Monosodium Citrate Market Overview: Key Drivers and Challenges

Other |

2026-04-16 05:57:49

PW Consulting today releases a strategy-focused industry briefing derived from our forthcoming Silicone Resin Market report (base year 2025, forecast 2026–2032). This executive preview translates rigorous market modeling into concrete strategic options for C-suite leaders, corporate strategists, and investors planning moves in 2026. It highlights why silicone resins are a strategic materials play—how value shifts, regulatory pressure, and supply-chain dynamics will shape winners—and what steps companies should be taking now to capture disproportionate value over the coming six years.

Silicone Resin Market

Market scale and growth trajectory: The silicone resin market expanded materially through the early 2020s, rising from roughly USD 4.1 billion in 2020 to an estimated USD 5.52 billion in 2025. Our forecasts project a continuation of steady expansion across 2026–2032 at a compound annual growth rate (CAGR) of approximately 6.22%, with the total market surpassing USD 8.4 billion by 2032 under the base scenario.

Silicone Resin Market

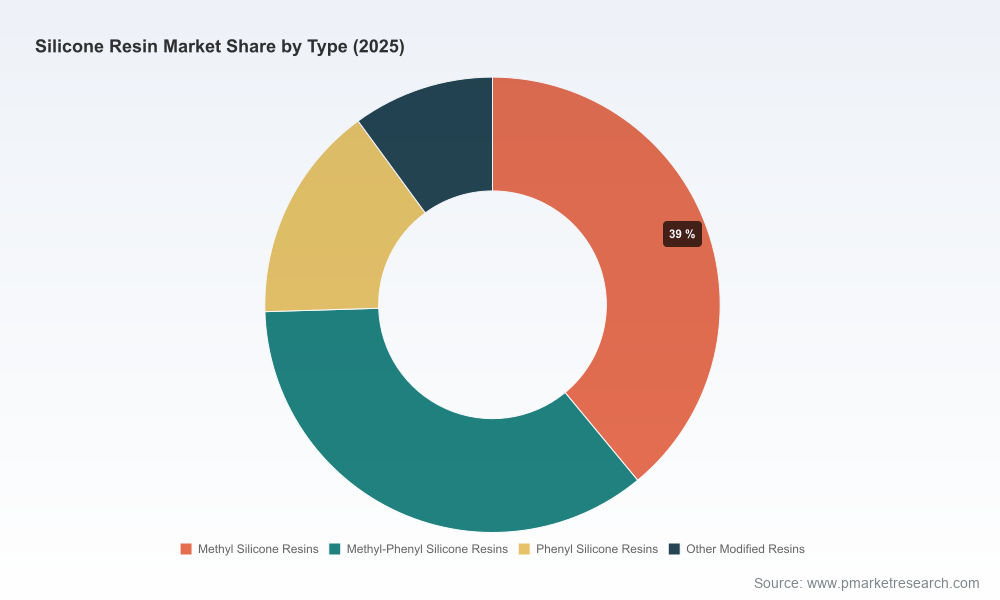

Market structure: Concentration is meaningful but not prohibitive—our analysis shows the top three suppliers account for roughly 41% of supply, while the top five firms together control about 57%. That structure enables both scale advantages for incumbents and tactical opportunities for challengers, especially in specialty niches and application-driven formulations.

Silicone Resin Market

Near-term supply-price drivers: Upstream input cost volatility—exemplified by elevated metallic silicon prices—remains a material margin lever for resin producers. Transport/packaging compliance changes (notably IMO/IMDG updates) and tariff regimes further complicate margin and route-to-market economics in 2026.

Prioritize portfolio segmentation by application value, not just volume. Volume-driven approaches will be outcompeted by players who align product grades to higher-value, regulation-driven uses (e.g., high-temperature coatings and electronics encapsulants). Our scenario work shows product-mix premium capture can outperform pure volume growth in mid-cycle markets.

Elevate regulatory and sustainability compliance to a go-to-market differentiator. Regulatory constraints such as EU REACH limits on specific cyclo-siloxanes and tightening green-building certification rules around fluorinated chemistries are already forcing reformulations. Firms that proactively re-engineer chemistries and obtain third-party certifications will shorten sales cycles and preserve margin in premium channels.

Build optionality into supply chains. Input cost shocks and logistics rule changes—alongside tariff exposures—necessitate multi-sourcing strategies, inventory levers, and selective nearshoring for strategic markets. Scenario models in our report quantify margin impact across alternative sourcing mixes to guide CAPEX and procurement decisions in 2026.

Target verticalized partnerships in electronics and automotive. The transition to higher electrification and electronics density in vehicles and industrial equipment opens routes for resin suppliers to co-develop specialized grades. Joint development agreements and long-term supply contracts will be decisive in locking demand from OEMs and tier-1s.

Our competitive benchmarking examines scale, product breadth, specialty competencies, and supply footprints. Leading global players maintain strong positions through diversified end-market exposure, integrated manufacturing, and established brand trust—yet strategic gaps persist that agile firms can exploit.

