Bare Metal Cloud Market Trends in Data Security and Compliance

Other |

2026-03-25 08:35:47

PW Consulting’s latest European Bread Market study—anchored on a 2025 base year and a 2026–2032 forecast horizon—provides the actionable intelligence that senior executives, private equity sponsors, and supply‑chain leaders need to set priorities for 2026. The report shows a resilient market that recovered from the early‑decade disruption to reach roughly USD 55.0 billion in 2025 and, at a steady compound annual growth rate (CAGR) of 2.5%, is projected to approach the mid‑sixty billion mark by 2032. While headline growth is modest, our analysis reveals differentiated pockets of margin expansion, supply‑chain leverage, and regulatory-driven cost shifts that will determine winners and losers in the coming 18 months.

European Bread Market

Portfolio prioritization: The market’s moderate growth masks significant heterogeneity across product formats and routes‑to‑market. For corporates planning CAPEX or M&A in 2026, timing and target selection must be informed by granular demand drivers and cost scenarios—elements that are central to our report.

European Bread Market

Cost and procurement playbook: Volatility in key raw materials is already reshaping procurement strategies. Our scenario models translate commodity-price shocks into operating‑income sensitivity, supporting procurement hedging and supplier diversification decisions for 2026 contracts.

European Bread Market

Regulatory readiness: New packaging requirements and regional fortification mandates create near‑term compliance costs and opportunities for private‑label differentiation. The study identifies implementation pathways and a compliance cost checklist for product and packaging teams.

The European bread market demonstrated a recovery trajectory through 2022–2025, culminating in a market size of approximately USD 55.0 billion in 2025. Our baseline projection—reflecting conservative demand assumptions, ongoing urbanization, and stable consumption patterns—points to a 2.5% CAGR over 2026–2032. By 2032 the market is projected to be materially larger than mid‑decade levels, offering volume-led opportunities for scale players and niche premiumization paths for innovators.

Market concentration metrics are instructive: the three‑player concentration ratio (CR3) stands below one‑third of the market, and the five‑player concentration (CR5) remains under 40%. This balance reflects a market where national and regional champions coexist with numerous local bakeries—a structure that favors targeted consolidation, bolt‑on acquisitions, and regional rollouts rather than simple national rollups.

Raw materials and input volatility: Wheat and other cereal costs have become a central operating lever. Notably, wheat futures reached levels in mid‑2026 that are over 20% higher year‑on‑year, materially compressing margins for manufacturers without effective hedging or indexed pricing mechanisms. Our modelling shows how different procurement strategies translate into margin outcomes under multi‑scenario commodity paths.

Packaging regulation: The EU Packaging and Packaging Waste Regulation (PPWR), effective from August 2026, imposes recyclability, recycled‑content, and waste‑reduction targets. For bread manufacturers and packers this is not only a compliance cost—it is a procurement and design challenge that invites collaboration with converters, brand owners, and retailers to reengineer pack formats for both sustainability and shelf‑presence.

Product and labelling rules: Existing EU food information requirements remain a baseline for prepacked products, while certain national fortification rules—such as mandatory folic‑acid fortification for wheat flour in the UK—introduce formulation and labelling obligations that food‑safety and R&D teams must operationalize by late‑2026.

Channel and consumer shifts: Omnichannel grocery and direct‑to‑consumer models continue to gain traction for value and premium breads. Our demand‑elasticity analysis quantifies how price, convenience, and freshness attributes impact channel share under differing economic scenarios.

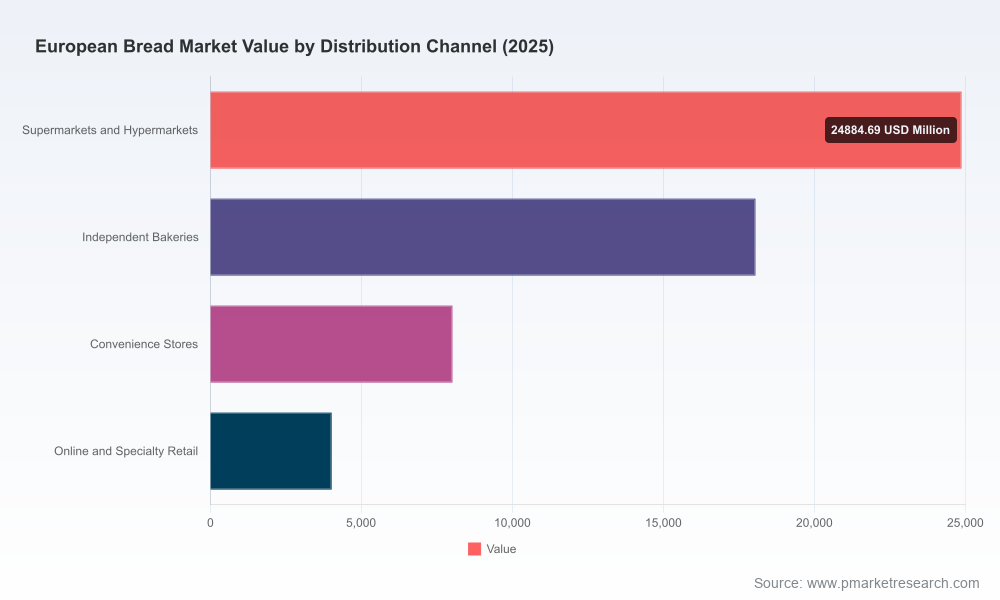

The market is composed of multiple product formats and distribution channels—fresh, frozen and par‑baked formats, traditional sliced and specialty loaves, retail outlets, independent bakers, convenience and online channels. While we intentionally withhold the detailed split tables in this release, the report identifies three strategic pockets with above‑market margin expansion potential: craft and artisanal premiumization, foodservice and QSR bake‑off supply chains, and convenience/online channels that capture premium price points through freshness and format innovation. The full report includes granular volumetric and pricing forecasts for each segment and channel, as well as an elasticity matrix to model promotional and price war scenarios.

