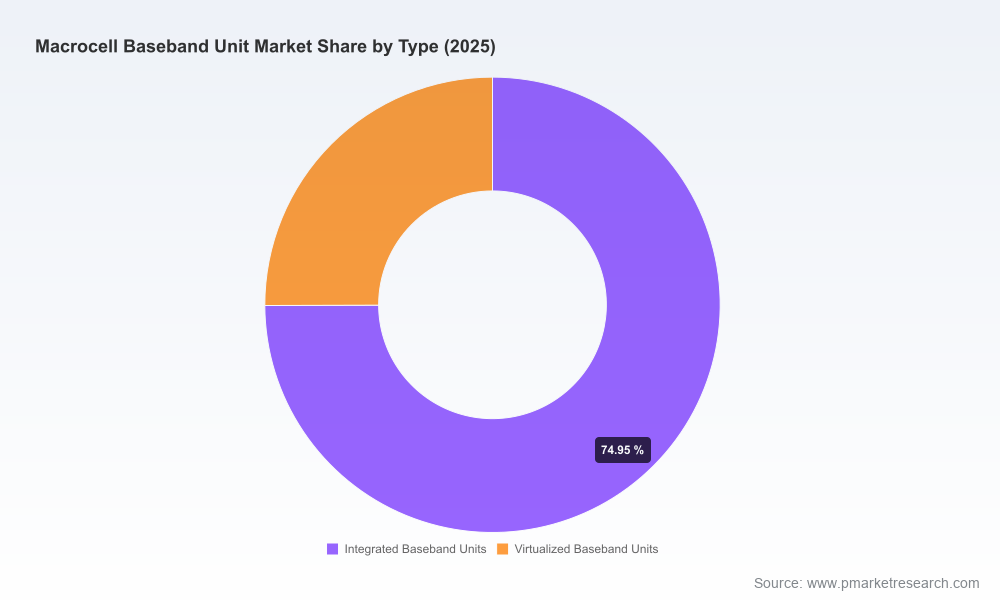

Architecture shift: The debate between fully integrated hardware platforms and cloud-native / virtualized basebands is now operationally consequential. Virtualized approaches promise operational elasticity and software-driven feature velocity; integrated solutions still deliver deterministic performance for high-capacity macrocell deployments. Procurement teams must balance lifecycle TCO against service velocity and integration risk.

Spectrum and deployment economics: Recent mid-band spectrum allocations are creating fresh macrocell capacity needs. However, macro upgrades require coordinated investments in fronthaul fiber and RRU integration and, for many operators, a multiyear site preparatory program that should be budgeted in advance.

Regulatory & trade risk: Export controls and entity-list actions affecting certain suppliers introduce sourcing constraints in specific markets. Commercial planners must layer geopolitical / compliance scenarios into vendor roadmaps and contingency inventory strategies.

Market concentration: The macrocell baseband sector is highly concentrated. A small number of global suppliers capture the majority of market share—an oligopolistic structure that affects pricing dynamics, innovation pacing and the predictability of supply for large-scale rollouts.

Nokia (Espoo, Finland) — Nokia’s AirScale family has evolved toward cloud-native baseband offerings designed for massive MIMO and 5G macro deployments. Recent product launches emphasize software modularity and hybrid cloud deployment models, making Nokia a natural partner for operators pursuing phased cloud migration strategies.

Ericsson (Stockholm, Sweden) — Ericsson’s macro baseband portfolio, with models purpose-built for high-capacity sites, is increasingly field-proven in large operator trials, including Open RAN experiments. Ericsson’s deployments demonstrate a pragmatic balance between performance for standalone 5G and spectrum-sharing operations.

Huawei (Shenzhen, China) — Huawei remains technologically aggressive on hardware performance and integrated AAU-BBU architectures that optimize spectral efficiency. In markets where regulatory and export constraints are manageable, Huawei’s product performance continues to pressure incumbents on price/performance.

ZTE (Shenzhen, China) — ZTE’s virtualized RAN-capable basebands target rapid feature upgrades and operator automation strategies; however, export controls and geopolitical sensitivities complicate ZTE’s access in certain operator portfolios, necessitating careful vendor risk assessment.

