Propiverine Market Revenue Analysis and Future Growth Opportunities

Health |

2026-06-03 14:12:00

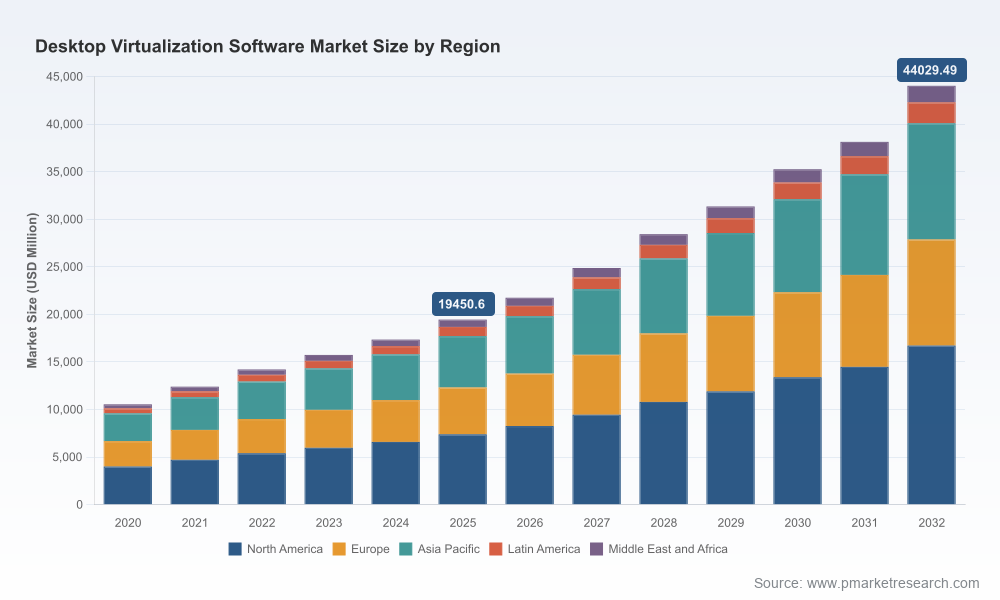

PW Consulting’s latest Desktop Virtualization Software Market report (base year 2025) delivers an evidence-backed roadmap for enterprise leaders, CIOs, and technology procurement teams making strategic decisions in 2026. After a period of accelerated adoption between 2020 and 2025—in which the global market nearly doubled in scale—the market is now set to continue robust expansion. Our analysis forecasts a compound annual growth rate (CAGR) of 12.38% across the 2026–2032 forecast window, taking the market from a 2025 base to a materially larger industry by 2032. At the same time, market concentration data indicate that the sector remains top-heavy: the three largest vendors command a substantial share of the market, and the five largest capture an even larger portion, reinforcing the importance of strategic vendor selection.

Desktop Virtualization Software Market

Timing of investment: With the market trending to double-digit growth, organizations must decide whether to accelerate cloud-first or hybrid desktop virtualization initiatives in 2026 to capture operational and security benefits while pricing and vendor dynamics remain favorable.

Desktop Virtualization Software Market

Vendor concentration and lock-in risk: The market exhibits significant concentration among the leading vendors. That creates advantages—mature tooling, ecosystem integration, global scale—but it also creates migration and licensing lock-in risks that should be explicitly evaluated during vendor selection.

Desktop Virtualization Software Market

Regulatory and compliance overlay: Desktop virtualization is increasingly the default architecture for regulated workloads, but compliance requirements (HIPAA, PCI-DSS, GDPR) and data-residency risk (e.g., implications of extraterritorial law enforcement access) raise architectural and contractual imperatives that must be addressed up front.

Total cost of ownership (TCO) complexity: Advanced security and monitoring modules, Zero Trust enforcement, and device compliance tooling are often sold as add-ons. Procurement and finance teams should model incremental operational costs, not just license and infrastructure fees.

From 2020 through 2025 the market experienced rapid uptake driven by remote-work acceleration, security modernization, and cloud migration programs. Entering 2026, the market’s growth is being sustained by three structural forces:

Hybrid and cloud-native enterprise architectures — Organizations are balancing centralized management with localized performance and compliance needs, pushing demand for flexible deployment models.

Security and compliance as purchase determinants — Adoption is tightly coupled to the ability to deliver workload isolation, endpoint posture checks, data exfiltration controls, and auditable logging that satisfy industry regulators.

Platform consolidation among major cloud and virtualization providers — This reduces fragmentation for some buyers but increases price and feature negotiation complexity for others.

The vendor field combines hyperscale cloud providers, specialist VDI vendors, and converged infrastructure suppliers. Strategic differentiators center on cloud integration, hybrid capability, performance protocols, licensing models, and partner ecosystems.

Microsoft Corporation (Azure Virtual Desktop, Windows 365) — Strengths: deep integration with Microsoft 365, multi-session optimization and a broad hybrid options set. Microsoft’s platform-level moves (including App Attach support for newer server session hosts) signal continued emphasis on enterprise migration ease and manageability.

Amazon Web Services (Amazon WorkSpaces) — Strengths: managed desktop-as-a-service with flexible pricing and expanding regional availability. Recent product updates and regional rollouts underscore AWS’s intent to make WorkSpaces a first-class option for both Windows and Linux workloads while rolling in enhanced platform security primitives.

