Europe Mezcal Market Dynamics: Key Drivers and Restraints

Other |

2026-05-12 07:25:48

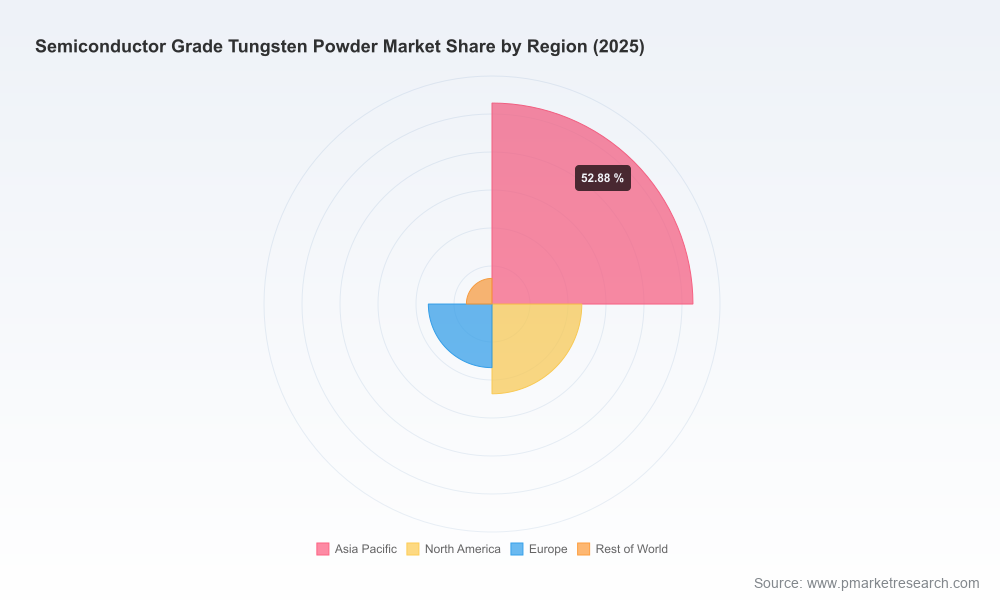

PW Consulting's latest market study on semiconductor grade tungsten powder frames an urgent strategic moment for semiconductor manufacturers, materials suppliers, and downstream equipment makers. Anchored on a 2025 base year and a detailed 2026–2032 forecast horizon, the report demonstrates that the market is moving from a commodity rhythm into a strategic materials regime: after growing from the mid‑hundreds of millions in 2020 to an estimated USD 565.0 Million in 2025, the market is projected to accelerate—reaching roughly USD 635.6 Million in 2026 and expanding at a compound annual growth rate (CAGR) of approximately 9.15% through 2032, when the market crosses the USD 1.04 Billion threshold.

Semiconductor Grade Tungsten Powder Market

Tungsten powder is no longer a back‑office procurement item. The combined effect of surging semiconductor demand, upstream feedstock constraints, and export regulatory interventions has converted tungsten into a strategic material with direct implications for wafer fab uptime, qualification schedules, and BOM pricing. Our analysis shows that a relatively modest supply‑side disruption can produce outsized effects on availability and lead times; 2025–early 2026 events have already provided a live stress test of supplier resilience and buyer preparedness.

Semiconductor Grade Tungsten Powder Market

Supply dislocation and regulatory shocks: China’s export controls on upstream tungsten intermediates announced in early 2025 substantially tightened global flows of ammonium paratungstate (APT) and related intermediates. Market intelligence indicates APT prices spiked—at times rising multiple‑hundreds of percent in volatile pockets of 2025–2026—feeding through to semiconductor‑grade tungsten powder prices and exacerbating lead time risk for qualified materials.

Semiconductor Grade Tungsten Powder Market

Price volatility and procurement exposure: Industry commentary and association data in 2026 noted multi‑fold price increases for certain semiconductor‑grade tungsten products. For buyer organizations this translates into non‑trivial cost exposure across component lifecycles, particularly for products with long qualification cycles and fixed pricing arrangements.

Structural concentration: The market exhibits concentration among a handful of established producers that combine legacy powder metallurgy know‑how with downstream qualification capabilities. Our proprietary concentration analysis indicates that top producers together hold a substantial share of the addressable market—underscoring both the gateway role of qualified suppliers and the negotiation power they wield in times of constrained supply.

Operational resilience via recycling and verticalization: Leading producers are investing materially in recycling and closed‑loop programs. Public and company disclosures point to recycling rates exceeding 60% in some operations, which meaningfully insulate supply chains from upstream feedstock shocks when combined with diversified feedstock strategies.

Our competitive review profiles established Western suppliers alongside major Asian producers. Incumbents that combine production assets, materials science capability, and semiconductor industry qualification experience are extending their value propositions in three ways: (1) enhanced purity and process control to meet advanced CVD/ALD and sputtering requirements; (2) supplier qualification partnerships with strategic buyers to shorten time‑to‑adoption; and (3) investments in recycling and feedstock integration to reduce exposure to upstream raw material disruption.

Illustrative moves include new product lines tailored for semiconductor use, operational reports showcasing elevated recycling and impurity control, and supplier statements quantifying increased product demand and pricing pressure. For prospective partners and investors, these signals point to where the industry is concentrating R&D and capex.

