Regional Healthcare and Microelectronics Hubs: Meeting Robust North American Demand for Functional Nanomaterials

Other |

2026-06-17 09:03:40

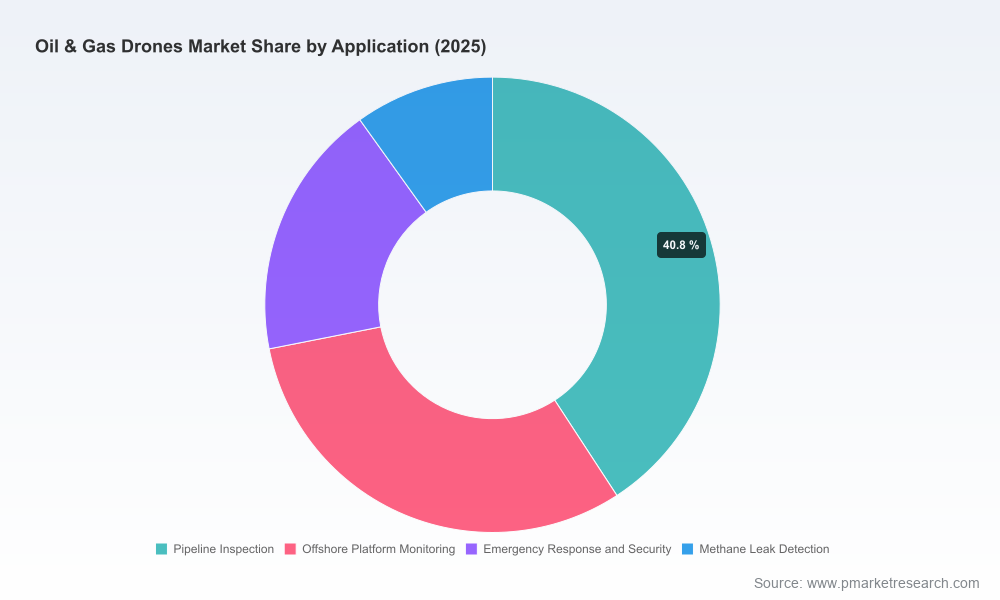

The unmanned aerial systems (UAS) ecosystem serving oil & gas operations is no longer a niche adjunct — it is a core operational lever. Our PW Consulting Oil & Gas Drones Market report (base year 2025) synthesizes market sizing, technology trajectories, regulatory inflection points, and actionable deployment frameworks needed to make high-confidence capital and operational decisions in 2026. At a macro level the market has accelerated from a mid-four‑figure base in 2020 to an estimated USD Million-scale market in 2025 and, driven by adoption of advanced sensing, autonomy, and regulatory acceptance, is forecast to grow at a 19.12% CAGR through the 2026–2032 horizon. By 2032 the market reaches a markedly larger scale, underscoring both the speed of adoption and the size of the opportunity for incumbents, service providers, and integrated energy operators.

Oil Gas Drones Market

Investment timing: The market’s sustained near‑20% CAGR signals that 2026 is a pivotal year to move from pilot programs to scaled deployments for operations seeking cost-to-risk optimization.

Oil Gas Drones Market

Procurement and vendor strategy: Market concentration is relatively low (top-three and top-five shares indicate fragmentation), meaning competitive procurement, strategic partnerships, or targeted M&A can rapidly change a buyer’s operating position.

Oil Gas Drones Market

Regulatory-readiness: Recent regulatory shifts create both runway and constraints. Companies that align procurement, operations, and compliance in Q1–Q2 2026 will gain decisive operational runway.

Our topline sizing shows a rapid expansion from 2020 through 2025, with continued acceleration into the forecast window. This scale-up is driven by three intersecting vectors: the maturation of sensor payloads (thermal, LiDAR, gas sensing), increased autonomy and data analytics capabilities, and regulatory acceptance of UAS for core pipeline and facility tasks. For strategic planners, the arithmetic is simple: organizations that establish standards, data pipelines, and contracting frameworks early will capture disproportionate operational and cost benefits as fleet utilization ratchets up.

Operational playbooks: Step-by-step guides for converting pilots into ongoing operations — including BVLOS considerations, asset access protocols, and integration with SCADA and asset integrity workflows.

Procurement and technology evaluation frameworks: A scoring matrix that compares airframes, sensor suites, autonomy stacks, maintenance models, and total cost of ownership across use case archetypes.

Regulatory compliance roadmaps: Region-agnostic templates for meeting new PHMSA/FAA guidance, hazardous materials transport by UAS, and mitigation strategies for jurisdictional restrictions on certain OEMs.

Data and analytics integration templates: Best practices for ingestion, labeling, anomaly detection, and actioning of aerial-derived datasets into existing asset integrity programs.

Risk, insurance, and safety modules: Practical checklists and scenario-based risk registers to support insurance underwriting and internal acceptance of UAS operations near high-consequence assets.

Commercial models and ROI tools: Sensitivity-tested financial templates that let operators model TCO, downtime avoidance, and incident mitigation value across conservative and aggressive adoption curves.

Vendor due-diligence packs and RFP templates: Ready-to-use scopes of work and evaluation criteria to accelerate vendor selection while protecting intellectual property, data sovereignty, and security requirements.

