العوامل التي تؤثر على نجاح تكبير القضيب في الرياض

Health |

2026-06-12 06:02:50

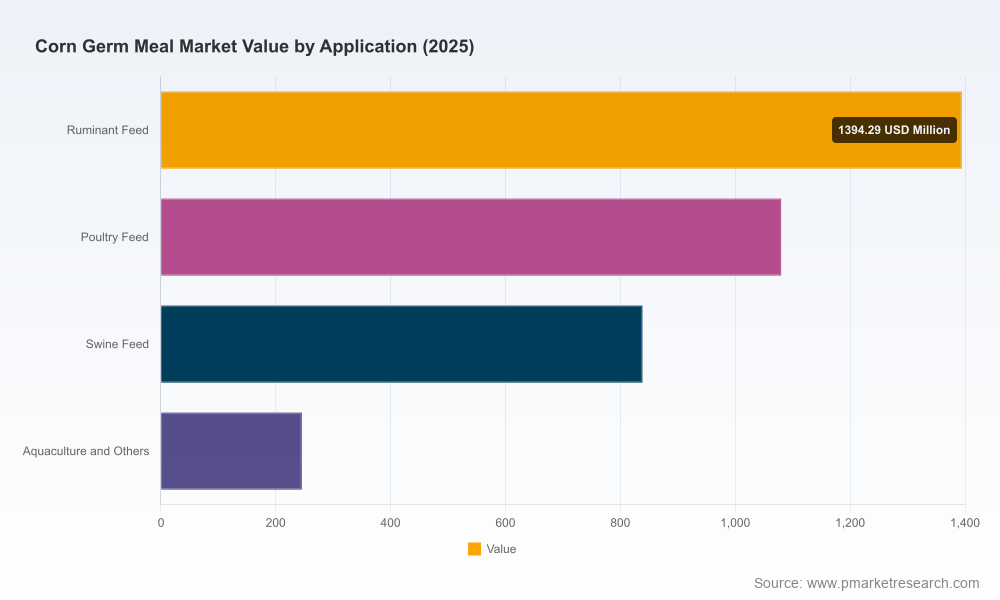

PW Consulting’s latest Corn Germ Meal Market report synthesizes five years of historical data (2020–2025) and delivers a forward-looking roadmap for 2026–2032. The market—measured in USD Million—was assessed with a 2025 base year and shows an estimated market value of USD 3,558.35 Million in 2025. Our probabilistic forecast anticipates steady expansion through the forecast window, driven by a compound annual growth rate (CAGR) of 4.52% (2026–2032), reaching a multi-billion-dollar market by 2032. This brief translates those macro dynamics into practical decision-making lines for processors, feed manufacturers, traders and investors preparing strategies in 2026.

Corn Germ Meal Market

Commodity and co-product dynamics have shifted: corn-processing margins, oil extraction efficiencies and wet-milling throughput are converging to change supply availability for corn germ meal. Notably, leading processors have signalled capacity moves in early 2026 that will alter regional supply balances.

Corn Germ Meal Market

Feed formulation pressures continue to rise as protein and oil markets remain volatile; corn germ meal’s nutritional profile positions it as a flexible medium-protein, energy-dense ingredient for ruminants and monogastrics—an immediate lever for formulators seeking cost and stability advantages.

Corn Germ Meal Market

Regulatory and quality-compliance regimes—especially GMP+ and mycotoxin monitoring—are becoming non-negotiable for cross-border trade and for premium feed segments, affecting both market access and pricing differentials.

The market’s base valuation and the 4.52% CAGR reflect two concurrent realities: (1) steady volume growth driven by livestock sector expansion and incremental product substitution in poultry and swine rations; and (2) periodic price and margin swings tied to corn/feedstock cycles and extraction technology gains. For 2026 strategy, that means companies must simultaneously manage near-term margin volatility and invest selectively in capacity or capability to capture medium-term (~3–6 year) upside as demand ecosystems mature.

Supply-side optimization: Processors should prioritize extraction efficiency and yield recovery programs. Recent capacity expansion announcements by major wet-millers underscore the competitive value of incremental germ extraction and downstream meal throughput. Firms that can raise effective germ recovery with modest incremental capital will elongate margins when feed demand tightens.

Quality and certification as market access levers: GMP+ certification and robust mycotoxin/pesticide/heavy-metal monitoring command a premium in export and high-value domestic markets. Certification is becoming a gating item for institutional feed buyers and integrators; investments in QA/QC systems can translate into tangible price and contract advantages.