Citrix Systems — Strengths: mature virtualization protocols for high-performance remoting and a long-standing position in regulated sectors. Recent licensing policy changes—mandating a cloud-based License Activation Service—have immediate operational implications for existing customers and should be a negotiation point for renewals and migrations.

Omnissa (formerly VMware) — Strengths: enterprise-grade on-premises and hybrid VDI, favored by organizations with large existing virtualization footprints. Rebranding and platform evolution make integration paths a key evaluation item for customers with hybrid requirements.

Nutanix — Strengths: unified infrastructure approach and increasing hybrid-cloud enablement. Partnerships that enable hybrid AVD deployments point to a “best-of-both-worlds” strategy that can reduce friction for customers seeking seamless on-prem/cloud operations.

Parallels — Strengths: cost-effective RAS solutions for SMBs and distributed workforces; appeals to buyers seeking simpler licensing and operational models.

Inuvika — Strengths: open-source, Linux-focused alternatives for customers seeking cost containment and avoidance of major vendor lock-in.

Oracle Corporation — Strengths: integrated OCI offerings that appeal to heavy Oracle-stack customers who value co-location with database and enterprise cloud services.

These vendor profiles highlight different trade-offs. Hyperscalers emphasize global scale and continuous platform innovation; specialist VDI vendors provide performance-centric remoting and maturity in regulated verticals; newer entrants and open-source alternatives provide targeted value propositions for cost-sensitive or niche technical environments.

AWS’s expanded regional footprint and support for newer Windows Server editions strengthen its proposition for global enterprises requiring local presence and modern session-host support. For buyers, this reduces latency and compliance hurdles but requires renewed diligence on regional pricing and contractual terms.

Microsoft’s enhancements to application delivery and session host support accelerate lift-and-shift opportunities for Windows-centric workloads. Enterprises that have standardized on Microsoft stacks should consider phased migrations combined with performance testing to validate multi-session designs.

Nutanix’s partnership activity to support hybrid AVD scenarios signals a path for organizations that want an AHV-first strategy without sacrificing cloud interoperability.

Citrix’s mandatory cloud licensing activation policy is a reminder that licensing architecture changes can be as disruptive as technical migrations. Buyers must bake license transition plans into their 2026 roadmaps to avoid service interruptions.

Our report is intentionally operational in scope, designed to support procurement decisions and migration roadmaps in 2026. Deliverables include:

Top-line historic and forecast market sizing (base year 2025 and forecasts through 2032) and scenario sensitivities that translate macro growth into procurement timing signals.

Vendor scorecards and a competitive matrix comparing performance protocols, hybrid enablement, licensing complexity, ecosystem integrations, and support footprints.

Negotiation playbooks and a list of commercial levers (subscription terms, regional commitments, seat tiers, and managed-services bundling) tailored for different buyer archetypes.

Deployment playbooks and a phased migration checklist covering proof-of-concept design, pilot sizing heuristics, security posture gates, and cutover sequencing.

Operational cost models and TCO frameworks that explicitly separate licensing, infrastructure, and ongoing security/management add-ons—enabling apples-to-apples comparison across vendors.

Regulatory mapping and data-residency risk analysis that identifies when specific vendor choices may trigger additional contractual or architectural constraints.

M&A and partnership heatmaps to identify potential acquisition targets and alliance partners that accelerate time-to-value for strategic customers.

Adopt a use-case-first vendor strategy: segment your desktop virtualization use cases (knowledge workers, power users, regulated workloads, contractor access) and let those profiles drive vendor shortlists rather than broad “cloud-first” mandates.

Insist on realistic TCO modeling: include security modules, monitoring, and compliance-related services as line items rather than optional extras when comparing proposals.

Plan licensing transitions explicitly: any vendor license architecture change (for example, cloud-based activation mandates) should be on the program risk register and linked to contractual SLAs and migration timelines.

Design hybrid pilot patterns: use hybrid pilots that validate both connectivity and policy enforcement across on-prem and cloud session hosts to avoid surprises at scale.

Use regional and legal risk filters early: build data-residency, export-control, and law-enforcement-access constraints into vendor-selection criteria where applicable.

Maintain negotiation flexibility: prioritise vendors offering transparent pricing bands, easily auditable usage metrics, and clear exit gates to preserve future optionality.

This brief is a high-level synthesis of the full PW Consulting desktop virtualization market study. The full report includes the granular datasets, regional and deployment-mode revenue breakdowns, vendor market shares, and detailed financial models that enterprise teams need to finalize vendor selection and procurement strategies. If you are preparing a 2026 roadmap—or evaluating proof-of-concept and enterprise pilots—our report provides the playbooks, models, and checklists to de-risk your program and align procurement, security, and operations on a single migration timeline.

Desktop virtualization is at an inflection point: market growth remains strong, vendor ecosystems are consolidating, and regulatory and licensing shifts are raising the operational stakes for enterprises. PW Consulting’s study translates these market dynamics into pragmatic guidance, enabling decision-makers to convert strategic intent into executable 2026 programs. Access to the full dataset and implementation workstreams is available through the PW Consulting report portal—where our complete vendor benchmarking, scenario models, and implementation templates can be downloaded to support your 2026 execution plan.

For detailed analysis of this topic, please visit the official page:Desktop Virtualization Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com