North America CAD Software Market Analysis, Share and Growth Forecast 2034

Technology |

2026-06-25 13:20:09

PW Consulting’s new Autostereoscopic Displays Market report (base year 2025; historical 2020–2025; forecast 2026–2032) articulates why 2026 is the first full year in which glasses-free 3D display technologies move from early adopter showcases into scalable commercial deployments. Backed by robust market modeling (CAGR 17.88% across the 2026–2032 forecast window), our analysis finds the global market more than doubling since 2020 and accelerating into a multi-billion-dollar industry by the end of the forecast period. For executives planning supply-chain allocation, R&D spend, M&A, or go-to-market entry in 2026, this brief explains the strategic value of the full report and highlights the operational levers that will determine winners and losers.

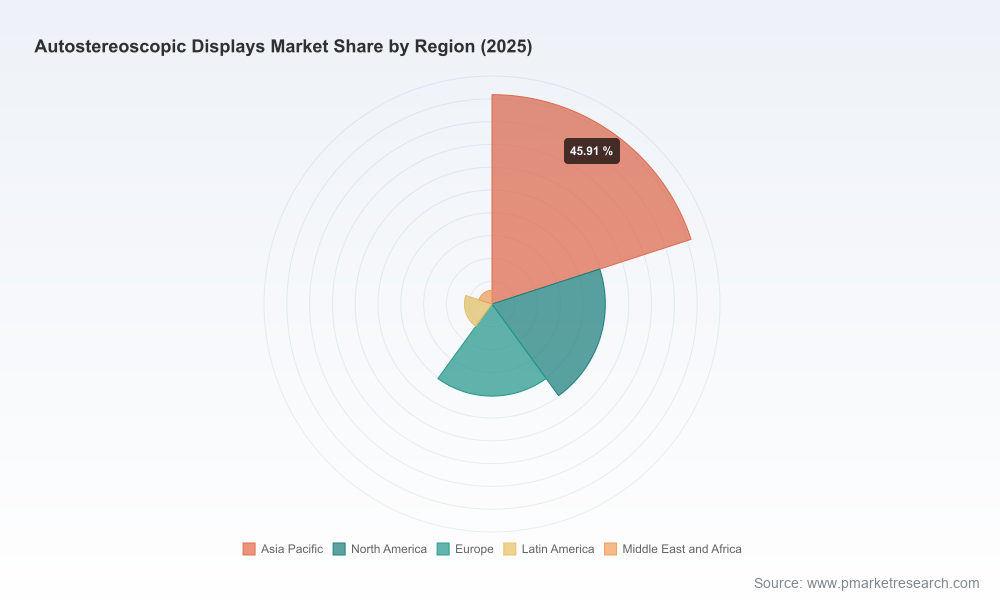

Autostereoscopic Displays Market

Technology convergence: Multiple autostereoscopic approaches (lenticular optics, parallax barriers, directional backlights, switchable light-field stacks and head-tracking solutions) are reaching product-grade maturity simultaneously. Recent product introductions and trade-show demonstrations during late 2025 and early 2026 show manufacturable form factors from handheld monitors up to large-format signage and medical-grade displays — enabling broader use-case coverage.

Autostereoscopic Displays Market

Commercial validation across verticals: Pilots and early deployments in digital signage, medical visualization, retail experiential displays, and consumer device demonstrations indicate pathway-to-revenue for suppliers beyond bespoke installations. That pathway is reflected in our market sizing where the installed base and replacement cycles support strong near-term revenue expansion compared with the 2020–2024 period.

Autostereoscopic Displays Market

Supply-chain and policy shocks turning strategic: Tariff shifts and policy actions (notably U.S. reciprocal tariffs introduced in 2025 and ongoing duties targeted at critical display cells) plus material-constrained optical supply chains change the calculus for localization, dual-sourcing and inventory strategy. These externalities make 2026 a planning deadline for firms seeking to avoid punitive margin and time-to-market impacts.

Our competitive mapping synthesizes company-level R&D trajectories, product roadmaps, distribution footprints and partner ecosystems. Selected incumbent and challenger positions are summarized below to illustrate strategic options for alliance, acquisition, and differentiation.

Magnetic 3D (New York, USA) — a pioneer in large-format glasses-free 3D for digital signage and enterprise visualization. Recent launches (including a new 43” Wildfire multiview unit in mid-2026) position Magnetic 3D as a practical partner for national and retail rollouts where turnkey hardware and content services matter.

Alioscopy (Paris, France) — known for high-precision lenticular manufacturing and high-resolution professional monitors. Their work on ultra-high-resolution panels targets industries where optical fidelity and pixel-level accuracy are decisive (medical, engineering visualization).

Leia Inc. (USA) — developing switchable light-field and spatial-AI platforms for consumer devices. Leia’s software-first approach and device partnerships make it a strategic ally for OEMs that want to enable glasses-free experiences without lengthy optics retooling.