Dow (Midland, Michigan, USA) — a leading global producer with a broad SILRES portfolio used across protective coatings, electrical insulation, and molded parts. Recent certification advances and compliance updates reinforce its suitability for regulated markets.

Wacker Chemie AG (Munich, Germany) — a major supplier known for high-temperature coatings and electronics encapsulation applications. Capacity expansions in Europe signal a deliberate move to defend coating demand and shorten lead times for regional customers.

Shin-Etsu Chemical (Tokyo, Japan) — a massive silicone producer with high-volume resin capabilities and strong positions in toners, paints, and sealants. New high-heat-resistant grades for automotive electronics point to an intent to capture emergent OEM electrification needs.

Momentive Performance Materials (Waterford, New York, USA) — focuses on specialty resins for industrial coatings and automotive clearcoats; its product development roadmaps emphasize optical and thermal performance.

Elkem ASA (Oslo, Norway) — offers formulations for electrical varnishes and high-performance coatings, leveraging its electrical-grade materials expertise.

KCC Corporation (Siheung, South Korea) — a regional leader producing silicone resins for paints, inks, and protective electronic coatings; well-positioned to serve Asia-Pacific customer clusters.

Recent corporate moves matter for 2026 sourcing and M&A strategies. Wacker’s European capacity expansion (Oct 2024) underscores regional demand resilience for coatings. Shin-Etsu’s mid-2024 product launches highlight the pace of innovation around high-heat automotive electronics. Dow’s REACH compliance updates (Mar 2024) illustrate how regulatory certification is becoming baseline for large enterprise procurement.

Regulatory constraints: EU-level restrictions on certain cyclic siloxanes and increasing scrutiny of PFAS-like substances are forcing re-formulation in some channels, particularly consumer-facing wash-off products and green-building applications. Firms must model product-composition risk across markets to avoid sudden derating of product acceptability.

Tariff exposure: Existing trade measures such as Section 301 duties materially change landed cost math for some supply corridors. Strategic sourcing and tariff engineering (e.g., use of bonded warehouses, tariff classification review) can recover margin—but require investment in customs expertise.

Logistics & labeling: IMDG/UN packaging and labeling amendments for certain resin shipments increase compliance and freight costs. For customers with global manufacturing, harmonized packaging and documentation are non-negotiable to preserve delivery reliability.

Raw material and energy volatility: Recent commodity moves demonstrate the sensitivity of resin margins to metallic silicon prices and energy inputs. Hedging policies, long-term feedstock contracts, or vertical integration options should be stress-tested in 2026 capital plans.

The full PW Consulting report is designed as a decision-support toolkit for executives, blending quantitative forecasts with hands-on strategic playbooks. Key operational deliverables include:

Market sizing and forecast models with scenario toggles for alternative growth, input-cost, and regulatory pathways—useful for investment prioritization and sensitivity testing.

Competitive benchmarking templates that map product portfolios, technical differentiators, and market footprints to identify whitespace for new grade launches or M&A targets.

Supply-chain stress maps showing tariff, logistics, and raw-material exposure by route-to-market—intended to inform procurement and Treasury hedging strategies.

Go-to-market playbooks for premium segments (e.g., electronics encapsulation, high-temperature coatings), including customer segmentation, value-proposition messaging, and recommended commercial KPIs.

M&A and JV scouting lists with high-level commercial rationales and integration risk checklists, focused on specialty resin technologies and upstream feedstock security.

Practical compliance checklists aligned to prevailing regulations and certification schemes, enabling product managers to prioritize reformulation and testing investments.

Run a margin-impact simulation that incorporates input-cost sensitivity, tariff scenarios, and transport-classification changes for your key SKUs.

Prioritize R&D and certification investments on grades likely to be excluded from green-building or OEM specs if left unchanged.

Audit your supplier network for concentration, single-source exposures, and geographic tariff risk; develop alternate sourcing or inventory strategies for critical feedstocks.

Assess strategic partnerships with OEMs in electronics and automotive to co-develop next-gen formulations and lock long-term offtake.

Run a rapid M&A screening for specialty resin firms with differentiated chemistries or regional manufacturing footprints that can be integrated with limited capex.

As silicone resins move from a largely commodity-associated input into an engineered performance material for electrification and high-durability coatings, firms that combine technical product leadership with supply-chain resilience and regulatory foresight will capture the outsized margins. The market’s steady CAGR and projected expansion to over USD 8 billion by 2032 create a substantive runway—but value will be uneven. Our report equips executives with the models, playbooks, and risk-mitigation frameworks to ensure 2026 investments compound into sustainable competitive advantage.

To access the complete data tables, regional and application breakouts, supplier scorecards, and downloadable scenario models that underpin this briefing, visit the PW Consulting report page. The full report contains the granular segmentation and proprietary forecasting that are deliberately withheld in this executive preview to provide a single authoritative source for subscription clients and transaction teams.

For detailed analysis of this topic, please visit the official page:Silicone Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com