GNSS Splitter Market: Competitive Landscape and Industry Forecast 2026-2034

Other |

2026-06-11 12:15:10

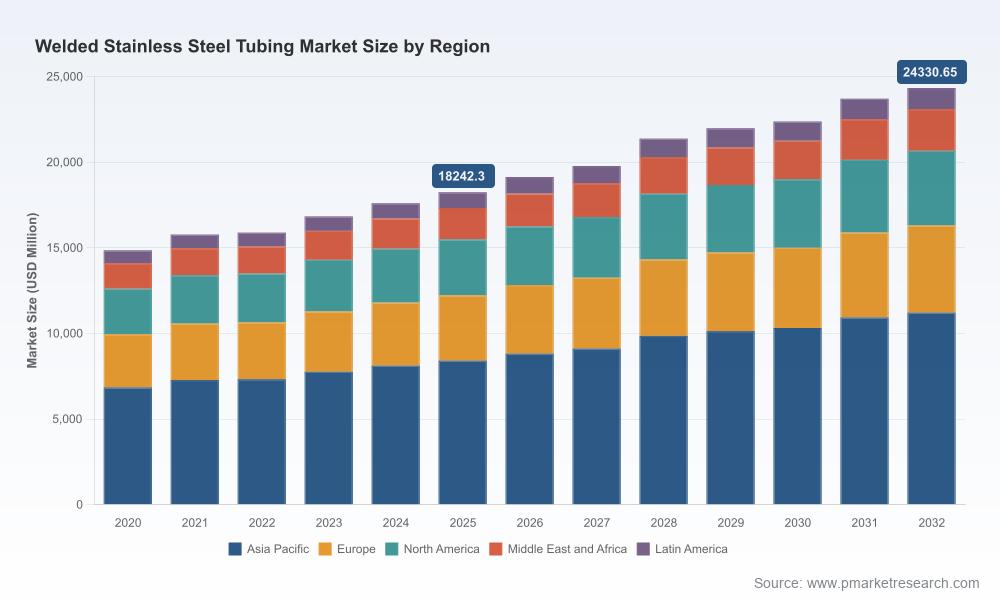

PW Consulting's latest market research on Welded Stainless Steel Tubing (base year 2025) frames a pragmatic growth narrative for 2026 planning cycles. The global market reached USD 18,242.3 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.2% through the 2026–2032 forecast window, approaching an estimated USD 24,330.7 Million by 2032. Grounded in a five‑year historical series (2020–2025) and built on scenario-based forecasting, this study is tailored to inform capital allocation, supply chain hedging, technology investment, and M&A decisions for senior executives entering FY2026.

Welded Stainless Steel Tubing Market

Intersection of structural demand and specialty performance: Welded stainless steel tubing sits at the nexus of traditional construction and emerging performance-driven applications — heat exchangers, energy infrastructure, and precision assemblies — creating parallel demand vectors that require distinct commercial and technical responses.

Welded Stainless Steel Tubing Market

Fragmented supplier landscape: Market concentration remains low (CR3 approximately 14.8%; CR5 approximately 22.15%), indicating a fragmented supply base with room for vertical integration, selective consolidation, and value capture through scale or specialization.

Welded Stainless Steel Tubing Market

Input volatility and margin pressure: Feedstock dynamics — notably nickel and chromium pricing volatility — continue to reverberate through producer margins and contractual terms, making procurement strategy and product-mix optimization high-priority topics for 2026.

This research is designed as a decision-support toolkit rather than a descriptive inventory. Key deliverables include:

Executive dashboard: concise topline market sizing, growth scenarios, and sensitivity analysis for commodity and demand shocks.

Commercial playbooks: go‑to‑market options for producers and distributors (e.g., premiumization vs. volume play, short‑lead JIT services, aftermarket and value‑added processing).

Supply chain and procurement playbook: stress‑tested hedging strategies, multi‑sourcing models, and raw‑material pass‑through clauses tailored to contractual horizons common in tubing applications.

Technology and product strategy: technology adoption roadmaps (including laser and laser‑hybrid welding), cost‑benefit matrices for process upgrades, and specification guidance tied to evolving standards.

Competitive intelligence & M&A playbook: 30+ company profiles, capability maps, valuation themes, and a shortlist of attractive archetypes for bolt‑on or platform transactions.

Regulatory and standards brief: implications of active specifications and recent standard updates for product certification and qualification timelines.

Several dynamics will shape corporate outcomes in 2026:

Technology-driven product differentiation. Laser and laser‑hybrid welding technologies deliver measurable performance gains — notably improved fatigue resistance — enabling welded tubes to displace alternative solutions in high‑cycle and thermal‑management environments. For companies that manufacture or procure tubing for emission control, thermal management in electrified systems, and advanced heat‑exchange designs, investing in, or partnering to access, laser‑weld capabilities is rapidly moving from optional to strategic.

Standards and certification as market access barriers. Recent and active standards provide both constraints and opportunities. ASTM specifications governing mechanical and structural welded tubing shape qualification lead times, acceptance criteria, and product claims. Firms that internalize certification timelines into product launches will shorten time‑to‑revenue and reduce qualification risk for strategic clients.