The European competitive map blends global multinationals, regional champions, and dense local networks. Several strategic patterns have emerged among the key players we track:

Grupo Bimbo (BIMBO Europa operations): Leveraging scale and acquisitive capabilities, the company blends sliced‑bread portfolios with artisan and QSR bakery propositions. Their multi‑country footprint and integration of fresh and convenience formats make them a natural consolidator in markets where distribution scale confers cost advantage.

ARYZTA AG: Specializing in frozen and par‑baked convenience bakery, ARYZTA is doubling down on QSR and retail bake‑off demand. In January 2026 they announced a significant investment in a new bun manufacturing facility in Portugal to optimize Iberian supply chains—an example of capex targeted at service‑level improvement for large foodservice customers.

Lantmännen Unibake: A global group with a clear play in frozen and bake‑off segments, recently expanding through strategic acquisition activity in Italy. Their model emphasizes production footprint optimization and tailored retail and foodservice SKUs.

Barilla: A strong retail brand with a complementary bread and bakery portfolio, focused on product innovation and cross‑category merchandising within modern grocery channels.

Associated British Foods / Allied Bakeries and AB Mauri: A vertical interplay of branded bread manufacturing and ingredient supply positions this group to capture margin across the value chain in the UK market, particularly under fortification and labelling changes.

European Bakery Group and national specialists: Regional bake‑off specialists remain attractive targets for scale players seeking last‑mile freshness solutions across Western Europe.

ARYZTA’s Lisbon investment (Jan 2026): A capital allocation designed to serve QSR customers and reduce lead times in the Iberian market. This underscores a broader trend: investment that prioritizes service reliability and SKU rationalization over purely volume‑driven expansion.

Lantmännen Unibake’s acquisition of an Italian bake‑off producer (Dec 2025): Illustrates targeted expansion into engineering‑intensive frozen segments where entry barriers include production know‑how and cold‑chain logistics.

FEDIMA’s policy manifesto (2025): A coordinated industry push to influence EU policy on ingredients and competitiveness—highlighting that active dialogue with policymakers must be part of corporate strategy in 2026.

Rebase commodity risk: Convert ad‑hoc procurement exposure into formal hedging and indexation approaches. Use the report’s commodity‑sensitivity scenarios to negotiate flexible contracts with raw‑material suppliers and pass‑through mechanisms with key retailers and foodservice customers.

Prioritize PPWR compliance as product innovation: Treat packaging redesign not just as cost, but as brand differentiation—invest in lightweight, mono‑material structures that meet recyclability thresholds while preserving shelf visibility.

Selective consolidation: Use the CR3/CR5 concentration profile to identify markets where bolt‑on acquisitions can rapidly expand route‑to‑market and bake‑off capability—particularly attractive where local freshness is a competitive advantage.

Operational resilience: Diversify plant footprints and invest in modular frozen‑bake capacity to flex between retail and foodservice demand surges while capturing economies of scale in logistics.

Regulatory and public‑affairs playbook: Build an integrated compliance roadmap for fortification and labelling changes and engage proactively with trade associations to influence pragmatic implementation timelines.

The full report provides: a 2020–2025 historical base and a detailed 2026–2032 forecast model; segment and channel volume and value matrices; commodity sensitivity and margin impact scenarios; an M&A target map and valuation benchmarks; factory‑level capex case studies; a regulatory impact matrix (including PPWR and national fortification changes); and a competitor intelligence annex with corporate profiles and recent deal/activity timelines. Importantly, the report includes interactive Excel models and a decision‑support toolkit for 2026 planning cycles. To preserve the competitive integrity of our modelling we are publishing the full segment tables and scenario models on our report page—this release intentionally omits the underlying segmented figures to encourage direct access to the source materials.

Commodity shock scenario: A sustained wheat‑price spike materially compresses margins for producers unable to pass cost through retail contracts. Our downside scenario quantifies operating‑income erosion under multiple hedging approaches.

Regulatory timing risk: PPWR implementation challenges or accelerated national mandates for fortification can create short‑term sourcing and packaging bottlenecks. Early engagement with converters and ingredient suppliers is a low‑cost insurance policy.

Channel disruption: Rapid acceleration in online and convenience channel uptake could disproportionately reward operators with fine‑tuned last‑mile logistics and SKU families optimized for small‑basket shopping.

For 2026, the European bread market presents a paradox: steady headline growth but a dynamic undercurrent of regulatory, commodity, and channel shifts that will reshape competitive advantage. Companies that combine disciplined procurement, targeted capex, and regulatory foresight will capture outsized returns. PW Consulting’s European Bread Market study equips leaders with the quantitative models and playbooks to make those decisions with confidence.

To obtain the full dataset, segment tables, scenario models, and the tactical decision toolkit referenced here, please visit the PW Consulting report page where the complete report and downloadable resources are available.

For detailed analysis of this topic, please visit the official page:European Bread Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com