Bone Cutting Forcep Market — Strategic Preview for 2026: How PW Consulting’s Latest Report Arms Decision‑Makers for the Next Growth Cycle

PW Consulting today releases an executive preview of our forthcoming Bone Cutting Forcep Market research, addressing an urgent need for clarity as stakeholders prepare strategic moves in 2026. Drawing on a comprehensive base period (2020–2025) and a detailed forecast to 2032, the report synthesizes market trajectory, competitive dynamics, regulatory pressure points, and actionable playbooks tailored for manufacturers, distributors, healthcare providers, and private equity investors.

Bone Cutting Forcep Market

High‑level market pulse: measured growth, clear opportunity

The bone cutting forcep market has demonstrated consistent expansion through the recent cycle. Our analysis positions the market at USD 285.5 Million in 2025, with a compounded annual growth rate (CAGR) of 5.85% across the 2026–2032 forecast window. Under the base forecast, the market reaches approximately USD 425.0 Million by 2032—an outcome driven by steady demand in core surgical specialties, incremental product premiumization, and the continuing replacement/upgrade cycle in advanced healthcare systems.

Bone Cutting Forcep Market

- Why this matters for 2026: a sub‑6% CAGR signals a market that rewards disciplined, targeted investments (product refinement, regulatory readiness, channel strengthening) over broad, capital‑intensive expansion.

- Market concentration: the CR3 is ~35% and the CR5 ~48.5%, indicating meaningful presence of established players while leaving space for boutique innovators and regional specialists.

What the report delivers: practical, deal‑ready intelligence

PW Consulting’s full report is explicitly designed to be operationally useful. Beyond baseline sizing and forecasting, it contains the following deliverables aimed at supporting 2026 decision cycles:

Bone Cutting Forcep Market

- Proprietary market model (2020–2032) with flexible scenario toggles—useful for sensitivity testing across pricing, sterilization cost pass‑throughs, and procedure volume shocks.

- Buyer and supplier heatmaps that identify pockets of premiumization, margin compression, and white‑space opportunities across materials, disposability trends, and service models.

- A regulatory compliance checklist and timeline (EU MDR, FDA pathways, ISO 13485 implications) tailored to reusable surgical instruments and relevant to new product submissions and refurbishment service launches.

- Commercial playbooks: GTM (go‑to‑market) recommendations for OEMs versus contract manufacturers, pricing guidance for tiered product families, and procurement negotiation levers for hospital systems.

- M&A and partnership scorecards identifying target profiles, likely valuation multiples, and integration risks for bolt‑on acquisitions in 2026 and beyond.

- Operational due diligence templates including sterilization cycle validation, lifecycle cost analyses, and refurbishment/repair economics for reusable forceps.

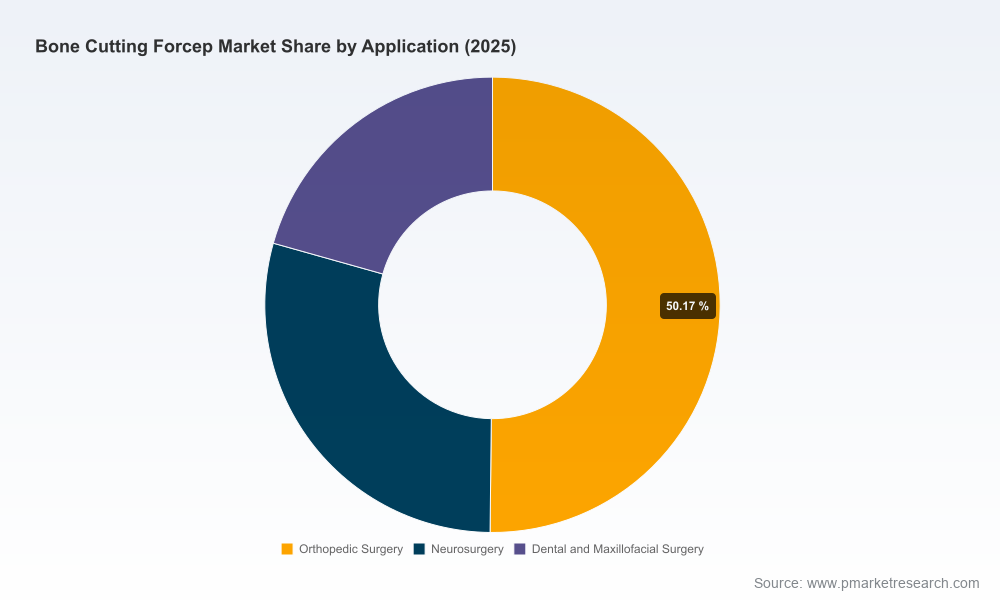

Note: consistent with the “trailer” approach, the full report contains granular segmentation tables and regional/application splits that are intentionally reserved for subscribers and purchasers; the preview highlights strategic implications without reproducing sensitive sub‑segment numbers here.

Regulatory and standards environment — a non‑negotiable gating factor

Regulation shapes both market access and competitive positioning. Bone cutting forceps are commonly regulated as reusable Class I or Class II medical devices under current EU and U.S. frameworks, which has several practical implications:

- Manufacturers must demonstrate sterilization compatibility and material durability under repeated autoclaving cycles, with surgical‑grade materials and validated processes.

