Chennai Nightlife: Experience the City's Exciting Evening Culture

Other |

2026-06-13 18:18:00

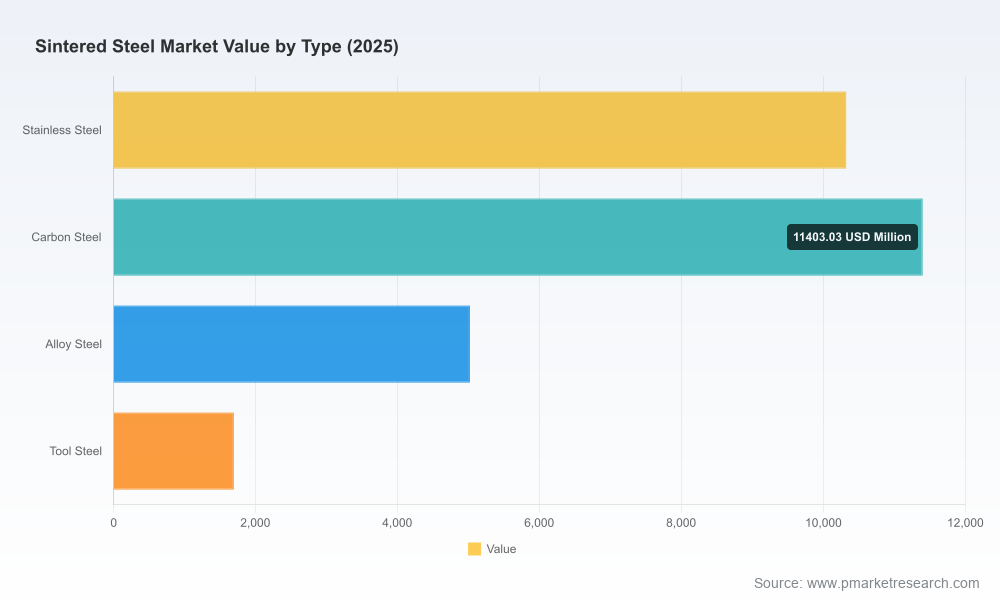

As companies finalize strategic plans for 2026, the sintered steel value chain is transitioning from incremental optimization to decisive repositioning. PW Consulting’s latest market study — covering 2020–2025 historicals and a 2026–2032 forecast horizon — synthesizes market dynamics, supplier moves, regulatory inflection points and cost trajectories into a decision-grade playbook. The global sintered steel market, which stood at approximately USD 28.45 billion in 2025, is projected to expand at a compound annual growth rate (CAGR) of 5.39% through the forecast period, reaching just over USD 41 billion by 2032. This brief highlights the report’s strategic value for corporate leaders while intentionally withholding granular sub-segment figures to preserve the report’s role as the definitive primary source.

Sintered Steel Market

Timing: 2026 is a pivot year. Early adopters of optimized material mixes, network reconfiguration and targeted capacity investments will capture outsized margin and share gains as demand from electrification and industrial automation accelerates.

Sintered Steel Market

Action focus: The report translates market growth into precise decision levers — where to allocate capex, which supply relationships to fortify, how to structure hedges against raw-material shocks, and which product-platform bets to prioritize for new mobility and industrial use-cases.

Sintered Steel Market

Risk-managed forecasting: Beyond headline growth, the study offers scenario-driven forecasts incorporating commodity volatility, tariff regimes and regulatory tightening — enabling boards and CFOs to stress-test investment plans.

PW Consulting’s study is designed for immediate operationalization. Key deliverables included in the full report are:

Market sizing and validated topline forecasts (2026–2032) with scenario pathways reflecting low-, base- and high-growth outcomes tied to EV adoption, industrial demand cycles and additive manufacturing uptake.

Cost-to-serve and landed-cost models that capture iron powder feedstock dynamics, sintering throughput economics, energy and labor differentials across production locations — modeled to inform offshoring vs. nearshoring choices.

Competitive heat maps and supplier capability matrices that profile technology positioning (e.g., soft magnetic composites, high-strength powders, binder-jet feedstock) to inform M&A, JV and supplier-development strategies.

Regulatory and compliance playbook mapping the implications of recent chemical and trade policy shifts for product formulation, export compliance and manufacturing certification timelines.

Go-to-market playbooks tailored to OEMs, tier-1s and industrial customers — including pricing strategy, innovation roadmaps and co-development contracting templates.

Transaction advisory support: target screening, valuation sensitivities, and integration checklists linking powder metallurgy assets to broader drivetrain, motor and structural component portfolios.

The sintered steel sector exhibits moderate concentration. The top three firms control a meaningful share of manufacture and technology leadership, and the top five players collectively command just under half of the market. This structure creates both opportunity and constraint: high barriers for pure greenfield entrants, yet attractive consolidation and bolt-on opportunities for established players seeking capability extension into powder development, soft magnetic solutions and additive manufacturing.

