Breaking: Battery Recycling Systems Maintenance Market Poised for Exponential Growth

Other |

2026-06-22 07:31:05

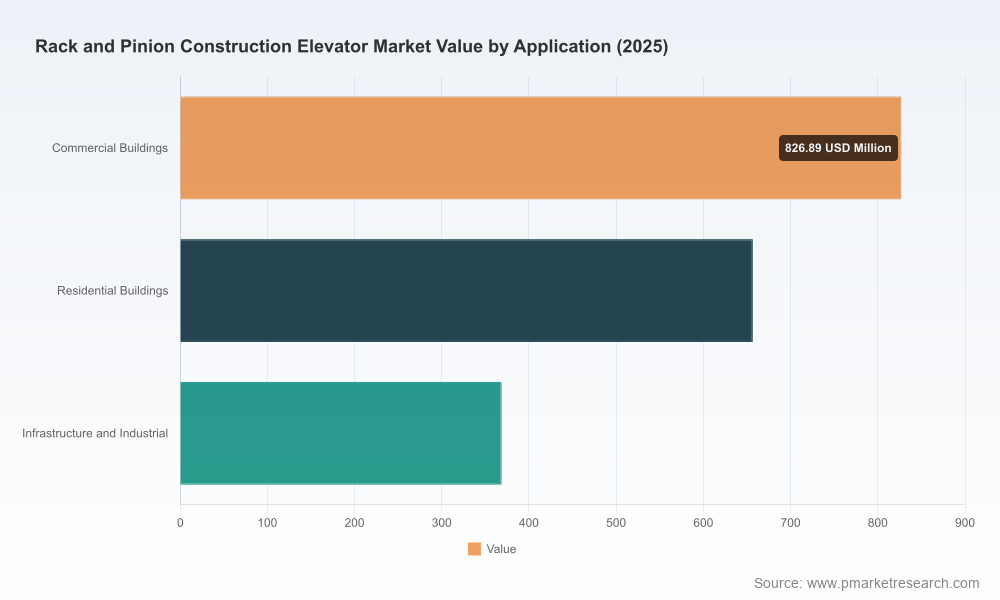

PW Consulting’s latest market study on Rack and Pinion Construction Elevators positions the sector at a strategic inflection point for 2026. After expanding from approximately USD 1.32 billion in 2020 to roughly USD 1.85 billion in 2025, the market is forecast to continue its multi-year expansion trajectory, reaching an estimated USD 2.09 billion in 2026 and approaching USD 3.0 billion by 2032, under a base-case compound annual growth rate (CAGR) of 7.0% for the forecast window. For executives contemplating capital allocation, fleet strategy, M&A, or supply-chain resilience in the coming 18 months, the implications are immediate: demand is rising, competitive intensity is concentrated but far from monopolized, and near-term inputs and regulatory shifts will materially affect unit economics.

Rack And Pinion Construction Elevator Market

Actionable foresight, not hindsight — The report translates historical momentum (2020–2025) into tactical scenarios for 2026 planning cycles, aligning commercial, operational, and regulatory considerations with realistic revenue and cost trajectories.

Rack And Pinion Construction Elevator Market

Investment-readiness — Whether your objective is to scale a rental fleet, evaluate a factory expansion, or pursue bolt-on M&A, the study provides calibrated financial templates and risk-adjusted return thresholds tailored to rack-and-pinion assets.

Rack And Pinion Construction Elevator Market

Procurement and CapEx optimization — Elevated raw material volatility and regionally divergent steel costs require a refreshed procurement playbook; our models quantify break-even points for localized fabrication vs continued import dependency.

Compliance-first operations — Anticipated changes to safety codes and inspection regimes (notably public review drafts of elevator safety standards and enduring OSHA requirements for material and personnel hoists) demand immediate updates to maintenance cycles and capital reserve strategies.

Demand fundamentals — Infrastructure and urbanization tailwinds, together with industrial maintenance and shutdown work, underpin continued replacement and incremental fleet growth across construction and industrial applications.

Input-cost inflation — Steel benchmark shifts in 2025–26 have raised landed costs for structural components. Our scenario analysis demonstrates how a 20–40% swing in coil prices compresses margins on new unit builds and accelerates aftermarket revenue importance.

Regulatory tightening — Ongoing revisions to elevator safety codes and existing OSHA requirements increase testing frequency and lifecycle servicing obligations; operators should budget for more frequent certification events and component replacement cycles.

Aftermarket and services as margin levers — Rental, refurbishment, and long-term service contracts are now central to durable profitability. Companies that reposition toward recurring service models can offset capital-cycle volatility.

The market shows meaningful leader presence but remains accessible to well-capitalized challengers. Our concentration analysis indicates that the top three manufacturers capture less than one-third of spend, with the top five controlling just under half — a structure that favors differentiated service propositions and targeted consolidation.

Alimak Group AB (Stockholm, Sweden) — Firmly positioned as a global technology and fleet leader, Alimak’s broad product portfolio and compliance pedigree make it a benchmark for premium engineering. Strategic implication: competitors should either match service ecosystems or pursue niche specialization to avoid head-on competition.

GEDA GmbH (Germany) — Deep industrial focus and in-house structural manufacturing capabilities give GEDA an edge for heavy-duty and specialty industrial projects. Strategic implication: pursue alliances or sub-supply arrangements when targeting high-spec industrial contracts.

