Sleeping Aid Market Outlook with 6% CAGR Through 2032; Pfizer, Sanofi, GSK Shape Industry

Networking |

2026-04-21 20:38:22

Insurance is evolving rapidly as businesses seek faster, more predictable financial protection against risks. While traditional insurance has been the industry standard for decades, parametric insurance is becoming increasingly popular for organizations that need immediate access to funds after a triggering event. Although both models aim to reduce financial uncertainty, they operate in fundamentally different ways. Understanding these differences helps insurers, brokers, CFOs, and risk managers choose the right billing model based on their operational needs, risk exposure, and financial objectives.

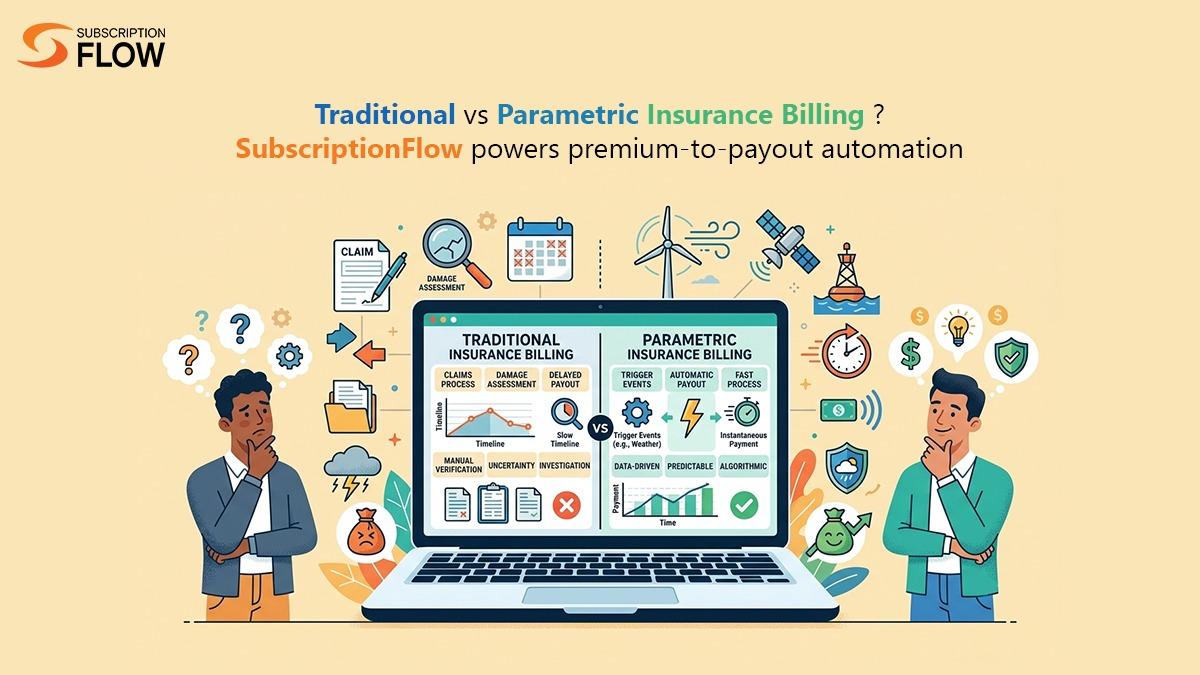

Traditional insurance follows the principle of indemnity, meaning policyholders receive compensation based on the actual financial loss they experience. Before a policy is issued, insurers perform detailed underwriting by evaluating assets, claims history, business operations, industry risks, and coverage limits. Premiums are calculated according to these factors and may include audits, policy endorsements, deductibles, and adjustments throughout the policy period. When a loss occurs, the claims process involves inspections, documentation, loss assessment, and verification before compensation is approved. Although this approach ensures accurate reimbursement, it often results in lengthy claim settlements and considerable administrative effort.

Unlike traditional insurance, parametric insurance does not depend on assessing physical damage. Instead, payouts are automatically released when a predefined measurable event reaches an agreed threshold. These events may include earthquakes exceeding a specified magnitude, hurricanes reaching a certain wind speed, rainfall falling below a defined level, or other objective environmental indices. Since there is no need for damage inspections or proof of loss, payments can be processed within days after the trigger is verified by an independent data source. This simplified approach provides businesses with rapid liquidity when they need it most.

The primary distinction between traditional and parametric insurance lies in how claims are settled. Traditional insurance compensates for actual verified losses, while parametric insurance pays predetermined amounts once an agreed trigger occurs. Traditional claims often require adjusters, inspections, invoices, and extensive documentation, making payouts slower but highly accurate. Parametric policies eliminate much of this administrative burden by relying solely on verified data, offering faster and more predictable payments. Premium pricing also differs, as traditional insurance focuses on individual risk characteristics, whereas parametric insurance is priced according to the probability and severity of measurable events.

Traditional insurance remains the preferred choice for protecting valuable physical assets, commercial properties, liability exposures, and complex business risks. Its greatest advantage is the ability to compensate policyholders according to their actual financial losses, ensuring comprehensive protection. However, this precision comes with challenges, including lengthy claim investigations, extensive paperwork, higher administrative costs, and delayed access to funds during critical recovery periods.

Parametric insurance offers speed, transparency, and operational simplicity. Businesses benefit from rapid payouts, reduced documentation requirements, and the flexibility to use funds wherever they are needed. This model is particularly valuable for natural disasters, business interruptions, agriculture, and climate-related risks. However, because payouts are predetermined rather than based on actual damage, businesses may occasionally receive more or less than their real financial loss. The model also relies heavily on accurate third-party data and clearly defined trigger mechanisms.

Selecting between traditional and parametric insurance depends on the nature of the risks being managed. Organizations with significant physical assets or liability exposures generally benefit from traditional insurance because it accurately covers verified losses. Businesses operating in disaster-prone regions, facing high deductibles, or requiring immediate cash flow after catastrophic events often find parametric insurance to be a valuable supplement. Increasingly, companies are combining both models to create layered protection that balances comprehensive coverage with rapid financial support.

Managing insurance billing across multiple policy structures can become complex without the right technology. SubscriptionFlow streamlines premium collection, recurring billing, payment processing, and policy lifecycle management for insurers using both traditional and parametric models. Its flexible billing engine supports multiple pricing structures while automating invoicing, payment collection, workflow management, and financial operations. Although it is not a dedicated parametric trigger platform, it enables insurers to efficiently manage the financial processes surrounding both billing approaches from a unified system.

Traditional and parametric insurance billing are not competing solutions but complementary approaches to modern risk management. Traditional insurance provides comprehensive protection by compensating verified losses, while parametric insurance delivers rapid financial assistance through predefined event triggers. As businesses face increasingly unpredictable risks, combining both models creates stronger financial resilience, improves cash flow during crises, and reduces operational disruptions. Organizations that understand the strengths of each approach can build more effective insurance strategies while leveraging automation platforms like SubscriptionFlow to simplify premium management and policy administration.