Our competitive analysis synthesizes public disclosures, capability mapping and primary interviews. Highlights for C-suite consideration:

GKN Powder Metallurgy (Bonn, Germany) — A global leader focused on sintered steel components for powertrain and structural applications. Recent capacity expansion in North America signals an aggressive push to capture EV drivetrain volumes. Strategic implication: partners and competitors should reassess North American supply capacity assumptions and evaluate local sourcing strategies.

Hoeganaes Corporation (Bala Cynwyd, PA, USA) — A leading atomized powder supplier with a recent product launch emphasizing higher fatigue resistance for automotive parts. Strategic implication: downstream manufacturers should update material qualification roadmaps to leverage improved powder grades.

Hoganas AB (Hoganas, Sweden) — Focused on high-performance powders and soft magnetic composites; recently introduced a new series aimed at high-efficiency electric motors. Strategic implication: motor OEMs and component suppliers must evaluate electromagnetic performance trade-offs and supply diversification.

Sumitomo Electric Industries (Osaka, Japan) and Mitsubishi Materials Corporation (Tokyo, Japan) — Both bring vertically integrated powder metallurgy capabilities with deep ties to automotive OEMs in Asia, representing attractive partners for co-development in shock absorbers, gears and bearings.

Hitachi Powdered Metals (Chiba, Japan) — Specializes in transmission components, presenting a strong OEM affinity for precision, high-reliability parts.

Porite Taiwan (Taoyuan, Taiwan) — A precision parts manufacturer in Asia with relevance for power tools and appliances; noteworthy for operational agility in high-mix, lower-volume segments.

Bound Metal Powders (Burton, MI, USA) — Represents the additive-manufacturing frontier with binder-jet feedstock development for stainless and specialty alloys; a bellwether for digital-manufacturing economics.

Collectively, these players illustrate two concurrent trends: consolidation around scale and deep materials expertise, and a parallel proliferation of niche, high-performance powder and additive-manufacturing specialists. Strategic buyers should use a bifurcated M&A lens — scale acquisitions to secure volume and regional footprint, and bolt-ons to acquire technical differentiation.

Raw material volatility: Iron powder prices have seen marked upward pressure recently due to supply-chain disruptions. Companies must integrate commodity hedging and alternative sourcing scenarios into procurement strategies to protect margins.

Regulatory tightening: New regulatory requirements in major markets have raised impurity limits and registration obligations for nickel-containing powders. Compliance timelines will affect product launch schedules and regional product formulations.

Trade policy: Persisting tariffs in certain jurisdictions continue to influence calculus on local production vs. import dependency for sintered components — a critical factor for total-cost-of-ownership analyses.

Labor and cost differentials: Rising labor costs in developed metalworking hubs are accelerating automation and nearshoring economics. Firms need to quantify the trade-off between wage inflation and capital intensity in factory modernization plans.

Technology shift: Advances in binder-jet powders and soft magnetic composites are unlocking new design paradigms for motors and compact drivetrains; first-mover adoption can yield system-level advantages for OEMs.

Rebase procurement strategies: Move from transactional sourcing to strategic partnerships with powder suppliers; lock in development roadmaps and dual-source critical feedstocks.

Invest selectively in capacity: Prioritize modular, flexible capacity that can switch between grades and parts to manage demand uncertainty and tariff exposures.

Double down on material R&D: Co-invest with suppliers on next-generation powders (soft magnetic composites, high-strength sintered powders) to secure IP and shorten qualification cycles with OEMs.

Stress-test M&A opportunities: Evaluate targets for either regional scale or technical differentiation; use the report’s valuation sensitivities to set realistic bid ranges.

Embed regulatory compliance: Integrate chemical registration and impurity management into product development lifecycles to avoid market access delays in key geographies.

The full study is more than an analytical dossier — it is an implementation toolkit. Subscribers receive dynamic models, supplier scorecards, contract templates and scenario scripts that can be used directly in board reviews, procurement negotiations and integration planning. For private equity and corporate development teams, the report provides bespoke screening criteria and synergy calculators tailored to sintered-steel adjacencies.

Given the accelerating pace of change in 2026, the value of timely, validated intelligence cannot be overstated. PW Consulting’s sintered steel market study pairs rigorous forecasting with execution-oriented tools designed to reduce time-to-decision and increase deal certainty. For companies seeking the full dataset, segmented market tables, and proprietary models (including sensitivity analyses on powder price and tariff scenarios), please consult the report landing page for subscription and licensing options.

Note: This executive brief is intentionally high-level. Detailed regional and application breakdowns, unit economics, and company-level financial assessments are available exclusively in the full report.

For detailed analysis of this topic, please visit the official page:Sintered Steel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com