Silica Gel Orange Desiccant Market 2026: A Strategic Preview for Decision-Makers

PW Consulting’s latest market research—Silica Gel Orange Desiccant Market: Strategic Outlook 2026—offers senior executives, product chiefs, and supply-chain leaders a concise, actionable intelligence brief as they set strategies for the year ahead. This preview distills the report’s analytical backbone, exposes the structural forces reshaping the market, and highlights competitive inflection points—while intentionally withholding the granular segment tables reserved for the full report.

Silica Gel Orange Desiccant Market

Executive snapshot: Why this market matters in 2026

The global silica gel orange desiccant market has evolved from a niche indicating product into a mainstream moisture-control material across industrial packaging, healthcare logistics, and electronics protection. After expanding from an estimated market base in 2020 to an overall market value of roughly USD 146.6 Million in 2025, our modelling points to an accelerating trajectory in 2026 with an initial-year market value near USD 154.7 Million. Over the forecast window to 2032, the market is projected to grow at a compound annual growth rate (CAGR) of approximately 5.12%, reaching a projected size north of USD 207 Million by 2032.

Silica Gel Orange Desiccant Market

For 2026 planning cycles, this data means two practical realities for corporate leaders: first, growth is steady and predictable—enough to justify near-term investments in production scale, new eco-formulations, and targeted channel expansion; second, the market is far from winner-take-all—concentration metrics indicate a fragmented supplier base, leaving room for ambitious mid-size players and innovators to capture meaningful share.

Silica Gel Orange Desiccant Market

What the research brings to your 2026 decision playbook

- Validated demand curves and scenario modelling calibrated to recent shocks and supply constraints—enabling finance teams to align CAPEX timing with realistic upside and downside cases.

- Supply-chain risk maps linking feedstock inflation, regional logistics nodes, and contract exposure—translating price volatility into procurement playbooks for raw materials and reactivation strategies for idle capacity.

- Regulatory and product-compliance pathways that de‑risk product launches into sensitive channels such as food and pharmaceuticals—crucial for companies aiming to upgrade to cobalt-free indicating formulations.

- Competitor playbooks synthesizing product portfolios, distribution footprints, and innovation moves—allowing commercial teams to construct targeted countermeasures or partnership strategies.

- An execution-ready go-to-market checklist: sample commercial propositions, testing protocols for indicating performance, and short-list vendor selection criteria for B2B procurement.

Market dynamics and pressure points

Three structural dynamics will dominate executive attention in 2026:

- Feedstock economics: Sodium silicate remains the primary precursor for silica gel. Recent industry pricing signals show upward pressure year‑on‑year with incremental monthly movements, making raw material procurement and hedging policies operational priorities. Procurement teams should expect continued sensitivity to soda ash and silica sand cost cycles and adopt flexible sourcing strategies.

- Regulatory and formulation shifts: The sector continues a notable move toward cobalt-free orange indicating formulations. This change is driven by tighter regulatory scrutiny of hazardous indicators and stronger buyer preference for non-toxic, recyclable desiccants in food, pharma, and healthcare packaging. Manufacturers that certify cobalt-free, non-toxic product lines gain accelerated access to regulated channels and premium contracts.

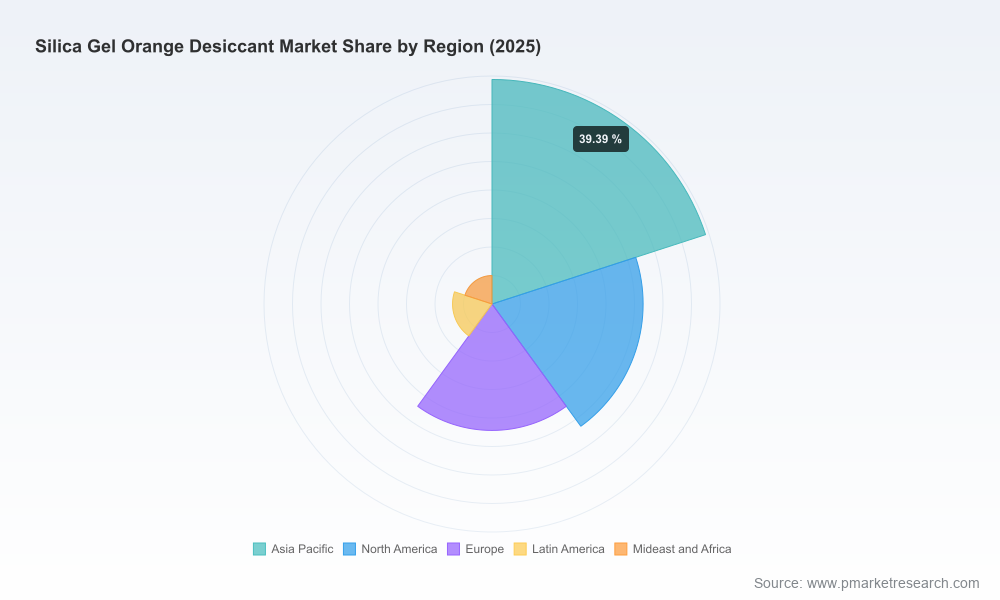

- Fragmented competitive structure: Market concentration is low—three leading suppliers account for a modest share of global revenues, and the top five remain under 30% combined. This fragmentation creates strategic opportunity: acquisition and alliance activity can rapidly uplift market share for disciplined acquirers, while innovators can scale through contract manufacturing and branded premium offerings.