Short‑term (0–90 days): Establish governance. Create an executive-level UAS steering committee that aligns procurement, operations, legal, and cybersecurity; launch a compliance gap assessment against the latest PHMSA and FAA guidance; and prioritize pilots that demonstrate direct expense avoidance or safety improvement within 6 months.

Medium term (3–12 months): Standardize data and ops. Adopt the report’s data ingestion and anomaly-detection templates to ensure aerial data can be operationalized. Lock in multi-year service agreements with clauses that manage vendor risk (e.g., alternate suppliers, spares pools, and domestic provisioning where jurisdictional restrictions apply).

Strategic (12–24 months): Scale via modular architecture. Move to a mixed-architecture deployment that combines long-endurance fixed‑wing for wide-area pipeline monitoring, multirotor for detailed facility inspections, and specialized indoor/collision‑tolerant platforms for confined-space work. Use competitive procurement informed by the report’s vendor matrix to negotiate performance- and outcome-based contracts.

The sector includes a mix of OEMs, service specialists, and analytics platforms. Our report provides a comparative lens on capability sets so buyers can choose partners for immediate operational readiness versus long-term strategic advantage. Highlights:

DJI Enterprise (https://www.dji.com) — Strength in industrial-grade multirotor platforms and a broad payload ecosystem (thermal, gas sensing, LiDAR). Best for organizations prioritizing broad sensor availability and a mature supply chain, but procurement teams must assess jurisdictional and federal funding restrictions in their markets.

Flyability (https://www.flyability.com) — Leader in collision-tolerant indoor inspection platforms suitable for confined-space tank and vessel inspection; valuable for refineries and downstream facilities where internal access is constrained.

Terra Drone (https://terra-drone.net) — Global services footprint with strong LiDAR and thermal survey capabilities; well-suited for large-scale pipeline and remote infrastructure surveying.

Cyberhawk Innovations (https://www.cyberhawk.com) — Service-led model pairing inspections with analytics; strong in offshore platform and flare stack inspection regimes.

AeroVironment (https://www.avinc.com) and Insitu (https://www.insitu.com) — Providers of rugged tactical UAS and long-endurance platforms for remote or harsh environments; attractive where mission endurance is critical.

Delair (https://www.delair.aero) and Microdrones (https://www.microdrones.com) — Fixed-wing and LiDAR specialists enabling long-range pipeline mapping and volumetric analysis.

Skydio (https://www.skydio.com), Acecore Technologies (https://acecoretechnologies.com), ZIYAN UAS (https://www.ziyanuas.com) — Emerging leaders in autonomy, modular industrial platforms, and helicopter-style solutions respectively — each offers differentiated approaches to autonomy, ruggedization, and AI-assisted operations.

PrecisionHawk (https://www.precisionhawk.com) — Combines hardware, software, and analytics for integrated aerial data programs and is often selected by operators seeking an end-to-end stack.

Policy shifts: PHMSA and FAA guidance released in late 2025 and early 2026 formally integrates remote sensing and addresses hazardous materials transport by UAS — creating new authorized use-cases but also new compliance obligations.

Jurisdictional constraints: Restrictions on the use of systems from covered foreign entities for federally funded projects require contingency planning and potential vendor diversification for organizations operating in constrained procurement environments.

State‑level restrictions and local statutes may further limit operations around critical infrastructure; a robust compliance layer and legal review are non‑negotiable prior to scaling.

Operational limits: Environmental factors (offshore weather, GPS-denied environments, RF interference), payload endurance trade-offs, and insurance coverage terms remain practical constraints that must be modeled into fleet sizing and O&M budgeting.

Given the market’s fragmentation (top provider shares are modest), buyers have leverage: design procurement to include dual‑sourcing, onshore spare pools, and performance SLAs that align payments to measurable outcomes (e.g., hazard detection rate improvements, downtime avoided). For suppliers and investors, partnership ecosystems — combining platform OEMs, analytics providers, and local service integrators — are the most efficient path to capture large, geographically dispersed contracts while managing geopolitical and regulatory risk.

For CFOs: Use the ROI and sensitivity models in the report to translate operational pilots into capital requests with scenario-based returns that account for regulatory risk and procurement contingencies.

For Heads of Operations: Adopt the deployment and data-integration playbooks to accelerate time-to-value and ensure aerial data feeds actionable maintenance workflows.

For Corporate Development: Use the competitive mapping and fragmentation analysis to prioritize M&A targets or strategic investments that fill capability gaps (e.g., autonomy, gas sensing, analytics).

Our full report includes the datasets, segmentation granularity, vendor scorecards, and procurement templates necessary to act with confidence. This release is intentionally a high-fidelity preview: it demonstrates our methodology, market sizing trajectory, regulatory synthesis, and practical playbooks while reserving the full segment-level data and proprietary scoring outputs for report access. For teams preparing 2026 budgets, procurement timelines, or M&A screens, the report is a practical toolkit and decision-support engine.

Executives and program leads planning allocations or pilots in 2026 should prioritize a short diagnostic (we provide a 48-hour readiness assessment) that maps current capabilities to regulatory windows and supplier risk. To access the full dataset, vendor matrices, and executable playbooks, visit the PW Consulting report portal and schedule a briefing. The window to establish operational leadership in this rapidly expanding market is narrow — the organizations that translate insight into disciplined execution in 2026 will realize outsized benefits as the market scales.

For detailed analysis of this topic, please visit the official page:Oil Gas Drones Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com