Fluorescent Lighting Market: Strategic Imperatives for 2026

As PW Consulting’s senior industry analyst, I present an executive briefing drawn from our latest Fluorescent Lighting Market report. The research synthesizes five years of historical performance (2020–2025) and provides a seven-year forecast horizon (2026–2032) to equip executives, investors, and procurement leaders with the context and decision tools they need for 2026. The market is contracting on a structural basis—our consolidated modeling shows a compounded annual decline of approximately 11.5% across the forecast window—creating a set of urgent strategic choices for incumbents and adjacent players alike.

Fluorescent Lighting Market

Why 2026 Is a Pivotal Year

Two regulatory inflection points and persistent technology substitution dynamics converge to make 2026 the decisive planning year for companies with exposure to fluorescent lamp value chains. New global mercury limits and a tightening regulatory environment have accelerated capex reallocation and product rationalization. At the same time, LED migration—now mature in many end markets—has shifted fluorescent demand into a lower-volume, higher-compliance niche. Our forecasts capture this transition and its implications for revenue, cost structure, and competitive positioning.

Fluorescent Lighting Market

- Market trajectory: The sector has experienced a marked decline from the early-2020s baseline and our consolidated model projects continued contraction through 2032, reinforcing the need for portfolio and balance-sheet stress testing.

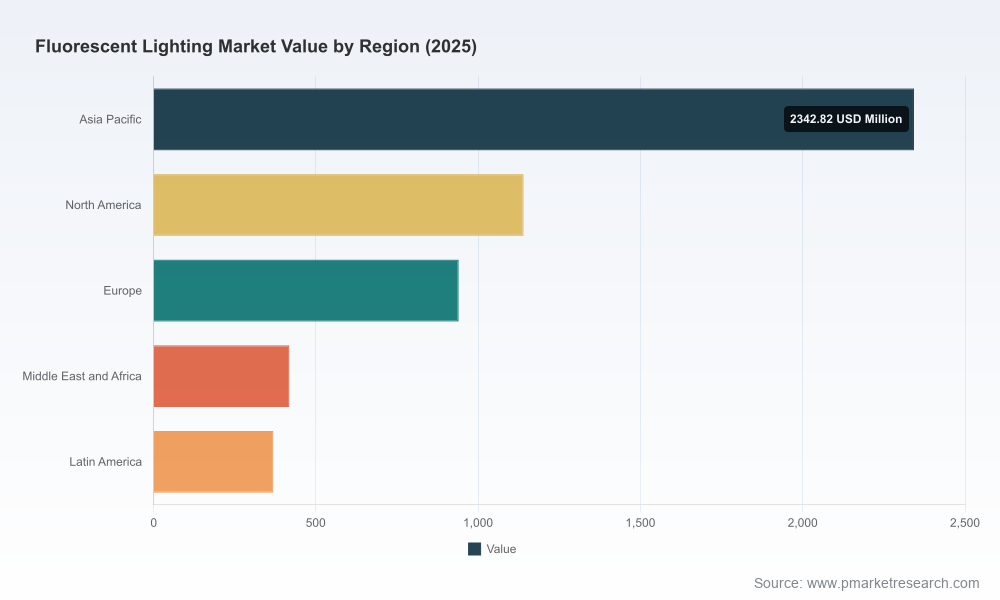

- Concentration dynamics: Market concentration is meaningful but not monopolistic; top-tier firms control a material share of the market, creating advantages in scale economies and compliance investments. This creates both barriers and opportunities for nimble challengers.

- Regulatory accelerants: Recent and upcoming regulation—most notably stringent mercury limits and regional phase-outs of specific lamp classes—are forcing product redesigns and supply-chain reconfiguration ahead of many procurement cycles.

Core Macro Findings (High-Level)

Our model, validated against historical corporate disclosures and trade data, shows a clear downtrend in aggregate industry revenue between 2020 and 2025 and extends this trajectory into the 2026–2032 forecast period. The cumulative effect of technology substitution, regulatory restrictions, and trade friction produces a negative compound annual growth rate of roughly 11.5% over the forecast window. This is a structural decline rather than a cyclical dip—meaning many business models premised on volume continuity will require strategic reorientation.

Fluorescent Lighting Market

What the Full Report Contains (Operationally Actionable)

To translate market insight into executable plans for 2026, the full PW Consulting report includes the following practical deliverables (summarized):

- Granular historical and forecast revenue models with scenario toggles for regulatory timelines, tariff regimes, and LED-adoption curves.

- Company benchmarking frameworks and supplier scorecards that evaluate scale, product portfolio resilience, regulatory preparedness, and go-to-market effectiveness.

- Regulatory impact matrices covering regional bans, mercury thresholds, and compliance timelines—mapped to product lines and SKU-level risk profiles.

- Cost-to-serve and margin analyses that isolate the impact of compliance-driven redesigns, rare-earth supply pressure, and tariff exposure on gross margins and working capital.

- Practical playbooks for procurement, including hedging strategies for rare-earths, contract clauses for regulatory change, and inventory rationalization templates tailored to retrofit-focused demand.