Supply chain intelligence: what you need to know now

Beyond headline growth figures, the report maps supply-chain chokepoints and cost levers in operational detail. Key takeaways:

- Sourcing flexibility for sodium silicate and related chemicals reduces exposure to regional cost inflections. Firms with diversified buyers or backward-integration options demonstrate better margin resilience in our scenarios.

- Processing footprint decisions (bead vs. granular production lines, indicating vs. non‑indicating formulations) materially affect capital intensity and margin profiles. Our modelling quantifies payback thresholds for common retrofit investments, allowing CFOs to test investment cases for 12- to 24-month horizons.

- Packaging and logistics are non-trivial value levers—reductions in dust, crush rates, and contamination translate into fewer returns and higher acceptance rates in sensitive end-markets (electronics, pharmaceuticals). Operational roadmaps in the full report outline quick wins and KPI targets.

Competitive landscape: who to watch and why

The silica gel orange market comprises a mix of long-established regional manufacturers, specialized suppliers, and vertically integrated chemical players. Our comparative analysis evaluates product attributes (indicator chemistry, adsorption capacity, crush strength), certifications (food‑contact, pharma‑grade), and go‑to‑market models (OEM supply, branded retail, converter partnerships).

- Sorbchem India: A legacy producer with multi-decade experience in orange indicating beads. Strengths include scale in bulk supply and a global OEM footprint—an attractive partner for firms needing consistent industrial volumes and established logistics.

- Aharnish Desiccant: Positions as a premium global supplier focused on high-performance indicating variants, appealing to customers that prioritize capacity and consistency over cost alone.

- AGM Container Controls: U.S.-based supplier that emphasizes non-toxic, environmentally conscious products for the packaging and container markets—well-placed for North American healthcare and electronics channels.

- DryCon and Innoveda Chemicals: Global suppliers offering high adsorption, indicating beads—their advantage lies in supply flexibility for multi-regional customers.

- Baltimore Innovations and Wisesorbent Technology: Both emphasize advanced indicator formats and rechargeable/reusable products—relevant where lifecycle cost and sustainability commitments are procurement priorities.

- DryTec Industries, Best Silica Gel Packaging, Cilicant, and Sorbstar: Regional players with OEM strength and export capabilities—key acquisition or contract-manufacturing candidates for firms seeking incremental capacity or cost arbitrage.

Recent vendor moves underscore the competitive thrust towards environmentally safer chemistries and market positioning in healthcare packaging. Notable industry events in the past 18 months include a major producer launching recyclable orange silica gel that eliminates cobalt compounds, and regional suppliers promoting cobalt-free, SGS-tested formulations tailored for regulated end-markets. These product initiatives materially shift procurement criteria and open premium pricing bands for compliant products.

Where the value sits: practical scenarios for 2026

Our scenario analysis presents three actionable pathways for market participants planning 2026 initiatives:

- Scale-and-optimize (for incumbent producers): Invest selectively in capacity expansion where existing line utilization can be raised with incremental capital. Emphasize improvements in crush strength and dust control to win large tendered contracts.

- Product-upgrade and certification (for challenger brands): Prioritize cobalt-free, recyclable formulations and obtain pharma/food-contact certifications to access higher-margin channels. Marketing and traceability become differentiators.

- Consolidation and partnerships (for financial sponsors and private equity): Leverage the fragmented landscape to build regional platforms through bolt-on acquisitions and shared logistics. Margins can be improved by centralizing procurement for sodium silicate and standardizing QA protocols.

Report contents—what you will get if you read the full study

The full PW Consulting report delivers:

- Comprehensive market sizing (historical 2020–2025, base 2025) and detailed forecast model (2026–2032) with scenario toggles.

- Supply-chain and cost-model templates, including sensitivity analyses for raw material price movements and logistics disruptions.

- Regulatory risk mapping, product compliance checklists, and an adoption roadmap for cobalt-free indicating chemistries.

- Commercial playbooks: RFP templates, specification language for indicating desiccants, procurement scorecards, and distributor evaluation matrices.

- Company profiles and benchmarking for the leading manufacturers, including product strengths, footprint, and recent strategic moves—with a clear view of M&A targets and licensing opportunities.

How to use this intelligence in Q1–Q2 2026

- Procurement: Reassess supplier contracts and build flexible sourcing clauses tied to sodium silicate index movements. Consider small strategic buffer inventories where lead-time risk is highest.

- R&D and Product: Accelerate testing and certification of cobalt-free formulations if not already underway. Prioritize performance validation for high-value channels (pharma, electronics).

- M&A and Corporate Development: Use the fragmentation data to target complementary regional manufacturers and convert operational synergies into near-term margin gains.

- Sales and Marketing: Reframe customer conversations around lifecycle cost and safety credentials; highlight certified non-toxic and recyclable options as a premium differentiator.

Conclusion and next steps

For decision-makers mapping 2026 priorities, the silica gel orange desiccant market presents a blend of steady growth and strategic opportunity. The sector’s predictable growth trajectory—backed by the 2025 baseline and a mid-single-digit CAGR into 2032—combined with a fragmented supplier landscape and regulatory momentum toward cobalt-free chemistry creates a favorable environment for targeted investment.

PW Consulting’s full report provides the layered analytics and operational checklists necessary to move from strategy to execution in 2026. To access the complete dataset, segmented models, and the practical playbook reserved for subscribers and clients, visit our report page and download the comprehensive study.

For detailed analysis of this topic, please visit the official page:Silica Gel Orange Desiccant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com