Fixed Wing Aircraft Rivets Market — Strategic Implications for 2026: PW Consulting Insight

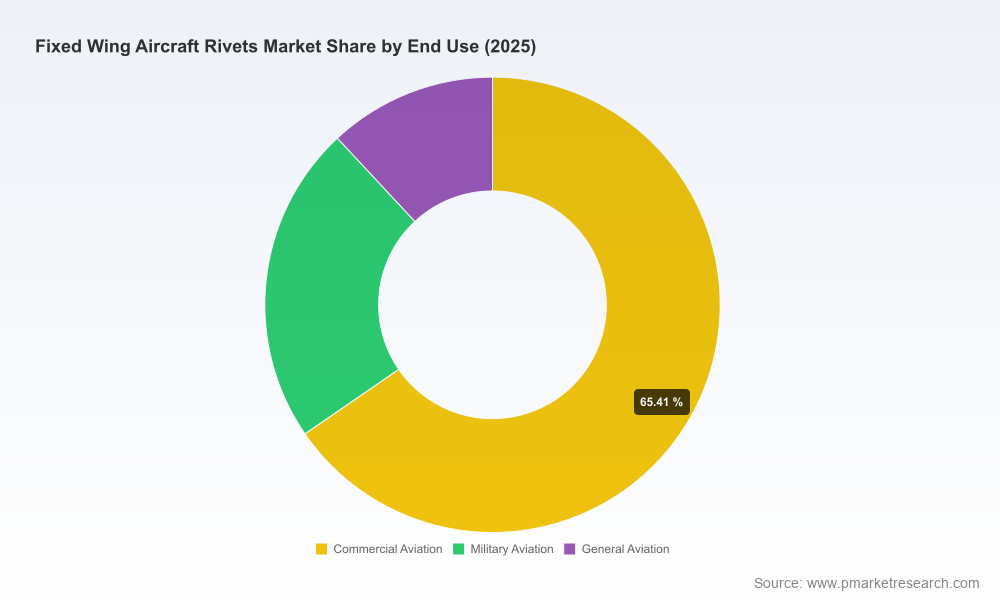

PW Consulting today releases a forward-looking executive insight drawn from our full Fixed Wing Aircraft Rivets Market report (base year 2025, forecast period 2026–2032). The global market for rivets used in fixed wing airframes continues to expand, with total industry revenues surpassing USD 1.0 billion in 2025 and our modelling pointing to sustained growth through the decade at a compounded annual growth rate (CAGR) of 5.26%. By 2032 the market is expected to approach the mid‑single‑billion mark, underscoring the continuing strategic importance of fastening technology across commercial, military and general aviation programmes.

Fixed Wing Aircraft Rivets Market

Why 2026 Is a Strategic Decision Year

Several converging forces make 2026 a pivotal year for procurement, product strategy and capital planning in the rivets ecosystem. Recent regulatory updates and industry initiatives introduced in late 2024–2025 are creating a new baseline for qualification, certification and traceability. At the same time, OEM investments in lower-impact joining equipment and public research funding for high‑temperature and sensor‑enabled fasteners are altering the technology roadmap. For companies that supply, specify or use rivets in fixed wing assembly, the near-term decisions taken in 2026 will materially influence cost of ownership, fleet reliability and compliance profiles for the next contract cycle.

Fixed Wing Aircraft Rivets Market

- Regulatory and standards updates introduced in 2025 require updated compliance matrices for blind fastening in composite-to-metal joints and electrical bonding in fuel‑tank areas—this elevates the certification burden for new fastener types.

- Parallel innovation signals—from OEMs piloting lower‑waste riveting equipment to public funding for high‑temperature and sensorized rivets—are shifting value from commodity metal supply toward systems that combine materials, installation tooling and data feedback.

- Raw‑material dynamics—particularly ongoing demand for lightweight alloys—create a supply‑chain premium on proven, defensible material strategies that balance cost, performance and sustainability goals.

What the PW Consulting Report Delivers (Practical, Operational Insight)

Our full study is designed as an operational playbook for executive teams planning budgets, supplier strategies and R&D roadmaps in 2026. Rather than a purely academic forecast, the report delivers tools and structured guidance that procurement directors, engineering leaders and corporate strategists can apply immediately.

Fixed Wing Aircraft Rivets Market

- Market model with transparent assumptions: a bottom‑up revenue forecast (2020–2032) and sensitivity scenarios that simulate demand shocks, certification delays and raw‑material price swings.

- Supplier and product taxonomy: mapping of solid, blind and specialty rivet form factors, materials strategy, and fit-for-purpose selection criteria for fixed wing airframes.

- Regulatory compliance matrix: crosswalks between new certification requirements and supplier qualifications to identify likely certification bottlenecks in 2026.

- Procurement playbooks and negotiation levers: templates for term contracts, inventory buffers, consignment models and make vs. buy decision frameworks specific to rivet procurement.

- Manufacturing and supply‑chain risk heatmaps: hotspot analysis for single‑source exposures, geography‑concentrated production, and supplier financial health indicators.

- Innovation and adoption roadmap: staged criteria to evaluate smart rivets, high‑temperature alloys, and new installation equipment—paired with test protocol recommendations and qualification timelines.