Samsung Networks (Suwon, South Korea) — Samsung offers distributed baseband and vCore approaches with an emphasis on Open RAN compatibility. Their position is particularly relevant for operators prioritizing multi-vendor interoperability and cloud-native workflows.

Notable recent developments—product launches and trial deployments in late 2024 and early 2025—signal vendor priorities. These moves underscore rapid productization for 5G-Advanced capabilities and real-world testing in Open RAN contexts. For procurement teams, this means shorter windows between prototype validation and commercial availability, pressuring decision timelines.

Proprietary market model: Annualized revenue model (USD Million) across the 2020–2032 horizon with sensitivity scenarios for accelerated spectrum deployment and regulatory friction.

Vendor decision playbook: Side-by-side capability maps, maturity matrices and vendor risk profiles tailored to macrocell procurement tiers (high-capacity urban cores, suburban aggregators, rural coverage).

Deployment cost framework: A modular cost model that quantifies material line-items, OPEX implications of virtualized vs. integrated architectures, and break-even timelines for cloud migrations—designed to be dropped into financial planning cycles.

RD&E and roadmap tracker: Feature roadmaps mapped to 3GPP releases and OTA timelines, enabling CTOs and R&D leaders to prioritize interoperability investments and lab-to-field test sequences.

Scenario playbooks: Actionable contingency plans for supply disruption, export-control escalation, and accelerated densification—complete with procurement triggers and contract clauses to protect schedule and margin.

Align procurement cadence to forecasted capacity inflection points. With the market expanding into 2026, procurement teams should sequence commitments to capture falling unit costs while retaining flexibility to pivot to cloud-native deployments.

Define a hybrid architecture strategy. Operators should adopt a two-track approach: protect deterministic integrated solutions for the highest-capacity macro sites while accelerating virtualization pilots where operational agility yields the greatest commercial upside.

Harden supplier diversification. Given the sector’s concentration and export-control dynamics, operators and OEMs should institutionalize redundant sourcing lanes, dual-qualified SKUs and escrowed software arrangements to avoid single-point failures.

Embed regulatory scenario planning into capital approval. Spectrum allocations and regional compliance regimes materially affect go-to-market timing; CFOs should require scenario-adjusted ROI models before capital deployment.

Accelerate field trials that validate interoperability. Open RAN and multi-vendor macrocell deployments reduce vendor lock-in but shift risk to systems integration and orchestration—areas where targeted trials reduce commercial roll-out risk.

Market realism: Our revenue projections and CAGR (5.23%) are grounded in operator capex plans, spectrum availability schedules and empirical field trial data—providing a defensible baseline for budget approvals.

Vendor-neutral playbooks: We synthesize technology readiness and geopolitical exposure into a single decision framework so procurement and network chiefs can execute with fewer surprises.

Execution templates: From RFQ language to test acceptance criteria and contingency procurement triggers, the report includes reusable templates that shorten procurement cycles and strengthen contractual protections.

In keeping with our “trailer” approach, this briefing surfaces the most consequential findings and strategic implications while omitting the granular regional and application segmentation tables and site-level cost line-items that live in the full report. That level of granularity—detailed regional splits, application-specific revenue breakdowns, and line-item site cost schedules—is essential for transactional procurement and site-by-site rollouts and is available in the full dataset and model.

CTOs and network strategy leads: Request the Vendor Decision Playbook and Scenario Playbooks to immediately inform 2026 lab and pilot budgets.

CFOs and procurement chiefs: Acquire the full financial model to run internal TCO and capex sensitivity scenarios aligned to your vendor mix and regulatory exposure.

Program managers: Use our deployment cost framework and acceptance-test templates to accelerate site commissioning and reduce integration rework.

PW Consulting’s Macrocell Baseband Unit Market report provides the empirical backbone and operational toolset to make 2026 a year of decisive, low-regret investment. For access to the full dataset, regional and application segmentation, and plug-and-play procurement templates, please visit the report landing page on our website to request the complete report package and model files.

For detailed analysis of this topic, please visit the official page:Macrocell Baseband Unit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com