PBN Heaters Market Expands with Rising Demand for Ultra-High-Purity Heating Solutions

Food |

2026-06-09 09:31:56

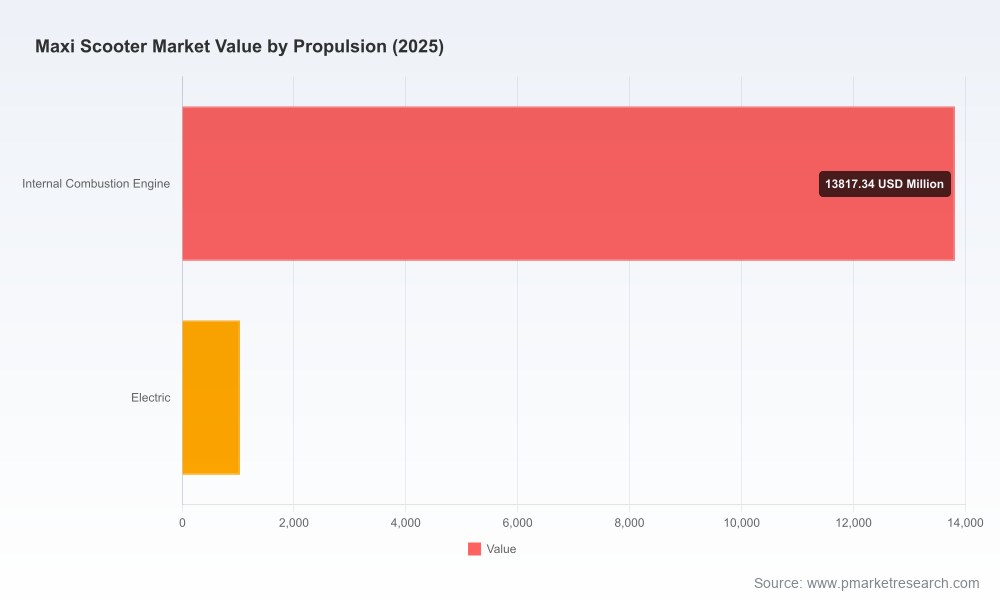

PW Consulting’s latest Maxi Scooter Market report—anchored on a 2025 base year and projecting through 2032—translates market dynamics into boardroom-ready intelligence for 2026 decision cycles. The market has progressed from a mid‑teens billion USD scale in 2020 to an estimated USD 14.85 billion (2025 base), and our forecast sees continued expansion toward roughly USD 22.51 billion by 2032, reflecting a compound annual growth rate (CAGR) of 6.12% across the 2026–2032 horizon. This release is designed as a strategic “trailer”: it demonstrates analytical depth and prescriptive guidance while preserving core proprietary segment datasets—available in full through our distribution channel.

Maxi Scooter Market

Timing alignment: 2026 is a pivot year for many OEMs and suppliers as product cycles, electrification commitments, and regulatory windows converge. Our report synthesizes historical momentum (2020–2025) with forward-looking scenarios to inform near-term capital and portfolio choices.

Maxi Scooter Market

Resource prioritization: With a measured but steady CAGR, incumbents and new entrants must optimize R&D, manufacturing capacity, and channel investments. The report quantifies trade-offs between investing in combustion refinement, hybrid bridging strategies, and full electrification pathways.

Maxi Scooter Market

Risk calibration: Regulatory complexity and component-level engineering constraints create uneven risk across product architectures and markets. We map these risks to specific product attributes—enabling CFOs and product chiefs to stress-test investment cases.

Our market model traces a clear recovery and maturation arc: robust historical expansion through 2020–2025 gives way to steady growth in the forecast period. For a manufacturer or supplier, the numbers imply three practical implications for 2026 planning: prioritize mid-cycle refreshes and flagship launches to capture premium buyers; secure modular supply chains to respond to fluctuating material and electronics demand; and implement nimble pricing and financing programs that improve conversion in premium and touring segments.

The market concentration profile is instructive: the top three players account for a meaningful share of global revenue, while a top five concentration indicates a moderately consolidated competitive environment. This dynamic favors focused investments in brand differentiation, dealer economics, and aftersales services for companies targeting market share expansion.

Urban-to-tour duality: Demand patterns split between urban commuters seeking stability and storage and premium buyers prioritizing comfort and range for long-distance touring. Product roadmaps that balance these needs will capture incremental volume without sacrificing margin.

Electrification momentum (policy and market): Stringent low-emission zones and tightening emissions controls across multiple markets accelerate interest in electric variants. At the same time, customer expectations for range, charging convenience, and premium features are rising—creating a two-track market for near-term electrified offerings and longer-term EV mainstreaming.