- ISO 13485 remains the baseline quality management expectation for suppliers; CE marking and FDA clearances are common differentiators for cross‑border OEMs and distributors.

- Regulatory timelines can materially affect new product launches—planning for conformity assessments and associated clinical/technical file preparation should be frontloaded into 2026 plans.

Materials and design trends — premiumization with pragmatic constraints

Material selection is central to both product performance and total lifecycle cost. The market continues to revolve around established surgical‑grade stainless steels that provide corrosion resistance and service longevity, while premium alloys and coatings are gaining traction in niche, high‑value segments where durability and weight reduction matter.

- Design innovation is incremental rather than disruptive: ergonomics, modular screw joints for easier disassembly and sharpening, and surface treatments that extend service life are the dominant innovation vectors.

- For producers, balancing raw material cost volatility against the willingness of purchasers to pay a premium for extended tool life will be a defining margin lever.

Competitive landscape: established incumbents and strategic consolidation

The competitive map is characterized by a mix of specialized surgical instrument makers, broader medical device suppliers, and regional distributors. Notable profiles from our vendor analysis include:

- Stille AB (Torshälla, Sweden): a premium manufacturer known for high‑quality double‑action instruments with precision screw joints and design features facilitating disassembly and resharpening—an incumbent whose product and service quality command premium positioning.

- Integra LifeSciences (Miltex) (Princeton, NJ, USA): a broad surgical instruments portfolio with multiple established forcep patterns and scale distribution advantages across major markets.

- Surgical Holdings (Southend‑on‑Sea, UK): historical expertise in 420 stainless steel manufacturing with complementary repair and refurbishment services that add lifecycle value for customers.

- gSource (New Jersey, USA): a distributor/manufacturer specializing in high‑quality German stainless steel patterns, favored by orthopedic buyers seeking European tooling standards.

- GerMedUSA / GerVetUSA (Garden City Park, NY, USA): supplier breadth across human orthopedic and veterinary use cases, representing an adjacent growth angle through diversified end‑user segments.

Strategic note: the September 2025 acquisition of Surgical Holdings by Stille AB (announced publicly) is illustrative of the consolidation logic we expect to continue in 2026 — incumbent premium brands expanding service portfolios and back‑end capabilities to capture more of the instrument lifecycle value chain.

Strategic implications and recommended plays for 2026

We translate market dynamics into four priority strategic plays that organizations should consider in the 2026 planning cycle.

- For incumbent OEMs: prioritize service‑led differentiation. Investing in refurbishment capabilities, validated sterilization guidance, and bundled service contracts increases wallet share and defends unit margins against commoditization.

- For mid‑market manufacturers: pursue focused product premiumization in one or two clinical niches tied to high frequency procedures. This creates defensible specialty positions without requiring expansive capital outlays.

- For distributors and channel partners: align on inventory and repair ecosystems. Faster turnaround on refurbishment and localized sterilization validation can be a decisive procurement criterion for hospital systems under cost pressure.

- For investors: seek targets with documented regulatory compliance (ISO 13485, CE/FDA clearances), proven refurbishment economics, and a clear route to international market access—these attributes materially de‑risk post‑acquisition integration.

Scenario thinking: what could bend the base forecast?

Our scenario modules identify three vectors that could create upward or downward deviations from the 5.85% CAGR base case:

- Procedure volume shock (demand side): significant increases in elective orthopedic procedures or accelerated hospital procurement cycles would lift demand; conversely, slower procedural recovery or budget tightening could compress growth.

- Regulatory tightening (supply side): stricter reprocessing requirements or new conformity assessment expectations would raise time‑to‑market and compliance costs, favoring larger firms with regulatory depth.

- Material cost and supply disruptions: spikes in alloy prices or supply chain interruptions for precision components would pressure margins, benefitting firms with vertical integration or diversified sourcing strategies.

Why PW Consulting’s intelligence matters for 2026 decisions

Actionable market foresight is not just descriptive—it changes how companies allocate capital, staff, and time. Our report equips decision‑makers with the empirical basis to:

- Prioritize product investments that generate durable returns under modest top‑line growth;

- Structure M&A and partnership diligence around regulatory and refurbishment capabilities;

- Design procurement contracts and channel strategies that capture lifecycle economic value rather than one‑time sales;

- Forecast cash flow scenarios that incorporate potential regulatory and materials shocks.

Accessing the full intelligence

This executive preview outlines the strategic contours and practical levers for 2026. For readers requiring the segmented tables, full regional and application breakdowns, company scorecards, and the downloadable market model that underpins our forecasts, the complete report and supporting datasets are available on PW Consulting’s research portal. The granular segmentation and proprietary matrices are intentionally excluded from this preview to preserve subscriber value and to encourage direct engagement with our specialists for tailored data extracts.

To inquire about the full report, bespoke consulting engagements, or to schedule a briefing with PW Consulting’s orthopedics and surgical instruments practice, please visit our official research page.

For detailed analysis of this topic, please visit the official page:Bone Cutting Forcep Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com