The Unstoppable Momentum Behind the Accelerating Global DevSecOps Market Growth

Other |

2026-06-19 06:48:48

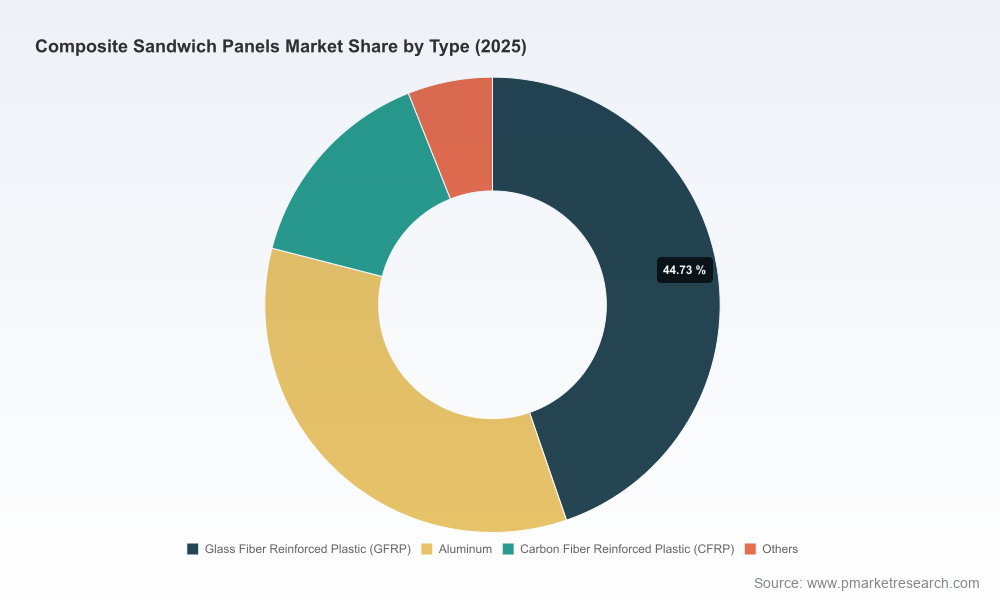

PW Consulting’s latest market intelligence on Composite Sandwich Panels provides a concise, decision-focused preview for executives planning capital allocation, product strategy, and supply-chain moves in 2026. Built on a 2020–2025 historical base and a 2026–2032 forecasting horizon, the research models market dynamics across raw materials, regulation, technology and competition. In plain terms: the global composite sandwich panels market grew from a multi-billion dollar base in 2020 to approximately USD 5,250 Million in 2025, and PW projects sustained expansion at a compounded annual growth rate (CAGR) of 7.15% across 2026–2032, taking the market toward roughly USD 8.52 Billion by 2032.

Composite Sandwich Panels Market

Timing: 2026 is the inflection year for several intersecting forces — tightened fire and building codes, accelerating demand for lightweight structural solutions in transport and renewables, and ongoing cost pressure on petroleum-derived feedstocks. Executives must reconcile near-term procurement exposure with medium-term product roadmaps.

Composite Sandwich Panels Market

Practicality: This preview distills the parts of our full study that matter for board-level trade-offs: revenue trajectory, concentration of supplier power, technology roadmaps, and scenario-tested responses to raw-material shocks.

Composite Sandwich Panels Market

Signal vs. noise: The market shows clear expansion, but winners will be those who pair technical differentiation (advanced cores, certified systems) with resilient sourcing and regulatory alignment.

Executive dashboard: headline market size, 2020–2025 historical series, and 2026–2032 forecast model with sensitivity bands for oil-price and regulatory stress tests.

Demand drivers and segmentation logic: robust methodology for regional, product-type and application modelling (note: detailed splits are available in the full report to subscribers).

Raw-material intelligence: cost pass-through analysis for PUR/PIR foams, PVC foams, honeycomb cores, thermoplastics and resins, and scenario mapping for feedstock volatility.

Regulatory and standards matrix: fire performance, thermal insulation targets, and certification pathways for construction, aerospace and transport segments.

Competitive intelligence: profile dossiers, capability maps and a transaction watchlist focused on manufacturing scaling, core technologies and certification milestones.

Playbooks and case studies: go-to-market approaches, partner models (JV, tolling, captive supply), and prioritized capex vs outsourcing decision trees.

Supplier risk map: tiered exposure assessment and mitigation levers for logistics, single-sourcing and feedstock concentration.

Raw-material tension: Polyurethane (PUR) and polyisocyanurate (PIR) foam cores and petroleum-derived resins remain primary cost drivers; volatility in oil markets translates rapidly into margin pressure for panel producers who lack hedging or flexible formulations.

