What Is Driving Elevator Market Growth in Smart Buildings and Urban Projects?

Networking |

2026-05-11 07:27:18

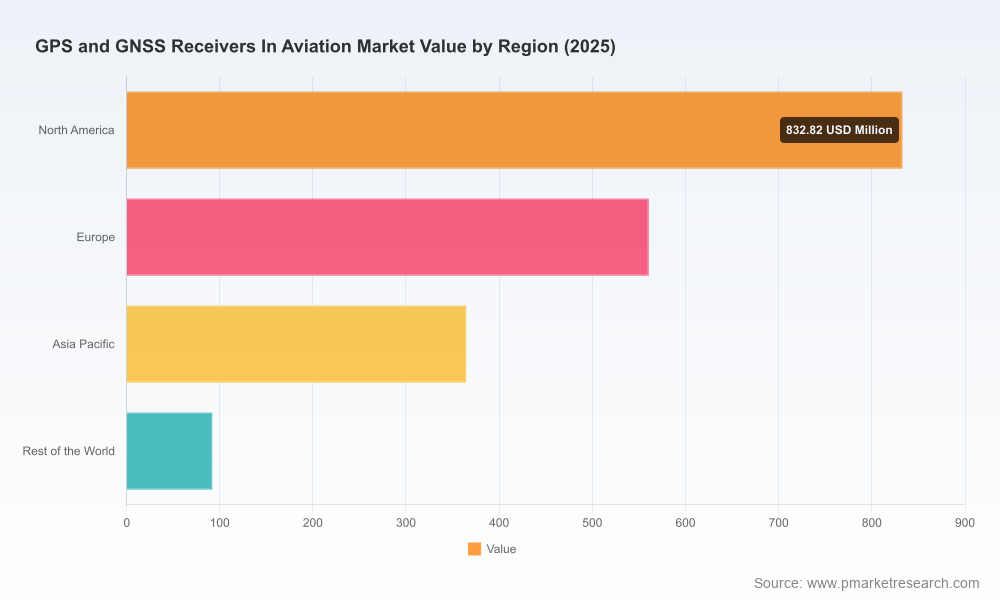

PW Consulting's latest market study on GPS and GNSS receivers in aviation provides a concise, decision-oriented roadmap for executives planning investments, procurement, certification, and partnership strategies in 2026. The market has evolved from a mid-cycle growth sector into a strategic vector for avionics modernization and resilient Positioning, Navigation and Timing (PNT). Our analysis shows the global market expanding from a 2025 baseline of approximately USD 1.85 billion to a projected market exceeding USD 2.9 billion by 2032, reflecting a compound annual growth rate (CAGR) of 6.75% across the 2026–2032 forecast horizon. Market concentration is meaningful: the top three vendors capture roughly half of industry revenues and the top five capture over 60%, underscoring a competitive but not immovable supplier landscape.

Gps And Gnss Receivers In Aviation Market

2026 will be a pivot year for aviation stakeholders. Regulators, air navigation service providers, airframers, avionics suppliers, and operators are aligning on near-term mandates and modernization programs that directly influence GNSS receiver requirements. PW Consulting's report distills the operational, regulatory, and competitive signals that matter when you must allocate capital, source retrofit or line-fit systems, or decide on M&A and technology partnerships. This briefing highlights the strategic trade-offs — speed-to-certification, resilience versus cost, and supplier lock-in versus modular integration — that will determine market winners over the next investment cycle.

Gps And Gnss Receivers In Aviation Market

Historical growth and near-term momentum: After steady expansion in the early 2020s, the market reached roughly USD 1.85 billion in 2025. PW Consulting projects continued growth driven by avionics retrofit cycles, NextGen/SESAR airspace modernization, and rising demand for multi-frequency, multi-constellation and anti-jam solutions.

Gps And Gnss Receivers In Aviation Market

Forecast dynamics: Our model anticipates a sustained CAGR of 6.75% from 2026 through 2032, culminating in a market size surpassing USD 2.9 billion by 2032. The growth is broad-based across civil and military aviation, though the risk and procurement profiles differ materially by customer segment.

Concentration and competitive posture: A moderately concentrated vendor structure (CR3 ~48.5%; CR5 ~62.3%) creates strategic implications for buyers and challengers: incumbent suppliers command scale advantages in certification, global support, and embedded platform relationships, but there is room for targeted insurgents with differentiated anti-jam, software-defined receivers, or integration-focused business models.

Airspace modernization (NextGen/SESAR): Programs stressing L5 and dual-frequency performance are accelerating demand for receivers that support advanced approach procedures, ADS-B integration and higher integrity positioning. Procurement timelines tied to air traffic modernization mean operators who delay will face longer lead times and potential retrofit backlog risk.

Interference and resilience: Recent FAA guidance (Interference Resource Guide v1.1, March 2026) and coordinated industry plans published by EASA and IATA (noting substantial increases in signal loss events in recent years) have elevated anti-jamming and spoofing mitigation from a "nice-to-have" to a procurement requirement in many fleets and military platforms.

Regional compliance mandates: National mandates — for example, dual-frequency compliance measures in certain jurisdictions — are creating definitive timelines for hardware upgrades and certification workstreams that suppliers and integrators must accommodate.