- Commercial due diligence and M&A screening: criteria for identifying attractive consolidation or partnership targets, and an index of strategic fit for fastener businesses.

Each of these deliverables is supported by annexes and templates that can be adapted within procurement systems and engineering qualification plans; the full deliverables are available via the report portal for teams preparing 2026 budgets and supplier development programmes.

Competitive Landscape: What Leading Suppliers Are Doing

The rivets market is neither a pure commoditised space nor a narrowly concentrated oligopoly. Our competitive analysis finds a mixed structure in which a small group of established aerospace fastener specialists exercise significant influence over standards, qualified supplier lists and premium segments of the market. The top three players account for a meaningful share of supply, and the five largest suppliers control a majority stake of the organised marketplace—creating both stability and potential chokepoints for buyers that rely on certified product lines.

- National Rivet & Manufacturing Co.: A vertically integrated specialist focused on solid aluminum rivets for airframe applications. Its AS9100:D and ISO 9001:2015 certifications, DFARS‑compliant material handling and in‑house quality control give it a strong position in programs that prioritise provenance and traceability.

- Howmet Fastening Systems (Howmet Aerospace): Known for high‑performance blind rivets engineered for limited‑access structures. Its product families are designed to meet aerospace NAS and MIL standards and are positioned to capture retrofit and repair work as well as new assembly where one‑side installation is required.

- Cherry Aerospace (SPS Technologies): A leader in blind rivet technologies for composite and thin‑skin assemblies, with a strong installed base for wing and fuselage applications that benefit from hole‑filling and locked‑spindle solutions.

- LISI AEROSPACE: Global reach and an integrated portfolio of metallic and composite-compatible fastening systems—well suited to OEMs seeking single‑source systems for multi‑platform assembly strategies.

- Hanson Rivet & Supply and RISCO Fasteners: Firms whose competitive advantages lie in MIL‑spec manufacturing disciplines and the ability to execute MS/NAS drawings and custom print work for specialised airframes.

Implication: For OEMs and Tier‑1s, supplier qualification will increasingly favour partners that can demonstrate both stringent quality systems and the capability to support new regulatory and data requirements (e.g., electrical bonding, embedded sensing). For suppliers, the path to margin improvement lies in bundled offerings—validated rivet + tooling + digital verification—rather than competing on raw material alone.

Market Structure and Consolidation Dynamics

Our concentration analysis shows that the market exhibits moderate consolidation: the top three suppliers accumulate a sizable portion of organised revenue, and the top five approach a majority share. This structure produces predictable pricing in established product lines, but it also elevates the strategic value of differentiated product development (sensor integration, high‑temperature alloys, tooling-as-a-service). Investors and corporate development teams should view specialised rivet technologies as potential bolt‑on targets for aerospace fastener groups seeking to deepen their OEM relationships.

Strategic Recommendations for 2026 Decision Makers

- Re‑baseline supplier qualification criteria to incorporate new certification and bonding requirements introduced in 2025. Prioritise suppliers who have demonstrable test protocols aligned with the updated standards.

- Accelerate pilot programmes for sensor‑enabled and high‑temperature rivet technologies where lifecycle benefits are provable. Use SBIR‑funded research and OEM pilot data as inputs to a staged adoption roadmap.

- Design procurement contracts with optionality: longer‑term commitments for base alloys to secure capacity, plus flexible call‑off structures for specialty fasteners that may require longer qualification cycles.

- Invest in in‑line verification and digital traceability. Installation tooling that provides a digital audit trail reduces rework risk and supports regulatory audits—an attractive ROI for high‑airframe‑cost platforms.

- Stress‑test supply chains against raw‑material volatility. Establish dual‑sourcing where feasible for critical grades and evaluate recycling and circular procurement pathways to lower exposure.

- Pursue partnerships with equipment OEMs focused on lower‑impact riveting systems: potential cost and sustainability benefits can be realised through co‑development agreements and volume guarantees.

- Build an M&A watchlist that prioritises firms with certified product families and niche technologies (e.g., blind rivets for composites, sensor integration, high‑temp alloys). Consolidation rationales should focus on access to qualified product lists and defence supplier networks.

Final Thought: Treat 2026 as a Strategic Investment Window

The rivets market for fixed wing aircraft is maturing from a component commoditisation phase into a systems and certification‑led landscape. The overall market trajectory—anchored by a 5.26% CAGR and rising revenues from a billion‑dollar base in 2025—creates both opportunity and complexity. Organisations that treat 2026 as an investment year for supplier qualification, tooling upgrade, and standards compliance will secure a disproportionate share of operational and regulatory advantage over the remainder of the forecast period.

PW Consulting’s full report contains the modelling, supplier scorecards, procurement templates, test‑protocol checklists and scenario workbooks needed to operationalise these recommendations. For the detailed segment‑level tables, supplier rankings, and the full set of decision tools referenced in this insight, please visit our report portal and request access to the Fixed Wing Aircraft Rivets Market study.

For detailed analysis of this topic, please visit the official page:Fixed Wing Aircraft Rivets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com