Procurement strategy: Move from spot buying to longer‑term, multi‑tiered agreements that explicitly account for qualification timelines, price escalation mechanics, and allocation rules in the event of supply shocks. Contracts should incorporate tiered pricing tied to feedstock cost indices, and options for volume flexibility to manage fab ramp risk.

Qualification and design flexibility: Accelerate materials qualification pipelines and invest in parallel path qualifications (multiple suppliers and grades). Where possible, standardize on families of tungsten chemistries and particle morphologies that are amenable to multi‑supplier sourcing without re‑engineering process windows.

Inventory and dual‑sourcing playbooks: Recalibrate safety stock policies for critical tungsten‑dependent components and codify dual‑sourcing protocols that include technical readiness reviews and periodic cross‑qualification exercises to validate swap‑in performance.

Engineering collaboration: Co‑fund downstream qualification labs and joint test programs with suppliers to accelerate acceptance of recycled and alternative feedstock‑derived powders while preserving process yields and device reliability.

Capex and geographic strategy: Prioritize modular capacity expansions near strategic demand clusters to shorten lead times and mitigate export control exposure. Consider near‑shoring or regional partnerships where regulatory or logistics risks are concentrated.

Product differentiation through purity and particle morphology: R&D efforts that lower impurity footprints, reduce metallic contaminants, and control particle size distribution will command premium pricing and stronger qualification defensibility.

Closed‑loop recycling and feedstock integration: Integrate recycled tungsten streams formally into commercial product offerings, combined with process guarantees and traceability, to assuage OEM concerns about consistency while capturing margin uplift from circularity.

M&A and partnership plays: Market concentration and demand growth create attractive opportunities for strategic acquisitions—particularly of specialty powder producers, purification technology providers, and recycling specialists that accelerate end‑to‑end qualification timelines.

Regulatory tail risk: Export controls and licensing regimes can emerge with limited notice; contingency scenarios and alternative feedstock mapping should be part of board‑level risk registers.

Price shock and pass‑through timing: Sudden jumps in upstream APT or oxide prices can outpace contract renegotiation windows. Hedging strategies and indexed pricing clauses are tactical levers to dampen earnings volatility.

Qualification lag: Even when supply alternatives exist, long qualification cycles can lock fabs into incumbent suppliers during shortage events. Proactive parallel qualification programs are a direct mitigation.

Concentration of specialty capability: A limited number of producers retain deep know‑how in ultra‑high purity production and particle engineering, making intellectual capital a strategic choke point in tight markets.

Forward‑looking economic model: A transparent market model with a 2020–2025 historical foundation and a 2026–2032 forecast that produces annualized market projections, scenario variants, and sensitivity analyses tied to feedstock price paths.

Supplier scorecards and readiness assessments: Qualitative and quantitative evaluations of leading producers across capability, capacity, geographic resilience, and qualification depth. These scorecards are designed for buyer short‑lists and supplier development roadmaps.

Procurement playbooks: Contract design templates, inventory heuristics, and negotiation frameworks tailored to tungsten markets and semiconductor qualification constraints.

Technology and materials guidance: Practical recommendations for materials engineers on acceptable tolerance bands, impurity management approaches, and accelerated qualification protocols for recycled and alternative feedstock powders.

Strategic scenarios and decision trees: Three core future states—moderate normalization, prolonged constrained supply, and structural re‑regionalization—each mapped to operational and corporate actions across CAPEX, sourcing, and R&D.

Selected industry events in the past two years underline the shift. Several established Western suppliers have launched semiconductor‑specific powder lines and publicly documented investments in product and process control. Industry associations and market sources reported multi‑fold price increases for tungsten inputs following tightened Chinese export policy. And leading producers are publishing higher recycling rates—concrete evidence that circularity is evolving from pilot programs into a core resilience strategy.

Immediate (0–6 months): Audit supplier exposure, validate critical‑path qualifications, and implement liquidity and contract clauses that cover extreme feedstock price moves.

Near‑term (6–18 months): Initiate parallel supplier qualifications, invest in supplier co‑testing, and negotiate multi‑year agreements with built‑in flexibility for volume ramps and price pass‑through.

Strategic (18–36 months): Pursue vertical integration or strategic equity stakes in specialized powder producers or recycling specialists where alignment to core roadmaps and fabs’ long‑term demand makes sense.

For C‑suite leaders, the report provides the market context and strategic playbook necessary to convert a materials risk into a competitive advantage. For procurement and materials engineering teams, it supplies concrete tools—scorecards, contract templates, and qualification roadmaps—that reduce time‑to‑decision. For investors and strategic development teams, it identifies attractive zones for capex and corporate development activity, without exposing the granular market splits we intentionally reserve for full subscribers.

PW Consulting’s Semiconductor Grade Tungsten Powder Market report combines proprietary market modeling, primary interviews with producers and fabs, plant‑level supply chain mapping, and a playbook of practical actions for 2026. To access the full dataset, supplier scorecards, and the scenario modeling workbook that underpins the strategic recommendations summarized here, please visit our Semiconductor Materials research page or contact PW Consulting for a briefing.

For detailed analysis of this topic, please visit the official page:Semiconductor Grade Tungsten Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com