Business Management Consulting Service Market 2026: Strategic Intelligence for Decisions That Matter

PW Consulting is pleased to release a strategic preview of our Business Management Consulting Service Market research—a forward-looking intelligence product designed to inform executive decisions in 2026 and beyond. Drawing on a harmonized view of historical performance (2020–2025), proprietary forecasting (2026–2032), and a granular competitive and regulatory scan, this briefing explains why the consulting market’s trajectory matters to corporate leaders, investors, and policy teams—without revealing the granular segmentation that is reserved for subscribers to the full report.

Business Management Consulting Service Market

Market snapshot and trajectory

The global business management consulting market expanded notably over the pandemic-recovery window and continued to grow into 2025. Our consolidated market sizing places the industry in excess of one trillion USD in 2025, with a projected expansion into 2026 and a multi-year compounded annual growth rate (CAGR) of approximately 5.22% over the 2026–2032 forecast horizon. This blend of steady organic demand and episodic, deal-driven surges means the advisory landscape will provide both stable recurring revenue pools and high-impact win-or-lose engagements for firms and their clients.

Business Management Consulting Service Market

Two implications follow immediately for 2026 planning: first, strategic allocation of consulting spend needs to balance immediate transformation priorities (digital, cost optimization, regulatory compliance) with longer-term capability-building (AI governance, cloud-native operating models). Second, suppliers and buyers should prepare for a market that is sizable and growing—but structurally fragmented—offering opportunities for specialization, partnerships, and consolidation plays.

Business Management Consulting Service Market

Why this report matters for 2026 decisions

- Actionable timing for investments: Our forecast maps the likely cadence of demand across the next seven years so CFOs and corporate strategy teams can align multi-year transformation budgets to market cycles and supplier capacity.

- Risk-aware scenario planning: With regulatory impulses accelerating and labor-cost pressures persisting, the report’s scenario modules translate macro uncertainty into quantified implications for program timing, outsourcing, and insourcing decisions.

- Commercial model design: The research identifies where fixed-fee, outcome-based, and subscription pricing are becoming commercially viable—and where legacy time-and-material models still dominate—helping commercial teams structure proposals that meet buyer risk appetites in 2026.

- Procurement and vendor selection playbook: Practical evaluation frameworks (including capability mapping, TCO templates, and negotiation levers) enable procurement to reduce selection risk and accelerate time-to-value.

What’s in the full report: practical, operational content

PW Consulting’s full report is designed as a working toolkit for decision-makers, not just as an academic exercise. Key deliverables include:

- Executive dashboards with trend overlays and sensitivity bands to test the impact of alternative macro scenarios (inflation, talent cost ramps, cybersecurity regulation).

- Rigorous vendor assessment templates and RFP language calibrated for strategy, operations, financial advisory, HR, and technology management engagements.

- Ready-to-use implementation roadmaps and milestone checklists for 12–36 month transformation programs, including staffing profiles, vendor-sourcing options, and change-management artifacts.

- Commercial negotiation playbooks that align fee structures to measurable outcomes, with legal and compliance risk checkpoints for cross-border engagements.

- AI & digital adoption matrices and governance checklists that integrate privacy and data residency requirements—critical where new state-level and sectoral rules affect advisory workflows.

- Due-diligence heuristics for M&A and portfolio rebalancing, including value-capture levers, integration risk scoring, and scenarios for scaling captive consulting units versus outsourced partners.

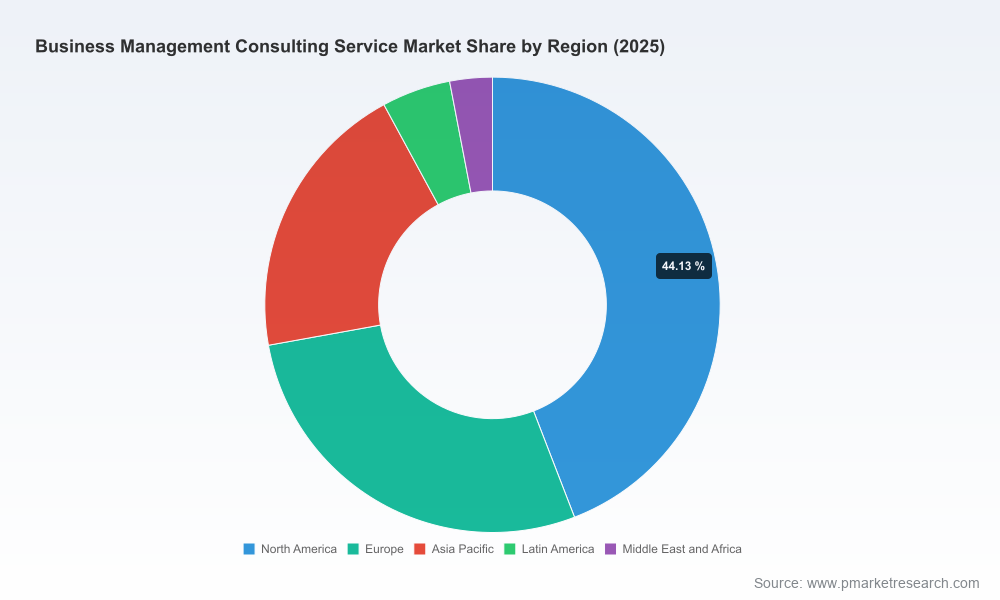

Note: this press briefing intentionally omits the granular regional and application-level splits that purchasers of the full report receive as downloadable datasets and interactive visualizations. Those segmentation layers are provided with methodological notes and validation samples in the subscriber edition.