Dimenco (Netherlands), 3D Global Solutions (Germany), Philips, Samsung, Barco, MOPIC, LG — range from specialty head-tracking and lenticular integrators to large display OEMs with deep channels. Together they create a competitive spectrum where solutions vary by image quality, interactivity, scale, and regulatory compliance.

Recent announcements (product launches from Magnetic 3D, Barco and MOPIC in late 2025; Zondision and other light-field monitor entries in early 2026; demonstrations at ISE 2026) confirm an active commercialization phase. For strategy teams, the implication is clear: choose partnership and procurement targets now while vendors still differentiate on product architecture and integration services.

Trade policy and tariffs: Heightened U.S.–China trade measures and reciprocal tariffs introduced in 2025 create potential duty exposure for display assemblies and optical components. Planning scenarios should include tariff pass-through, qualification of exempted product classes, and remediation timelines tied to national security reviews.

Supply constraints for optical materials: Optical films, parallax barriers, and AMOLED inputs are concentrated in Asia. Tariff uncertainty amplifies input cost volatility — a critical factor for margin modeling and for deciding whether to invest in vertical integration or secure long-term supplier contracts.

Manufacturing cost geography: Asian manufacturing retains a material labor and proximity advantage (our sector analysis indicates a 28–35% cost edge in relevant production scenarios versus Europe/North America). For many commercial programs this favors Asia-based production with nearshoring or dual-sourcing as risk mitigants.

Technology substitution risk: Advances in switchable light-field stacks, ASIC-enabled eye-tracking, and novel optics (including metalens research) mean that product roadmaps must include upgrade paths and modularity to avoid obsolescence for units intended to be in service multiple years.

The PW Consulting report goes beyond narrative to provide operational tools executives use in 2026 planning cycles. Highlights include:

Proven market-sizing and forecasting models (base year 2025; historical 2020–2025; forecast 2026–2032) with sensitivity scenarios that reflect tariff, price, and adoption-rate variance.

Technology readiness and cost curves for lenticular, parallax, directional backlight and switchable light-field approaches — practical guidance for platform selection by use case and TCO horizon.

Supply-chain stress-tests and a supplier-qualification framework that integrates tariff exposure, material sourcing concentration, and manufacturing cost differentials by geography.

Commercial playbooks for three priority verticals (enterprise signage & retail experience, medical visualization, and consumer/handheld devices) that lay out deployment timelines, content infrastructure needs, pricing strategies and pilot-to-scale pathways.

Financial templates for evaluating capex vs. outsourcing, M&A target screens focused on strategic assets (optical IP, ASICs, systems integration) and partnership architectures for go-to-market acceleration.

To preserve the strategic value of the research, this release intentionally omits the granular segment-by-segment figures available in the report. The full study contains detailed regional, type and application breakdowns and interactive models that are essential for sourcing decisions, budgeting and investor diligence—access to those tables is available on the report landing page.

Lock down supply flexibility: Initiate dual-sourcing pilots for optical films and parallax components, and run tariff-impact simulations now. For larger programs, negotiate multi-year agreements with staggered delivery clauses to smooth price volatility.

Prioritize modular product architectures: Design displays with replaceable optics or upgrade bays so customers can adopt improved light-field or metalens modules without full unit replacement — this protects installed-base value and supports premium aftermarket revenue.

Localize selectively: For high-volume signage and medical units where lead-time and regulatory compliance matter, evaluate nearshoring production in lower-cost Asian hubs while maintaining a small European/North American line for certified medical SKUs.

Partner for content and deployment: Delivery of glasses-free 3D is as much about content pipeline and calibration as it is about optics. Forge partnerships with content studios, system integrators and signage networks early in pilot phases.

Invest in software and AI for spatial UX: Spatial-AI and eye-tracking dramatically improve perceived quality and reduce optical constraints. Consider licensing spatial stacks or co-developing software to differentiate on user experience rather than purely on optical hardware.

Use M&A strategically: Target acquisitions that buy you critical optical IP, custom ASIC capability, or integration expertise. Our report’s M&A playbook helps prioritize targets by synergy and integration risk.

Autostereoscopic display technologies are transitioning from demonstration to deployment. Our report quantifies that transition and provides the operational playbook companies need to translate technological promise into profitable programs. With a base year anchored in 2025 and a forecast horizon through 2032, the analysis equips C-suite and business unit leaders to model multiple commercial and policy scenarios, select partners strategically, and structure manufacturing and R&D investments to maximize upside while managing tariff and supply risks.

For firms making budget, sourcing, or M&A decisions in 2026, this study is not background reading — it is a decision support system. PW Consulting’s full report contains the granular segmentation, interactive financial models, and supplier-level intelligence necessary to operationalize these recommendations. Visit our report page or contact PW Consulting’s Autostereoscopic Displays team to request the complete dataset, executive briefing, or a tailored strategic workshop.

For detailed analysis of this topic, please visit the official page:Autostereoscopic Displays Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com