Operational feedback loops: Airlines and military operators are demanding not only accuracy but assured availability and auditability of PNT sources; this drives system-level solutions (GNSS + INS + cyber-hardened software) rather than stand-alone receivers.

The supplier field is populated by established avionics and aerospace systems integrators, specialist GNSS OEMs, and emerging defenders of resilient PNT. Key players profiled in the report include:

Garmin Ltd. (Schaffhausen, Switzerland) — strong in certified avionics and retrofit avionics for general aviation and business jets, with FAA TSO-aligned products.

Honeywell International Inc. (Charlotte, NC) — focuses on integrated GNSS/INS and solutions for GNSS-denied environments, leveraging deep aircraft systems integration expertise.

Collins Aerospace (RTX) (Cedar Rapids, IA) — supplies multi-constellation receivers and navigation suites tailored to both military and commercial applications.

Thales Group (Paris, France) — builds certified receivers with anti-jam capabilities and civil/military dual-use solutions.

Trimble Inc. (Westminster, CO) and NovAtel/Hexagon (Calgary) — provide precise OEM GNSS/INS modules and reference-grade receivers for avionics integrators and government customers.

L3Harris, Northrop Grumman, BAE Systems — maintain defense-focused portfolios, including M-code capable and jam-resistant products critical for high-end military platforms.

Septentrio (Leuven, Belgium) — a specialist in multi-frequency, anti-jam GNSS receivers for high-integrity aviation needs.

Recent industry developments underscore a bifurcation of product strategies: one track emphasizes small-form, low-SWaP anti-jam solutions for unmanned systems and retrofit flexibility (e.g., new compact PNT products introduced in 2026), while another track consolidates platform-level embedded, certified avionics for line-fit installations and military modernization programs.

FAA published an updated interference guide in March 2026, increasing emphasis on operational reporting and mitigation workflows.

EASA and IATA framed coordinated mitigation plans in mid-2025 that have since affected certification priorities.

Several suppliers announced product deliveries, launches, and certifications in early 2026 — including modernized EGI deliveries, certified retrofit avionics, and compact anti-jam receivers aimed at both crewed and uncrewed platforms.

Whether you are a Tier-1 OEM, an airline CTO, a defense acquisition lead, or a private equity investor, 2026 decisions should be guided by the following strategic priorities:

Prioritize resilience: Mandate anti-jam/anti-spoof capabilities and multi-constellation/multi-frequency support in procurement specs. For operators, require suppliers to demonstrate not just static performance but validated performance under interference scenarios.

Accelerate certification pipelines: Time-to-market is driven by certification; pursue parallel certification strategies (EASA/FAA) and invest in test-lab capabilities early to shorten retrofit lead times.

Design for modularity: Favor receivers and navigation modules designed for software-defined feature upgrades and easier line-replaceable integration to reduce life-cycle costs and enable future capability insertion.

Balance own-versus-buy for INS fusion: Platform integrators should evaluate whether to develop INS fusion capabilities in-house or partner with specialized OEMs to accelerate delivery and spread certification risk.

Leverage procurement windows: Government and commercial fleet upgrade cycles open procurement windows that suppliers can exploit with bundled warranty, support, and certification roadmaps.

Monitor geopolitics and supply chain exposure: Ensure parts and software provenance meet national security requirements for sensitive programs and account for regional mandates requiring local or specific constellation compliance.

This study is designed as an operational playbook for 2026 and beyond. The full report contains:

Granular market model and scenario analyses — including upside and downside cases tied to regulatory timelines and interference trends.

Buyers' decision matrix — practical procurement templates specifying minimum resilience, certification, and integration requirements.

Supplier benchmarking and vendor strategy maps — assessment of technology, certification, global support footprint, product roadmaps, and M&A positioning for leading suppliers.

Risk register and mitigation playbooks — covering interference, supply chain, certification delays, and cybersecurity threats to PNT systems.

Actionable recommendations for R&D prioritization, go-to-market channels, retrofit vs. line-fit economics, and partnership frameworks to accelerate adoption.

For OEMs: Map existing product roadmaps against regulator timetables and prioritize features that unlock immediate procurement opportunities (e.g., L5 support, DFMC compliance, anti-jam modules).

For operators: Conduct a rapid fleet vulnerability assessment and a supplier readiness audit to identify high-risk airframes and schedule mitigations during planned maintenance windows.

For investors: Use the report's vendor scorecards and M&A scenarios to identify acquisition targets with certification assets, anti-jam IP, or software-defined upgrade pathways.

In an environment where modernization programs, interference risk, and national mandates are converging, GNSS receiver decisions are strategic, capital-intensive, and time-sensitive. PW Consulting's report converts market dynamics into executable choices: who to partner with, when to certify, how to design for future resilience, and which procurement levers unlock fleet-level outcomes. We intentionally present high-level market sizing and concentration context here while reserving the detailed segmentation, regional and application-level forecasts, and complete vendor scoring for the full report to preserve its operational value as a decisioning tool.

To access the full analytical model, vendor profiles, and the step-by-step implementation playbooks for 2026 action, please visit our report landing page or contact PW Consulting's Aviation Advisory desk for a briefing.

For detailed analysis of this topic, please visit the official page:Gps And Gnss Receivers In Aviation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com