Raw material volatility demands proactive procurement. Historical swings in nickel and chromium prices have exceeded twenty percent over multi‑year windows, directly impacting bill‑of‑materials and contract margins. In 2026, procurement teams must assume elevated baseline volatility and bake in layered mitigation tactics: index‑linked pricing, longer‑term agreements with price collars, and selective forward purchasing tied to firm order books.

Fragmentation creates arbitrage opportunities. The low top‑tier concentration signals a market alive with regional specialists, custom manufacturers, and niche precision players. For strategic buyers, the opportunity set includes acquiring capability (precision, laser welding, specialty alloys), expanding geographical coverage, or consolidating distribution to capture margin uplift.

Our analysis benchmarks a set of established and specialist firms to illustrate strategic archetypes and tactical moves observed in the market:

Plymouth Tube Company (Warrenville, IL): A precision‑focused producer that emphasizes high‑performance grades and close tolerances for aerospace, heat‑exchange, and instrumentation markets. Competitive advantage rests on certification breadth and supply reliability for mission‑critical applications.

Tubacex (Llodio, Spain): A global high‑performance alloy specialist with depth in nickel and titanium alloys for oil & gas and power generation. Tubacex exemplifies the scale‑plus‑specialty model where alloy expertise underwrites premium pricing.

Marcegaglia Steel (Mantova, Italy): A European leader in welded tubing and pipes with a broad industrial portfolio; its scale and distribution network make it a go‑to for industrial and sanitary segments.

ArcelorMittal (Luxembourg): Represents the integrated steel‑maker archetype — broad product reach, cost discipline, and the ability to supply large infrastructure accounts where single‑supplier scale matters.

Nippon Steel Corporation (Tokyo): Integrated automotive and infrastructure exposure, where tight engineering collaboration and qualification cycles support long‑term contracts.

Sandvik / Alleima (Sandviken, Sweden): Specializes in precision and specialty tubing for demanding sectors (medical, energy), where material science and processing precision are differentiators.

KVA Stainless (California) & Indiana Tube (Indiana): Examples of US‑based custom and price‑competitive welded producers; they compete on customization, speed, and value for applications where seamless tubes are not a strict requirement.

Bristol Metals (Brismet) & Stainless Structurals: Bristol represents high‑volume, continuous‑mill capacity; Stainless Structurals is an exemplar of laser‑weld specialization and fast qualification for structural profiles — both illustrate divergent routes to market in North America.

Fischer Group & YC Inox: Regional manufacturers with focused export strategies that serve industrial and precision niches in EMEA and Asia.

Standards and market visibility: Stainless Structurals has actively positioned itself under a recent ASTM structural tubing standard and demonstrated product use cases at major industry conferences — a clear example of standards‑driven commercial positioning accelerating adoption in structural and data center markets.

Application demand shifts: Market participants have highlighted a step‑up in heat‑exchanger demand as a meaningful driver of tubing consumption, underlining the need for suppliers to align product portfolios and capacity plans with thermal‑management growth pockets.

Technology adoption: Consistent industry commentary points to laser welding’s role in improving fatigue performance and enabling design consolidation, supporting selective capital and partnership decisions in 2026.

Procurement: Adopt a layered hedging strategy for alloy exposure, standardize contractual language to allow price pass‑through where feasible, and expand approved‑vendor lists to reduce single‑source risk.

Operations and CapEx: Prioritize investments in laser/laser‑hybrid welding where product roadmaps require fatigue improvement or geometry complexity; where volume stability is uncertain, prefer modular upgrades and contract manufacturing partnerships.

Commercial: Differentiate via certification speed, custom value‑added services (cutting, finishing, just‑in‑time logistics), and application engineering support — these are effective margin levers in a fragmented market.

M&A and corporate development: Target acquisitions that add specialty alloys, laser‑weld capability, or customer relationships in high‑growth end markets. Given low top‑tier concentration, bolt‑ons can yield rapid share and margin gains if integration captures operational synergies.

R&D and product strategy: Translate standards and evolving specifications into product roadmaps; pre‑qualify products against common buyer specifications to shorten sales cycles and reduce qualification attrition.

Our deliverables are structured for immediate use in boardroom and executive planning sessions. The report blends quantitative forecasting (topline sizing and scenario work based on historical 2020–2025 trends) with qualitative playbooks that map directly to C‑suite levers: procurement, operations, sales, and M&A. Critically, while this preview highlights the macro outlook and strategic pathways, the full report contains the granular segmentation, regional trajectories, application‑level demand curves, and supplier scorecards required to operationalize decisions — material we intentionally withhold here to preserve the report’s role as an actionable, proprietary planning asset.

Executives preparing budgets, capital plans, or acquisition pipelines for 2026 should use the market’s projected mid‑single‑digit growth profile (CAGR 4.2% across 2026–2032) as the baseline scenario and overlay company‑specific assumptions for price and product mix. For immediate support, PW Consulting offers tailored workshops that translate the report’s insights into company‑level strategies: supplier rationalization, CapEx prioritization, and go‑to‑market segmentation aligned to end‑market dynamics.

To access the full Welded Stainless Steel Tubing Market report, including detailed segmentation tables, supplier scorecards, and downloadable financial models, please consult PW Consulting’s market research portal.

For detailed analysis of this topic, please visit the official page:Welded Stainless Steel Tubing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com