Competitive landscape: what leading firms are doing (and what it means)

The market remains shaped by global strategy houses, integrated professional services firms, and technology-enabled consultancies. The top-tier strategy firms continue to command reputation premiums for high-stakes strategy and private-equity work, while large multidisciplinary firms deliver scale in enterprise-wide digital, cloud, and restructuring engagements. Recent firm-level moves illustrate how competition is evolving:

- McKinsey & Company persists as a go-to advisor for board-level strategy and complex operational turnarounds, leveraging deep sector practices to win transformational mandates.

- Boston Consulting Group (BCG) has doubled down on digital and AI-enabled transformation; their recent public disclosures reflect continued revenue momentum and a push into outcome-linked offerings.

- Bain & Company remains focused on results-oriented engagements and private equity advisory, emphasizing measurable performance improvement during implementation phases.

- Deloitte, PwC, EY, and KPMG (the Big Four) continue to leverage consulting scale combined with audit, tax, and deal flows to offer integrated solutions—now increasingly packaged with software and managed services.

- Accenture and IBM Consulting are expanding technology-led consulting bundles: recent quarterly results from Accenture underline strong bookings and a willingness to invest in capability buildouts that pair advisory with cloud and AI delivery.

- Oliver Wyman and selected boutiques retain niche strength in financial services, risk, and regulatory compliance, offering specialized domain expertise for complex sectors.

Market concentration remains moderate: the top three to five firms do not control the majority of demand, leaving room for mid-tier and niche players. That structural openness means new entrants and specialist firms can capture disproportionate value by targeting under-served problem sets (for example, industry-specific AI governance or hybrid operating model implementation).

Regulatory and labor dynamics shaping advisory demand

Several cross-cutting dynamics will materially influence commercial and delivery choices in 2026:

- Talent costs and supply: Competition for senior strategy, digital, and AI talent is elevating bill rates and hiring costs. Buyers and sellers must evaluate workforce models that mix onshore senior design with offshore implementation to preserve margins while protecting knowledge transfer.

- Data privacy and cyber regulation: A proliferation of state-level privacy laws and recent cybersecurity mandates for regulated sectors are raising the bar on how consultancies handle client data and AI tooling. Compliance-ready delivery templates and certifications are becoming table stakes in vendor selection.

- Transaction and procurement rules: New rules on bulk data handling and cross-border transfers require advisory teams to embed privacy and record-keeping processes into every engagement that uses sensitive personal data.

Strategic recommendations for 2026

Based on the market sizing, competitive scan, and regulatory context, PW Consulting recommends the following priority actions for corporate decision-makers in 2026:

- Adopt a modular sourcing strategy: Break large transformation programs into modular, outcome-aligned workstreams. Use a mix of elite strategy partners for framing and specialist implementers for technical execution. This reduces schedule risk and improves vendor accountability.

- Lock in governance for AI and data practices: Require consulting partners to present certified controls and operational runbooks for AI models, data residency, and privacy during the RFP stage. This protects programs from stop-work orders and costly remediation.

- Make commercial incentives explicit: For initiatives where measurable business outcomes can be defined (cost-to-serve, revenue uplift, cycle-time reduction), structure multi-year contracts with clearly auditable milestone payments tied to jointly agreed KPIs.

- Invest in internal capability while buying sparingly: Prioritize building in-house capabilities for vendor management, data engineering, and change activation—capabilities that reduce long-term dependence and lower TCO for recurring needs.

- Use scenario-based budgeting: Incorporate the report’s scenario bands into mid-year re-forecasts; this is particularly important where regulatory or labor-cost shocks could compress or accelerate program timelines.

How to use the full PW Consulting report

The preview you are reading outlines the strategic logic and operational tools we include in the full market study. Subscribers receive:

- Interactive datasets for market sizing and forecast sensitivity across 2026–2032;

- Complete segmentation breakdowns with regional and application-level detail (omitted here to preserve the report’s subscriber value);

- Vendor scorecards and recent development timelines with source-linked citations; and

- Customizable playbooks and Excel models to support procurement, investment committees, and program boards.

Executives who need to convert insight into action in 2026 should consider the full report as a practical operating manual: it is structured to be used in board meetings, procurement negotiations, and transformation program gates.

Conclusion

The business management consulting market in 2026 presents a compelling mix of scale and fragmentation. With total industry revenue surpassing the trillion-dollar mark and a steady mid-single-digit CAGR through the forecast window, consulting remains a strategic lever for competitive advantage. But seizing that advantage requires disciplined procurement, compliance-forward delivery models, and a calibrated mix of external talent and internal capability building. PW Consulting’s full report equips leaders with the actionable frameworks, validated data, and operational templates needed to make those choices confidently.

To access the complete dataset, regional and application breakouts, and the practical tools referenced in this briefing, please visit the PW Consulting report page for subscription and licensing options.

For detailed analysis of this topic, please visit the official page:Business Management Consulting Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com