BYOD and Enterprise Mobility Market Size, Share, Diagnostics Trends, and Forecast by 2032

Other |

2026-06-29 09:59:11

As corporations recalibrate sustainability roadmaps and procurement strategies for the post‑pandemic green transition, renewable silica is emerging as a strategic raw material with both commercial upside and supply‑chain complexity. PW Consulting’s latest Renewable Silica Market report (base year 2025; historical period 2020–2025; forecast 2026–2032) synthesizes quantitative forecasts with forward‑looking playbooks to help executives convert market momentum into defensible advantage. Our headline projection: the global renewable silica market is accelerating on a double‑digit trajectory with an 18.01% compound annual growth rate through the 2026–2032 forecast window — a dynamic that transforms sourcing, technology, and product strategy across tires, rubber, personal care, coatings, and specialty industrial segments.

Renewable Silica Market

From pilot lines to commercial capacity — 2025 closed with several tier‑one producers moving from demonstration to industrial‑scale operations. That momentum converges with anticipated capacity ramps in 2026, making this year the first where buyers and investors must act on medium‑term supply visibility rather than experimental outcomes.

Renewable Silica Market

Regulation and voluntary sustainability standards are sharpening procurement criteria. Claims of lower carbon intensity are now auditable inputs to supplier selection and product specs, not marketing embellishments. Companies that wait will face both price and reputational risk.

Renewable Silica Market

Feedstock economics and variability — notably rice husk ash and other agricultural by‑products — will determine operational feasibility. Securing high‑quality, consistent upstream inputs becomes as strategically important as product formulation.

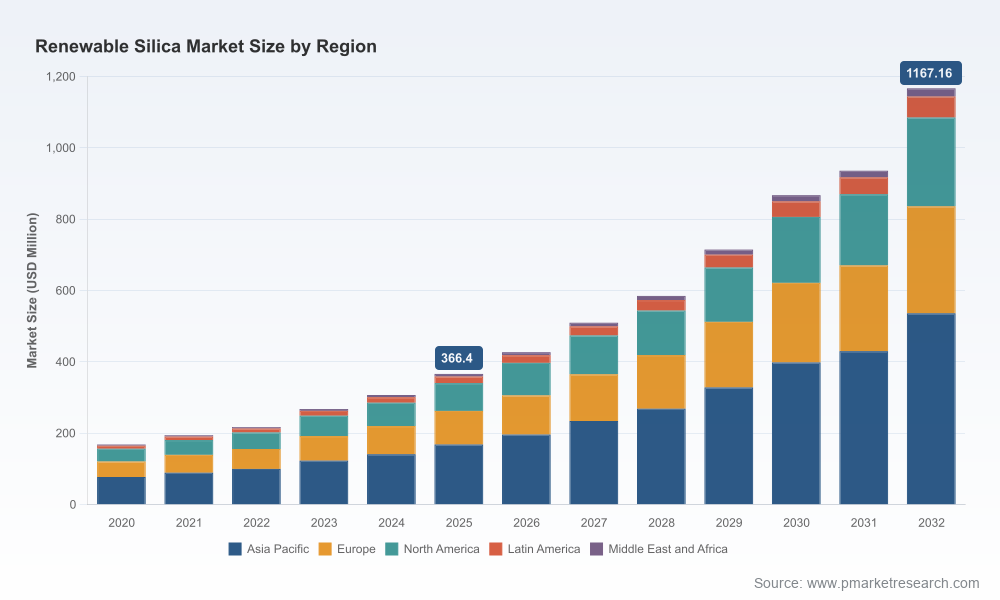

PW Consulting’s model reconciles historical shipments and capacity announcements to yield a near‑term market value of approximately USD 366.4 Million in 2025, rising to an estimated USD 427.3 Million in 2026 and accelerating to a multi‑hundred‑million market by the early 2030s. By 2032 our forecasted market size exceeds USD 1.16 Billion. This progression is driven by compound effects: rising adoption in green tire formulations, expanding specialty applications in personal care and food contact grades, and successive rounds of capacity expansion by incumbent chemical producers and specialized biobased players.

These top‑line figures matter for three categories of decision‑makers: (1) procurement leads who must secure feedstock and allocate offtake commitments; (2) R&D and product teams calibrating blend ratios and lifecycle claims; and (3) investors and corporate development teams sizing opportunities for M&A, joint ventures, and brownfield expansion. Each cohort faces a time‑sensitive window in 2026 to lock favorable economics and strategic options before capacity and contractual terms reset.

PW Consulting’s Renewable Silica Market report is organized to bridge analysis and execution. Key practitioner resources include:

Investment‑grade market model — month‑by‑month capacity build, utilization scenarios, and downside/upside supply curves for 2026–2032 (interactive files included with enterprise licenses).

Feedstock sourcing playbook — procurement pathways for rice husk ash and alternative biomass, supplier scorecards (quality, variability, logistics risk), and contract templates for security of supply.

Carbon and lifecycle assessment module — scenario comparisons of conventional vs. bio‑circular processes, abatement cost curves, and guidance on third‑party verification to support ISCC+/equivalent claims.