Formulation playbooks for feed producers: Nutritional evidence shows corn germ meal can substitute a meaningful portion of soybean meal in broiler diets while preserving performance, and can be included at higher rates in swine finishing rations due to its fat content. Feed mills that redesign premix strategies to optimize blend economics will gain short-term cost relief and long-term buyer stickiness.

Risk management for traders and buyers: Monthly production monitoring—such as official tracking observed in large wet-milling jurisdictions—needs to be embedded in procurement cadence. Real-time visibility into wet-mill outputs and germ meal co-product flows is now table stakes for pricing and hedge strategy formation.

The sector is characterized by vertically integrated agribusinesses and specialist ingredient manufacturers. Global wet-milling leaders and regional processors play different strategic roles, but all are sharpening focus on three vectors: extraction efficiency, product quality/certification, and downstream feed customer relationships.

Global wet-milling majors (e.g., established agribusiness integrators): These firms leverage integrated origination, processing scale and diversified co-product portfolios to manage feedstock cycles and capture margin across the value chain. Their strategic playbooks emphasize capacity rationalization and selective modernization of extraction lines.

Ingredient specialists and refiners: These players are differentiating through technical services, certification credentials and specialty formulations targeted at premium feed segments and processors requiring tight QA/QC validation.

Regional producers and emerging-market processors: They are focused on local feed demand growth, shorter logistics chains, and competitive pricing but face rising compliance and quality expectations—creating potential partnership or consolidation targets for multinational offtakers.

Recent industry moves—capacity expansions at select wet-milling sites and the continued public reporting of monthly wet-mill outputs—signal an industry positioning for incremental growth rather than exponential volume shocks. Quality certifications maintained by several European and global producers further indicate where value will accrue.

Market sizing and demand modelling: Annual historical series (2020–2025) and scenario-based forecasts for 2026–2032, with sensitivity tests to feedstock price, extraction yield and livestock population trajectories (units presented in USD Million).

Supply-side mapping: Facility-level wet-mill capacity overlays, co-product routing, and a short-cycle visibility dashboard for monthly production indicators where public reporting exists.

Quality and regulatory matrix: Comparative analysis of certification regimes, testing protocols and trade compliance requirements that materially affect market access and premiums.

Company scorecards: Strategic assessments of leading processors, refiners and regional producers including capability, exposure to feedstock volatility, and likely strategic responses in 2026.

Commercial playbooks: Tactics for procurement, feed formulation optimization, co-product monetization and go-to-market approaches for new value-added germ meal derivatives.

Transaction and investment toolkit: Valuation sensitivities, due-diligence checklists and integration risk matrices tailored for M&A, greenfield builds and tolling arrangements.

Processors: Prioritize capital deployment to projects that improve germ recovery and QC throughput rather than broad capacity expansion; monetize certification and traceability as a revenue differentiator.

Feed manufacturers: Re-run least-cost formulation analyses incorporating higher-inclusion germ meal recipes; pilot programs in poultry and finishing swine rations can validate performance and establish commercial references.

Traders and distributors: Build near-real-time intelligence pipelines on wet-mill output and logistics constraints; restructure contracts to include quality/grade flexibility and incentive-sharing for certified loads.

Investors and corporate development: Focus diligence on technology that reduces mycotoxin and contaminant risk, assets with established QA certification, and regional assets that complement global supply networks.

Key downside risks for 2026 include feedstock price shocks, abrupt changes in biofuel or subsidy policy affecting corn availability, and compliance failures that limit access to high-value export markets. PW Consulting’s report provides a monitoring framework with leading indicators—monthly wet-mill production series, QA incident tracking, and feedstock futures spreads—to give decision-makers early warning and response options.

Our analysis translates macro figures—anchored in a 2025 market assessment and a quantified CAGR for 2026–2032—into an operational playbook. The value for executives lies not only in the headline growth rate but in the programmatic levers we identify: extraction and quality investments, formulation redesign, agile procurement, and disciplined M&A filters. In short, 2026 is a year for targeted, high-conviction actions that preserve margin while positioning for the projected multi-year expansion.

PW Consulting’s full Corn Germ Meal Market report contains the granular segmentation, facility-level maps, supplier scorecards and the scenario datasets that underpin the recommendations summarized here. For decision-makers preparing 2026 budgets and strategic initiatives, we recommend commissioning the full report and a tailored briefing, which will include custom sensitivity runs relevant to your portfolio and region. Visit the PW Consulting research portal to request access and to arrange a strategy workshop with our senior industry analysts.

For detailed analysis of this topic, please visit the official page:Corn Germ Meal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com