Mobility On Demand Market Drivers and Opportunities by 2034

Other |

2026-04-28 12:31:17

PW Consulting’s latest market research report on Medical Silicone Vasculature Models synthesizes historical performance (2020–2025), a market base year of 2025, and a forward-looking forecast spanning 2026–2032. The sector has demonstrated resilient expansion through 2025, with total industry revenues approaching USD 296 Million in the base year and a projected compound annual growth rate (CAGR) of approximately 7.5% over the forecast horizon. For leadership teams making resource-allocation and innovation decisions in 2026, this study provides the strategic context, risk diagnostics, and execution frameworks required to convert upside into market share.

Medical Silicone Vasculature Models Market

Confluence of clinical need and technology: Clinical demand for anatomically accurate, patient-specific phantoms is increasing across education, device R&D and pre-surgical planning, driven by higher procedural volumes and an emphasis on reproducibility in training and simulated use testing.

Medical Silicone Vasculature Models Market

Commercialization window: With the market size exhibiting steady growth through 2025 and continued expansion projected, 2026 represents a pivotal year for investment — when product differentiation and supply-chain resilience become decisive competitive levers.

Medical Silicone Vasculature Models Market

Regulatory and reimbursement dynamics: Evolving regulatory guidance (including standards referenced in cardiovascular device testing) and growing acceptance of pre-procedural simulation mean early movers who demonstrate compliance and clinical validity will capture premium positioning.

Three macro dynamics dominate the landscape:

Demand-side sophistication: Hospitals, academic centers and medtech OEMs increasingly require high-fidelity, tortuous 3D anatomical models for training and simulated use validation. This demand is not merely volumetric — it skews toward customization, multi-modality compatibility (fluoroscopy, endovascular access, device manipulation), and reproducible mechanical properties.

Technological differentiation: Advances in 3D printing, silicone formulations and composite manufacturing (including hybrid soft-rigid constructs) are raising the bar for anatomical realism and device interaction. Vendors able to marry material science with scalable digital workflows will command higher margins.

Supply-chain & cost sensitivity: Raw material dynamics — notably medical-grade liquid silicone rubber (LSR) pricing — and manufacturing throughput determine unit economics. As of mid‑2025, benchmark LSR pricing in Europe clustered in a narrow range; procurement strategies and vertical integration options are critical to protect pricing models.

Compliance considerations are central to product adoption. Silicone mock vessel testing for cardiovascular devices is commonly benchmarked against established standards (including ISO and ASTM protocols), and regulatory guidance increasingly recommends tortuous, anatomically accurate models for simulated use testing of neurovascular devices. These standards not only shape product design but also influence clinical study endpoints and verification pathways for customers such as device manufacturers.

The competitive structure is best described as moderately concentrated, with the top tiers of suppliers controlling a meaningful but not dominant share of the market. Market concentration metrics indicate room for both established providers and specialized entrants to expand, particularly where differentiated IP or vertical integration exists.

United Biologics (Irvine, CA) — Known for proprietary silicone (AngioClear™) and anatomically representative models tailored for endovascular training and device demonstrations. Their focus on proprietary materials and a clear go-to-market for training and device development highlights a premium-product strategy that leans on material differentiation and clinical credibility.

BDC Laboratories (Wheat Ridge, CO) — Specializes in engineered compliant mock vessels and simulation platforms for cardiovascular testing. BDC’s active engagement at industry trade events signals a business model aimed at partnerships with device OEMs and research institutions where testing fidelity is paramount.

TrandoMed (Ningbo, China) — A high-volume manufacturer of 3D printed silicone vascular models for neuro, coronary and peripheral interventions. Their production capabilities and cost structure illustrate how scale and rapid digital-to-physical workflows can serve OEMs and training networks seeking both customization and competitive pricing.

Elastrat Sàrl (Geneva, Switzerland) — Produces transparent soft and rigid silicone phantoms targeted at education, training and device R&D. Elastrat’s positioning underscores the importance of optical clarity and mechanical property control for research and visualization use cases.

Mentice (Gothenburg, Sweden) — Offers patient-specific silicone and 3D-printed models integrated into simulation platforms. Their blended hardware-software approach is instructive for players considering bundled solutions that tie consumable revenues to simulator ecosystems.

Preclinic Medtech (Shanghai, China) — Focuses on high-simulation models produced via 3D printing for surgical training and device testing. Their activity reflects the growth of regional manufacturing clusters that can serve global customers through export and partnerships.

MedScan3D (Galway, Ireland) — Delivers anatomically precise patient-specific silicone models for healthcare and device testing. Regional specialization and clinical collaboration are core to their approach, emphasizing quality over volume.

Swiss Vascular (Zurich, Switzerland) — An ETH Zurich spin-off delivering anatomically exact, highly transparent cerebral vessel models. Their 2025 launch is a reminder that academic spin-outs with deep R&D roots can rapidly inject advanced capabilities into the market, particularly in niche neurovascular segments.

Industry launches and product introductions continue to surface from academic spin-outs — a sign that research innovation is translating into commercial offerings.