Go‑to‑market templates for chemical producers and converters — product positioning, pricing architecture, and channel strategies that align with OEM decarbonization requirements.

M&A and partnership screening — candidate lists, value levers, and integration checklists keyed to three strategic plays: vertical integration (feedstock ownership), capacity aggregation (regional consolidation), and specialty differentiation (high‑purity grades).

The market is neither atomized nor monopolistic. Our concentration analysis indicates a moderate leading group with top three players holding a material share of industry volumes and top five firms capturing a significant majority of established capacity. That concentration underpins a paired dynamic: incumbents can accelerate commercialization through capital deployment, while nimble regional entrants and specialized producers can exploit feedstock proximity and sustainability credentials to win business.

Notable strategic moves observed in our research include:

Solvay S.A. (Brussels) has introduced a bio‑circular highly dispersible silica produced from rice husk ash at its Livorno site and is expanding circular initiatives globally, including announced programs in Asia with ISCC+ certified inputs. Solvay’s roadmap emphasizes certified supply chains and measurable CO₂ reductions per ton — positioning legacy specialty chemical capabilities behind a circular narrative.

Evonik Industries AG (Essen) continues to invest in precipitated and sustainable silica capacity, with targeted expansions to serve the green tire market. Their approach combines scale‑oriented capacity expansion with partnerships to localize feedstock processing for industrial applications.

Regional and purpose‑built operators such as Blue Ocean Biotech in India and several Southeast Asian producers are commercializing rice husk‑based precipitated silica at commercial scale. These players leverage feedstock proximity and lower energy intensities to offer competitive sustainable grades.

A cohort of specialist firms across Asia and Latin America are focusing on niche, high‑value segments (food and healthcare grades, specialty coatings). Their agility on product development allows rapid qualification for sensitive applications.

Together these actors create a multi‑track competitive environment: integrated multinationals pursue certification, scale, and breadth; regional specialists pursue feedstock arbitrage and rapid product qualification; and technology startups focus on process innovation and niche differentiation.

Feedstock variability: Rice husk ash quality exhibits compositional variability that complicates continuous industrial production. The practical mitigation is layered: (a) upstream quality assurance and blended sourcing, (b) investment in preprocessing standardization, and (c) contractual quality bands with flexible price/volume clauses.

Certification as a commercial lever: ISCC+ and similar credible verification frameworks matter — not only for sustainability claims but also for premium offtake relationships with OEMs and brand owners. Firms should budget both CAPEX for cleaner processes and OPEX for ongoing compliance and auditing.

Capital intensity vs. incremental margin: While early adopters report attractive margin profiles for specialized renewable silica grades, the shift from niche to mainstream is capital intensive. Greenfield investments must be evaluated against partnership and tolling models that reduce payback periods.

Regulatory and reputational risk: Public sustainability claims are increasingly scrutinized. Companies must ensure lifecycle transparency and avoid overclaiming substitution benefits without end‑to‑end verification.

Our report examines vertical use cases that will matter for procurement and innovation teams in 2026. Tire and high‑performance rubber formulations are already the largest demand vectors for renewable silica; however, the second wave of growth is likely to come from higher‑margin personal care and food‑grade applications where the intersection of sustainability and regulatory approval creates opportunities for differentiated pricing. For each use case, we map qualification timelines, testing protocols, and the commercial implications of switching raw materials.

Procurement: prioritize mixed sourcing strategies combining long‑term offtake with short‑term spot access to manage feedstock and price volatility.

R&D: allocate parallel development paths — one focused on near‑term cost parity, another on premium sustainability attributes that can justify higher margins.

Corporate Development: use our M&A screening matrix to identify assets that unlock three levers — feedstock security, regional aggregation, and product differentiation.

Risk & Compliance: adopt lifecycle accounting frameworks recommended in the report to validate supplier claims and to de‑risk procurement choices.

This release is intentionally selective. To preserve the commercial value of our market intelligence and to drive decision makers to the full analytical toolkit, we are withholding proprietary segmentation tables, detailed regional share breakdowns, and application‑level price modeling from this summary. Those data sets are included in the full report and in the interactive model that accompanies enterprise licenses. If you are evaluating supply agreements, tender strategies, or investment options for 2026, that granular intelligence is the difference between an informed bet and an avoidable misstep.

Download the executive summary and request a briefing to see the interactive supply/demand model.

Schedule a tailored workshop where our team will map your portfolio against the report’s scenarios and produce a 90‑day action plan for procurement, R&D, or M&A.

Engage with our carbon‑abatement module to quantify CO₂ reductions by substitution strategy and evaluate the economics of certification.

In an industry transitioning from pilots to commercial reality, 2026 is when strategy turns operational. PW Consulting’s Renewable Silica Market report provides the quantified forecasts, supplier intelligence, and executable playbooks leaders need to make those operational choices with conviction. For the full data tables, regional and application segmentation, and access to our interactive forecasting model, please visit the report page or contact our industry practice team for a private briefing.

For detailed analysis of this topic, please visit the official page:Renewable Silica Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com