Regulatory tech baseline: Safety and emissions requirements—such as mandatory ABS on motorcycles above certain displacements and pollutant thresholds that drive higher-pressure fuel systems—raise the technical baseline for all new models. These mandates increase engineering complexity, weight, and parts content, which must be reflected in cost modeling and warranty provisioning.

Two engineering notes in particular shape 2026 sourcing and design choices. First, advanced suspension and stability systems—required to deliver premium ride quality across urban and touring use cases—introduce additional part complexity and weight. Second, conventional ICE maxi-scooters increasingly require higher-spec fuel-injection systems and emission-control calibrations to meet pollutant limits, while EV variants shift material demand toward batteries, power electronics, and thermal management subsystems. Our report provides supplier tier mapping, cost-to-serve estimates by architecture, and breakpoints for in‑house versus outsourced production decisions.

The competitive field remains anchored by traditional OEMs and a rising set of global and regional challengers. Leaders differentiate on product engineering, experience features, and distribution reach; nimble players compete on price-to-feature ratio and regional focus. Highlights from our corporate review include:

Piaggio Group (Pontedera, Italy) — strength in premium three-wheel and touring maxi scooters with established models focused on stability and storage; their product philosophy underscores a premium-experience route to grow share among affluent urban and touring buyers.

Honda Motor Co. (Tokyo, Japan) — leverages engine refinement, transmission options such as DCT, and a clear push into adventure/touring niches; recent announcements indicate targeted market introductions aligned with global premiumization.

Yamaha Motor Co. (Iwata, Japan) — maintains sport-maxi leadership through the TMAX lineage, prioritizing performance and rider engagement as a way to defend high-margin segments.

BMW Motorrad (Munich, Germany) — blends premium comfort and electronics with both combustion and electric offerings, targeting urban-to-touring riders who prioritize technology and brand prestige.

Kymco (Kaohsiung, Taiwan) — positions itself strongly in long-distance touring maxi scooters and is increasingly visible in strategic partnerships for electrification.

Suzuki, SYM, Peugeot, Italjet, Zontes, and emerging electric entrants (including LiveWire) — each pursues differentiated playbooks from value-driven offerings through high-performance and stylistic niche plays to electrified premium launches.

Recent strategic moves underscore shifting competition: partnership announcements and cross-licensing accelerate EV platform readiness; targeted market launches expand presence in North America and South Asia; and anniversary or halo model updates re‑energize brand narratives. PW Consulting’s competitive chapter distills these developments into implications for share gains, margin compression risk, and partnership strategies.

Executive dashboard: Line-of-sight metrics, scenario toggles, and a 2026 decision checklist for CEOs and CFOs.

Demand model: Market-size and demand-by-use-case engine with sensitivity levers for fuel price, incentive regimes, and urban policy shocks (note: detailed segment tables are reserved for the full report).

Competitive playbooks: Strengths/weakness matrices for 12+ OEMs, launch calendars, and go-to-market recommendations tailored to premium, mass, and electric sub-segments.

Technology and supplier mapping: Tier‑1 and specialty supplier lists; cost and lead-time benchmarks for powertrains, suspension systems, ABS and electronics; EV battery supply scenarios.

Regulatory risk matrix: Jurisdiction-level triggers, compliance timelines, and cost-to-compliance estimates for 2026–2028 decision windows.

Deal and partnership screening: Acquisition targets, potential JV partners, and a prioritized shortlist for strategic alliances—scored by strategic fit and execution complexity.

Dealer economics and aftersales playbook: Profitability models, service network expansion plans, and subscription/finance product frameworks to enhance lifetime value.

Adopt a platform mindset: Invest in modular architectures that allow quick shifts between combustion, hybrid, and electric variants to protect investment across regulatory scenarios.

Prioritize segment-defining features: Stability systems, storage solutions, rider connectivity, and comfort enhancements are decisive for premium buyers; allocate R&D accordingly.

Secure critical suppliers: Lock multi-year agreements for ABS modules, advanced suspensions, and battery cell supply where applicable; small weight increases and added modules materially affect cost and performance.

Pursue selective partnerships: Collaborations—particularly in EV platforms and electronics—are lower-cost routes to market entry and capability acceleration, as evidenced by recent industry alliances.

Design dealer economics for retention: Strengthen service, financing, and digital sales capabilities to convert higher ASPs into sustainable margins across the product lifecycle.

This briefing intentionally highlights analytical conclusions, strategic implications, and the modular tools that senior teams need in 2026, while preserving the granular segment matrices and proprietary forecasts that underpin our recommendations. For detailed segmentation tables, market-share matrices, regional demand curves, and the full set of scenario outputs—plus tailored briefings for executive teams—visit the PW Consulting Maxi Scooter Market report page or contact our industry desk for an authorized extract.

For detailed analysis of this topic, please visit the official page:Maxi Scooter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com