Breaking: Agricultural Tractor Repair and Maintenance Services Market Grows Steadily

Other |

2026-06-18 10:56:57

PW Consulting’s newly published market research on the Automatic Leak Detection (ALD) Equipment market delivers an actionable intelligence package designed to shape executive decisions in 2026. Built on a 2020–2025 historical foundation with 2025 as the base year and a 2026–2032 forecast horizon, the study combines macroeconomic projections, regulatory horizon scanning, technology landscaping and competitor playbooks to inform product, commercial and M&A strategies.

Automatic Leak Detection Equipment Market

The ALD equipment market reached USD 4,158.5 Million in 2025 (base year) and is forecast to expand at a compound annual growth rate (CAGR) of 5.85% over the 2026–2032 period, reaching approximately USD 6,192.8 Million by 2032. This growth trajectory reflects accelerating regulatory enforcement, broader deployment of permanent monitoring solutions across utilities and industrial sites, and faster commercialization of higher-resolution sensor platforms. For executives planning 2026 budgets, the confluence of near-term regulatory compliance deadlines and technology maturation creates windows for both defensive investments (to maintain compliance and service existing clients) and offensive plays (to capture greenfield deployments and high-margin retrofit opportunities).

Automatic Leak Detection Equipment Market

Regulatory acceleration: Recent regulatory activity is a primary demand driver. Notably, the U.S. EPA’s January 2026 rule requires automatic leak detection systems for certain newly installed commercial and industrial refrigeration appliances above a defined refrigerant charge threshold, with retrofit requirements for a subset of existing equipment phased in by January 1, 2027. Separately, the PHMSA Advanced Leak Detection Program (ALDP) standards introduced in January 2025 set performance expectations for pipeline monitoring technologies. These rules convert latent demand into scheduled procurement and create predictable retrofit pipelines for suppliers and service providers.

Automatic Leak Detection Equipment Market

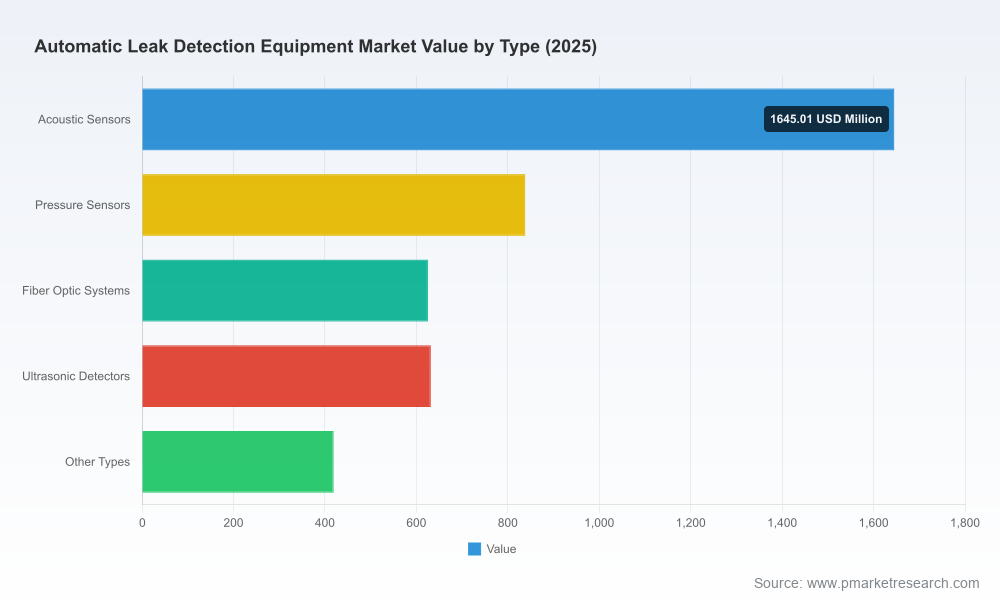

Technology convergence and product evolution: Acoustic correlation, pressure-based testing, fiber-optic distributed sensing, ultrasonic detection, and centralized analytics are moving from niche to standardized building blocks in ALD solutions. Vendors packaging sensor hardware with cloud-native analytics, automated alerts and API-friendly asset integration are increasingly favored by utility and enterprise buyers seeking to simplify operations and demonstrate compliance.

Market structure and concentration: The market exhibits moderate concentration: the top three vendors account for a meaningful share of revenue, and the top five firms represent over half of industry sales. This concentration supports continued technology-driven competition where scale, field service networks and data analytics capabilities differentiate winners.

Procurement cadence and investment windows: The combination of regulatory deadlines and capital planning cycles means C-suite decisions in early-to-mid 2026 will determine vendor selection and rollout schedules for many regulated segments. Early movers with demonstrable compliance case studies and scalable deployment playbooks will secure longer-term service contracts.

Our report profiles the commercial and product strategies of key incumbents and innovative specialists. Selected insights:

InterTech Development Company (Skokie, IL): Known for automated leak and flow test systems leveraging proprietary mass flow and hydraulic technologies, InterTech continues to push into high-speed, precision leak testing for medical-device and wearable manufacturers. Recent trade show engagements demonstrate a push to translate bench-level accuracy into scalable production-line solutions targeting regulated manufacturing segments.