STROS (Czech Republic) — A recognized supplier into the U.S. market via partners, STROS demonstrates the commercial viability of channel-led expansion. Strategic implication: OEMs can scale faster by deploying partner distribution models rather than building costly local footprints.

USA Hoist / Mid-American Elevator (Crest Hill, IL, USA) — Focused U.S. manufacturing and custom high-capacity platforms position USA Hoist as a go-to for speed, reliability, and ANSI-compliant designs. Strategic implication: localized manufacturing remains an important differentiator for North American projects sensitive to lead times and standards.

Century Elevators (Alimak Group, USA) — Concentration on permanent industrial installations indicates the growing split between temporary construction hoists and permanent industrial systems. Strategic implication: product-line segmentation can increase yield per installed asset.

McDonough Elevators (USA) — A prominent fleet operator and service provider, McDonough highlights the commercial value of rental scale and full-lifecycle services. Strategic implication: scale in rental fleets and refurbishment capability materially changes cash flow profiles.

UCEL Inc. (Canada) — As a regional integrator with European OEM partnerships, UCEL underscores the importance of cross-border sourcing and compliance knowledge, especially for projects requiring CSA/ANSI/CE conformance.

BrandSafway (USA) — End-to-end turnkey offerings position BrandSafway to win on bundled engineering, installation, and maintenance; this is a notable trend toward integrated site solutions.

Maspero Elevatori (Italy) and Ficont Industry / 3S Lift (China) — These firms reflect the spectrum from bespoke European craftsmanship to CE-certified, cost-competitive manufacturing—each presents distinct partnership or competition vectors depending on buyer priorities.

Supply-chain hedging — Adopt a dual-sourcing strategy for critical structural components, combined with multi-year purchase agreements tied to indexed steel prices to protect margins.

Service-led commercial models — Transition toward predictable revenue through long-term maintenance contracts, performance SLAs, and certified inspection packages.

Fleet utilization optimization — Use telematics and predictive maintenance to raise uptime and reduce total cost of ownership; our models quantify utilization elasticities that shift ROI on rental units by several percentage points.

Compliance and testing cadence — Update operational budgets to reflect mandated biannual testing frequencies and multi-year replacement cycles for safety devices; non-compliance risk now carries both financial and reputational costs.

Selective vertical integration — Evaluate acquisitions that offer spare-parts inventories, refurbishment facilities, or local manufacturing to shorten lead times and capture aftermarket margins.

Product refreshes and model launches — New model announcements from regional manufacturers indicate continuing product innovation on capacity and modularity; buyers should re-assess spec sheets against lifecycle cost impacts, not just purchase price.

Industry commentary on industrial projects — Thought leadership from integrators highlights the growing use of rack-and-pinion lifts in maintenance and shutdown contexts, expanding the addressable market beyond pure construction cycles.

Regulation updates — Proposed revisions to safety codes are expected to clarify equipment definitions, location rules, and periodic testing requirements; firms must update certification roadmaps immediately to avoid retrofit spikes.

The study is designed as a decision-ready toolkit for 2026. Key deliverables include:

Financial models and scenario analyses that translate market growth and input-cost volatility into capital planning templates for manufacturers, fleet operators, and investors.

Go-to-market playbooks for product positioning—whether you compete on engineered premium platforms, cost-competitive builds, or service-led rental models.

Regulatory compliance checklists and inspection calendars aligned to current OSHA and emerging code drafts, plus recommended documentation and audit practices.

Supply-chain risk maps and procurement negotiation frameworks that quantify the threshold for localized manufacturing vs. continued offshore sourcing.

Competitive benchmarking and acquisition screening criteria, including vendor scorecards, synergy potential metrics, and post-merger integration blueprints.

Operational playbooks for fleet optimization—telematics adoption roadmaps, predictive maintenance recipes, and refurbishment economics to extend asset life.

Run a 90-day procurement stress test to model steel-price scenarios and identify hedging or contractual levers.

Audit all service contracts and testing schedules against anticipated code changes; prioritize CAPEX for systems that will face more frequent testing or earlier component replacement.

Screen potential acquisition targets with spare-parts inventory or refurbishment centers that can be integrated to accelerate aftermarket revenue capture.

Initiate pilot telematics on a representative subset of rental units to validate utilization uplift and maintenance-savings assumptions in our financial models.

The rack and pinion construction elevator market is maturing into a domain where engineering capability, aftermarket services, and supply-chain agility determine winners. With market value expanding materially into 2026 and beyond, executive teams must align capital allocation, regulatory compliance, and commercial models to capture growth while protecting margins from input-cost shocks and evolving safety regimes. PW Consulting’s report condenses market-scale forecasting, competitive intelligence, and hands-on playbooks into a single resource engineered for immediate operationalization—an essential input for any 2026 strategic planning cycle.

Download the executive brief and order the full report for access to the detailed models, vendor scorecards, and scenario workstreams that we intentionally reserve for subscribers and clients. PW Consulting stands ready to convert the study’s recommendations into an executable 12–18 month transformation plan tailored to your organization.

For detailed analysis of this topic, please visit the official page:Rack And Pinion Construction Elevator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com