Honeycomb core evolution: Honeycomb cores are increasingly dominant in high-value applications. The broader honeycomb market underpins much of demand for structural sandwich solutions and is itself a focal point for cost and capability investments.

Thermoplastics and recyclability: Thermoplastic cores and recycled polyolefins are moving from niche to mainstream in segments where end-of-life and circularity matter (notably automotive and modular construction).

Regulatory acceleration: Stricter fire-safety and energy-efficiency standards are forcing reformulation and re-certification; products that combine low embodied carbon with improved fire performance will capture premium specification slots.

Price vs. performance trade-offs: Buyers in construction prioritize cost and speed; aerospace and defense buyers value certified structural performance — manufacturers that can cost-segment their portfolio stand to expand share.

The sector displays moderate concentration: the top three firms control roughly one-third of organized market demand, while the top five capture under half. This leaves room for regional champions, specialized suppliers and vertically integrated players to succeed — particularly where product certification, scale of production and distribution strength create barriers.

Kingspan Group (Ireland): recognized for insulated composite panels and advanced core technologies emphasizing thermal efficiency and fire safety. Strategy signal: double down on envelope solutions for energy-regulated markets.

Hexcel Corporation (United States): advanced honeycomb cores and aerospace-grade sandwich systems with a continued focus on high strength-to-weight ratios. Strategy signal: certification milestones and mid-temperature core innovations are runway items for aerostructures.

The Gill Corporation (United States): custom multi-opening press production for transportation and aerospace — a specialist play in high-value, low-volume segments.

ArcelorMittal and Tata Steel: traditional metal-faced panel expertise with product lines engineered for load-bearing and industrial roofing — incumbency in construction and industrial building applications remains a strategic moat.

Regional and specialist players (Assan Panel, Nucor, DANA Group, 3A Composites, EconCore, and multiple US OEMs): a mix of capacity expansion, product launches and recent certifications (notably thermoplastic and honeycomb systems) points to a dual dynamic of consolidation and targeted differentiation.

Recent signals to note: capacity expansions and new product certifications across the industry (capacity increases in thermoplastic fiberglass production; aerospace-focused out-of-autoclave certifications; mid-temperature honeycomb launches; and new roof-panel systems) indicate manufacturers are positioning for both volume growth and higher-spec niches.

Hedge feedstock exposure. Implement a two-pronged approach: tactical hedges for immediate cost stability and strategic supplier diversification to gain access to thermoplastic and recycled-core options.

Prioritize certification paths. For firms targeting transport and aerospace, accelerate NCAMP/airworthiness-equivalent certifications; for construction-focused players, secure fire-rating and low-U-value endorsements aligned with new codes.

Segment your portfolio. Separate low-margin, high-volume commodity panels from differentiated high-margin structural/insulated systems and align manufacturing footprints accordingly.

Choose capacity expansions deliberately. Greenfield builds must be validated against local feedstock, labor and logistics economics; alternative routes (contract manufacturing, tolling or JV) can achieve flexible scale at lower capital intensity.

Pursue modular and renewables adjacencies. Opportunities in prefabricated modular construction and structural components for wind and transport present faster routes to margin improvement.

Embed sustainability in procurement. Buyers are increasingly demanding recycled-content cores and low-carbon binders; early movers will capture premium specification positions and reduce future regulatory risk.

Operationalize a supplier-risk dashboard. Map single-source nodes, logistics choke points, and regulatory dependencies; maintain prioritized mitigation plans for the top 10 risks.

Use M&A selectively. Target bolt-on capabilities (e.g., certified honeycomb cores, thermoplastic process know-how, or regional distribution networks) rather than indiscriminate scale plays.

PW Consulting combines market modeling, technology due diligence and deal advisory to convert the perspectives above into executable plans. For 2026 we offer three immediate engagement tracks: (1) rapid diagnostics — an eight-week prioritized actions roadmap; (2) sourcing and supplier-risk redesign — procurement re-alignment and hedging playbooks; and (3) M&A and JV origination — target screening, valuation yardsticks and integration planning.

Note: this briefing deliberately omits the granular region-by-region, type-by-type and application-by-application splits that underpin our forecast model. Those decompositions — including regional demand curves, product-type margins, and application-specific price elasticities — are provided in full in the primary report and are essential for transaction-level and plant-level decisions.

For boards and executive teams preparing 2026 budgets: treat this preview as the strategic scaffolding. Use it to stress-test capex proposals, prioritize certifications and lock down critical suppliers. For access to the full dataset, interactive model and company benchmarking tables that underpin the projections in this brief, please consult our Composite Sandwich Panels Market report on PW Consulting’s research portal.

For detailed analysis of this topic, please visit the official page:Composite Sandwich Panels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com