Veeder-Root (Simsbury, CT): A long-established provider of tank gauging and pressurized line leak detection systems, Veeder-Root’s strength is continuous monitoring integrated with regulatory compliance workflows—making it a preferred partner for fuel storage and pipeline operators subject to stringent EPA requirements.

GUTERMANN AG (Zug, Switzerland): A leader in acoustic leak detection and permanent network monitoring, GUTERMANN’s recent product launches emphasize high-sensitivity hydrophone loggers tailored for plastic pipe networks—addressing a growing need for non-invasive, permanent monitoring in distribution systems.

INFICON (Bad Ragaz, Switzerland): INFICON’s portfolio in gas and refrigerant leak detection positions it strategically at the intersection of industrial manufacturing service and refrigeration compliance—areas made more active by recent EPA mandates.

Hermann Sewerin GmbH (Gütersloh, Germany): With a strong heritage in acoustic correlators, ground microphones and locators, Sewerin remains an important supplier to utilities and service contractors that require reliable field diagnostics and localization capabilities.

Recent competitive moves reinforce these positioning plays: in December 2025, GUTERMANN introduced a high-sensitivity hydrophone logger for permanent monitoring in plastic pipe networks, signaling intensified focus on continuous monitoring hardware. In early 2026, InterTech showcased high-resolution leak testing solutions at a major medical-device trade show, illustrating vendor efforts to capture regulated manufacturing procurements. Taken together, these developments highlight vendor differentiation through hardware innovation, field-deployable analytics and industry-specific compliance expertise.

The full PW Consulting report is structured to support immediate decision-making and includes:

Macro forecasts (2020–2032) with scenario sensitivities linked to regulatory implementation timelines.

Technology roadmaps showing maturity curves for acoustic, pressure, fiber-optic, ultrasonic and hybrid systems, and guidance on integration with asset management and SCADA environments.

Buyer persona and procurement-pathway maps for utilities, pipeline operators, industrial manufacturers and commercial real estate owners—detailing evaluation criteria, budget cycles and common barriers to procurement.

A competitor playbook with capability matrices, recent product launches, partnership patterns and likely acquisition targets.

Go-to-market recommendations, including channel strategies, pricing frameworks for capex vs. O&M (monitoring-as-a-service) models, and pilot-to-scale deployment templates.

Risk and mitigation frameworks covering supply-chain constraints, field-service scaling, data privacy concerns and heterogeneity in regulatory enforcement across jurisdictions.

Note: To preserve the research value of this briefing we have intentionally omitted detailed segment-level tables and region/application share data from this press release. The full dataset and granular segmentation tables are available in the complete report.

Compliance-first posture for regulated customers: Firms serving refrigeration, pipeline and large-scale industrial sectors should prioritize certification, pre-qualification and joint pilots that demonstrate compliance to EPA and PHMSA standards. Contracts that bundle hardware with guaranteed compliance milestones will outcompete hardware-only offers.

Shift to outcomes-based commercial models: Transitioning from one-off hardware sales to subscription or performance-based models (e.g., monitoring-as-a-service, uptime and leak-detection SLA guarantees) will increase customer retention and create predictable revenue streams as retrofit programs scale.

Invest in field service and data ops: Deployments at scale require service networks and data engineering teams capable of ingesting high-frequency sensor streams and converting alerts into prioritized work orders. Early investment in these capabilities shortens ramp times and improves customer economics.

Pursue selective M&A and partnerships: Given moderate market concentration and fragmented technology niches, strategic bolt-ons—targeting analytics startups, fiber-optic system integrators or local service contractors—offer rapid capability expansion and faster entry into new geographies.

Differentiate on interoperability and lifecycle cost: Buyers increasingly evaluate total cost of ownership. Vendors that emphasize open APIs, ease of retrofitting, and clear upgrade paths for sensor generations will win procurement competitions.

Prepare for accelerated retrofit waves: With some regulatory retrofit deadlines concentrated within the next 12–18 months, companies that pre-deploy pilot kits and create pre-approved retrofit bundles will shorten sales cycles and secure priority rollouts.

PW Consulting’s ALD market study combines quantitative forecasts with qualitative, field-validated insights. For clients preparing 2026 strategic plans we offer tailored workshops to: map regulatory impact on addressable spend; validate go-to-market tactics by buyer segment; run M&A target screening; and stress-test commercial models under alternative enforcement scenarios. Our deliverables accelerate time-to-decision while preserving downstream value capture across installed bases.

The automatic leak detection market presents a compelling growth opportunity for suppliers, integrators, and service providers in 2026. Regulatory mandates create a near-term demand horizon; technology evolution and shifting commercial models create durable long-term value. Executives that act now—aligning product roadmaps, compliance credentials and field service scale—will convert regulatory compliance cycles into a sustained competitive advantage.

Access to the full report, including the complete segmentation tables, regional and application-level analyses, and our proprietary datasets, is available via the PW Consulting publication page. The detailed numbers and modelled scenarios will enable procurement teams, product leaders and corporate strategists to operationalize a 2026 roadmap with confidence.

For detailed analysis of this topic, please visit the official page:Automatic Leak Detection Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com