Trade show activity and public demonstrations (ex: early‑2026 events) reveal vendor priorities around partnership development and clinician-facing education — indicators of channels that move the needle for adoption.

Raw material pricing and regulatory clarifications will act as near-term constraints or accelerants depending on how manufacturers hedge and demonstrate compliance.

This study is structured to support immediate decision-making in 2026. Key deliverables include:

A succinct yet evidence-based market sizing model with historical context (2020–2025) and scenario-based forecasts through 2032 to support budgeting and strategic planning.

Market concentration analysis and competitive benchmarking that identifies capability adjacencies, white-space opportunities and potential M&A targets.

Go-to-market frameworks for suppliers and OEM customers, including channel strategies, pricing archetypes and partnership models matched to institutional buyers (training centers, academic hospitals, device R&D).

Manufacturing & sourcing playbook covering material selection, outsourcing vs. vertical integration trade-offs, and unit-cost sensitivity analyses tied to LSR pricing dynamics.

Regulatory alignment checklist and simulated-use study design templates that reconcile ISO/ASTM norms with agency guidance for neurovascular device testing.

Investment decision matrices and a 12–24 month roadmap for capability-building initiatives, from rapid prototyping to scale production and clinical validation.

Prioritize differentiated material science or digital workflow IP. Commodity displacement will intensify; unique combinations of silicone formulations, hybrid composites, and validated mechanical properties are durable advantages.

Lock in supply resilience. Given the sensitivity of unit economics to LSR pricing and availability, form strategic supplier agreements, consider regional stocking hubs, or explore co-development to stabilize raw-material exposure.

Invest in regulatory and clinical validation early. Demonstrable compliance with standard testing protocols and agency expectations is increasingly a commercial precondition for device OEM partnerships.

Match product breadth to channel strategy. Simulation platforms and academic customers value integrated solutions and service-level agreements, while OEMs prioritize reproducible, testable phantoms for validation. Tailor offerings accordingly.

Scan for consolidation targets. Market concentration leaves room for well-capitalized entrants to acquire capability gaps — particularly advanced materials, proprietary printing processes or bundled simulation software.

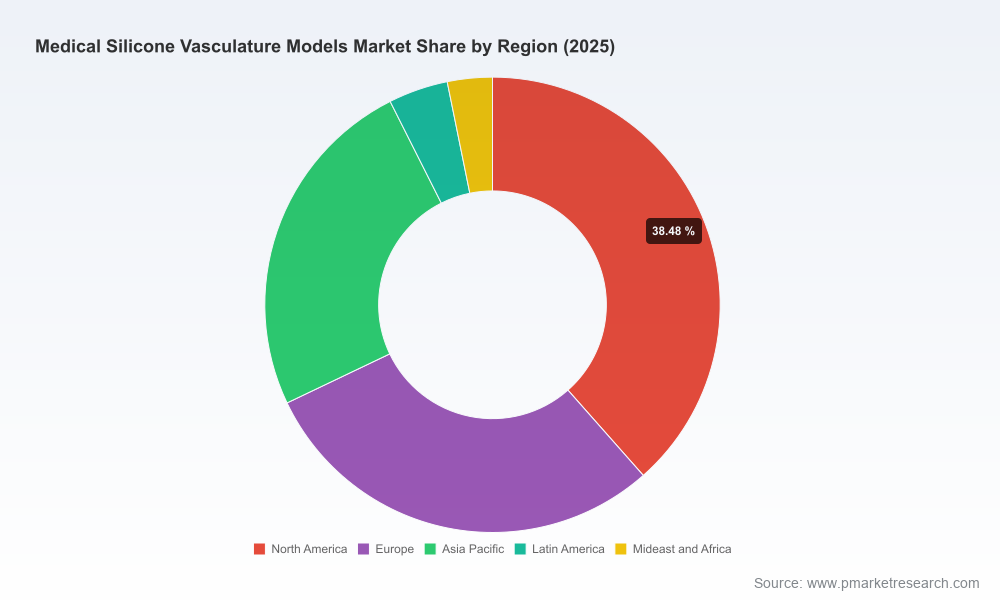

To preserve the strategic integrity of the analysis and to direct executive teams to the utility-grade deliverables, this press brief intentionally omits granular regional breakdowns, application- and type-level dollar splits, and forward-looking share projections by segment. The full PW Consulting report includes the complete split-level modeling, primary-source interview transcripts, manufacturer cost curves, and scenario-specific playbooks that underpin the recommendations summarized above.

For leadership teams preparing budgets, partnership strategies, or M&A pipelines in 2026, PW Consulting offers tailored briefings that contextualize the report findings to your organization’s objectives. Schedule a strategic briefing to receive:

A tailored executive summary mapping to your product roadmap or investment thesis.

Access to our proprietary model with configurable scenarios (price, volume, regulation) and a walk-through of the underlying assumptions.

Introductions to potential partners and prioritised supplier lists based on your risk tolerance and market-entry objectives.

Contact PW Consulting to access the full Medical Silicone Vasculature Models Market report and to arrange a 60‑minute strategy session that turns insight into a quantified action plan for 2026.

For detailed analysis of this topic, please visit the official page:Medical Silicone Vasculature Models Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com