- Scenario-based M&A screeners and divestiture criteria to identify targets or non-core businesses suitable for consolidation or exit under varying recovery assumptions.

We intentionally withhold segment-level dollar breakdowns in this briefing—those detailed tables, time-series, and downloadable models are available within the full report to paying subscribers and clients. This briefing is a strategic preview designed to demonstrate the analysis depth while protecting the primary research assets.

Competitive Landscape: Strengths and Strategic Routes

The competitive map remains anchored by established lighting manufacturers, regional champions in emerging markets, and a growing set of hybrid/LED-focused incumbents. Our assessment emphasizes capability clusters rather than raw market shares to highlight actionable competitive moves:

- Global OEMs with scale (e.g., Signify Holding): Scale supports compliance investments, global distribution, and retrofit service bundles. These firms are best positioned to convert installed-base service contracts into recurring revenue streams.

- European and Japanese professional brands (e.g., LEDVANCE, Panasonic): Technical depth and channel relationships enable premium positioning for regulated or specification-heavy projects, particularly in institutional and commercial tenders.

- Large Asian manufacturers and regional leaders (e.g., Opple, NVC, Havells, Crompton): Strong cost-to-serve, rapid SKU rotation, and deep domestic channels support resilience in price-sensitive markets, though tariff and raw-material exposure can compress margins.

- North American specialists and distributors (e.g., Satco, Westinghouse, MaxLite): Distribution-led models and retrofit-focused hybrids provide pathways to serve replacement demand, niche specialty segments, and legacy systems where LED conversion is slower.

Each company cluster faces different strategic imperatives: scale players must optimize capital allocation between legacy products and LED service portfolios; regional champions must de-risk supply chains and upgrade product compliance; distributors should accelerate aftermarket and retrofit services where margin pools persist.

Regulatory and Supply-Chain Risks to Prioritize

- Mercury limits and product redesign: The global limit on mercury content effective from 2026 mandates product reformulation or redesign for many existing SKUs. Firms that delay will face market access constraints and potential liability.

- Regional phase-outs: Several jurisdictions have already removed specific lamp classes from permitted sale, accelerating obsolescence of certain SKUs and tightening the replacement market dynamics.

- Raw-material concentration: Phosphors and some rare-earth inputs remain heavily sourced from a single supplier geography—this concentration creates price and availability shocks that directly affect product cost baselines.

- Trade measures: Select markets maintain elevated tariffs on imports from certain origins, reshaping near-term sourcing decisions and total landed cost calculations.

Strategic Playbook for 2026 Decision-Makers

Against the headwinds described, we recommend a three-track strategic approach for organizations planning 2026 actions:

- Protect core cash flow: Rationalize SKU portfolios to eliminate non-compliant and low-margin SKUs; negotiate supply contracts with clauses for regulatory change; prioritize aftermarket and service pathways that convert one-time sales into recurring revenue.

- Reallocate to growth adjacencies: Accelerate development or acquisition of LED and hybrid technologies, retrofit services, and lighting-as-a-service models. Use M&A selectively to acquire compliance expertise or channel reach rather than pure production capacity.

- Hedge supply-chain exposure: Build supplier redundancy for critical phosphors and rare-earths, explore local sourcing options where tariffs apply, and create dynamic procurement models to manage cost volatility.

Scenario Planning: Four Plausible 2026 Pathways

Our report operationalizes four scenarios executives should stress-test their 2026 plans against:

- Base case: Continued LED substitution and phased regulatory compliance—gradual revenue contraction consistent with the forecast CAGR.

- Accelerated retrofit: Faster-than-expected LED conversions in commercial and industrial segments, compressing fluorescent demand more quickly but increasing service and retrofit opportunities.

- Regulatory shock: Stricter-than-expected implementation timelines or expanded bans accelerate obsolescence and create short-term supply dislocations.

- Raw-material shock: Disruption in rare-earth or phosphor supply chains elevates costs, forcing rapid pricing and sourcing responses.

Decision-makers should run capital-allocation simulations across these scenarios to determine minimum viable scale, acceptable margin thresholds, and go/no-go parameters for new investments entering 2026.

How PW Consulting’s Deliverables Translate to Measurable Outcomes

- Short-term: Reduced inventory write-offs through SKU rationalization templates and prioritized compliance roadmaps.

- Medium-term: Improved margin resilience via supply-chain hedging and targeted retrofit service rollouts.

- Long-term: Optimized portfolio composition achieved by disciplined M&A screening and strategic exits from declining subsegments.

Next Steps

This briefing intentionally highlights the strategic contours and actionable frameworks emerging from our Fluorescent Lighting Market study while preserving the proprietary segment-level data and company scorecards that underpin our recommendations. For access to the full dataset, detailed segment forecasts, supplier matrices, and the downloadable Excel models that support 2026 planning, please consult the full PW Consulting report and model package.

PW Consulting stands ready to support scenario workshops, custom benchmarking, and implementation roadmaps that translate this analysis into measurable operational and financial outcomes for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Fluorescent Lighting Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com