Payroll Outsourcing Market Size 2026 | CAGR Analysis: Transforming Global Payroll Solutions

Other |

2026-02-03 10:13:37

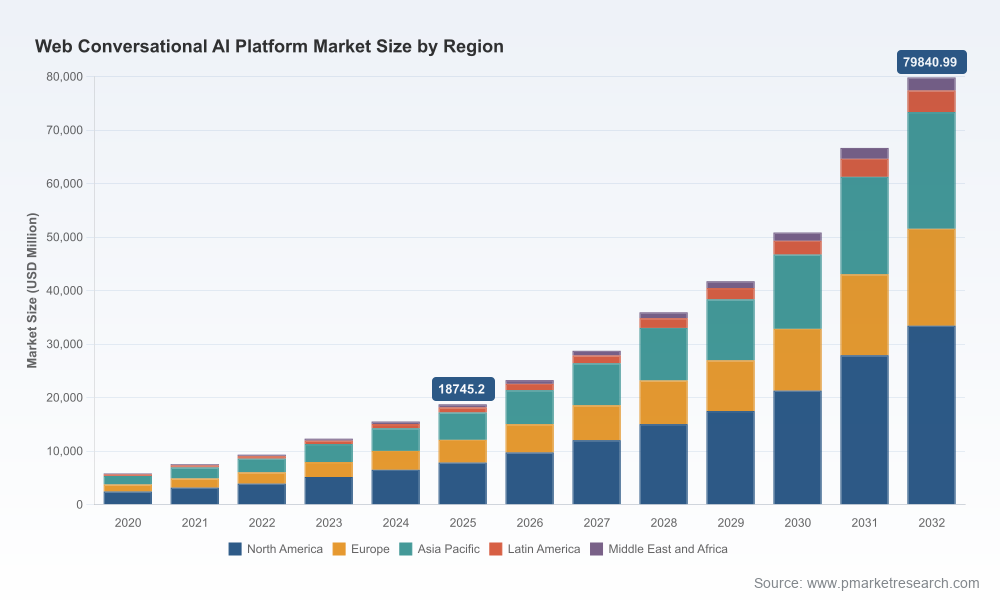

PW Consulting’s latest market research brief on the Web Conversational AI Platform market synthesizes five years of historical evidence and a seven-year forecast horizon to deliver an actionable strategic roadmap for enterprise technology and CX leaders. Anchored on a rigorous base year of 2025 and a detailed historical window (2020–2025), our analysis shows the market expanding at a near-23% compound annual growth rate through the forecast period (2026–2032). This growth trajectory underscores both the acceleration of AI-enabled customer and employee experiences on the web and the attendant strategic choices that will define competitive advantage in 2026.

Web Conversational Ai Platform Market

Timing: The market is transitioning from pilot-heavy adoption to scaled production deployments. Organizations planning procurement cycles in 2026 will be sourcing technology in a landscape dominated by platform extensibility, agentic capabilities, and cloud economics—factors that materially affect TCO and time-to-value.

Web Conversational Ai Platform Market

Commercial leverage: Higher growth rates create a seller’s market for differentiated capabilities (LLMs, action models, low-code orchestration). Buyers who align product roadmaps with near-term vendor roadmaps can capture outsized ROI; conversely, lagging procurement risks vendor lock-in and migration costs.

Web Conversational Ai Platform Market

Risk and regulation: Energy, data sovereignty, and cross-border data rules are increasingly material to platform selection. These operational factors must be baked into commercial negotiations and deployment architectures in 2026.

The report is designed as a playbook for technology executives, procurement leads, and CX heads. It combines market sizing and growth modeling with deep operational guidance, including:

Market sizing and forecast model (2020–2032) showing adoption inflection points and scenario analyses under alternative macro assumptions.

Vendor evaluation framework: technical, commercial, and operational scorecards to objectively assess platforms against enterprise requirements (integration, compliance, orchestration, observability, and cost predictability).

Deployment blueprints: cloud, hybrid, and on-premise reference architectures aligned to latency, data residency, and security constraints.

TCO and ROI templates: interactive levers addressing licensing, cloud compute and energy costs, maintenance, and labor offsets from automation.

Procurement assets: RFP language, contract clauses for sustainability and data residency, SLAs for LLM performance, and vendor transition checklists.

Sector playbooks: outcome-focused use cases and KPIs for mission-critical verticals, and workforce transformation roadmaps for contact centers and digital service teams.

Change-management and governance guide: recommended organizational structures, vendor governance forums, and compliance guardrails for 2026 deployments.

The market is shaped by hyperscalers, legacy enterprise software firms, specialized conversational AI vendors, and an emerging set of startups focused on agentic or outcome-driven experiences. Our vendor analysis profiles leaders and challengers across technical depth, enterprise readiness, ecosystem reach, and innovation cadence.

Google (Dialogflow CX): Strong in building multi-turn, web-native agents with deep integration into Google Cloud infrastructure—well-suited for enterprises that prioritize scale and ecosystem consolidation.

Microsoft (Copilot Studio / Azure Bot Service): Leverages broad Microsoft stack integration (Azure, Teams, Office) to offer conversational capabilities that are often compelling for enterprises seeking unified employee and customer experiences.

Amazon (Lex): Provides scalable web and voice agent capabilities tightly integrated with AWS services—appealing where cloud-native compute elasticity and pay-as-you-go economics are priorities.

IBM (watsonx Assistant): Focuses on no-code/low-code building, LLM integration, and business process automation—attractive to regulated industries that require enterprise-grade governance and lifecycle management.

Specialized players (Kore.ai, Cognigy/NICE, Yellow.ai, LivePerson, Sprinklr, OneReach.ai): These vendors frequently win on verticalized templates, omnichannel orchestration, and faster time-to-production for industry-specific workflows.

Outcome- and developer-focused entrants (Rasa, Sierra, Decagon, Intercom/Fin): Span the open-source to high-growth startup spectrum, enabling tailored experiences where custom NLU, agent memory, or outcome-based commercial models are required.

In 2026, vendor differentiation will be less about raw NLU capabilities and more about composability (how well a platform integrates LLMs and action models), operational observability, and the commercial terms that reflect compute and energy cost exposure.

Large suppliers and platforms are embedding agentic capabilities—products that can act (execute tasks) as well as converse—creating new opportunities for automation and new vendor lock-in dynamics.

Strategic partnerships between retailers and cloud providers demonstrate the push to integrate conversational agents into end-user journeys at scale, reinforcing the importance of data integration and UX design.

Consolidation and funding events show both investor confidence and the acceleration of enterprise adoption: acquisitions that bring workforce optimization together with conversational capabilities, and significant funding rounds for outcome-focused startups.

Three operational vectors are material for procurement and architecture choices in 2026:

Energy and infrastructure costs: Data center energy demand and associated cost exposure are rising. Expect cloud providers and platform vendors to pass through or reprice compute-heavy workloads; sustainability SLAs and energy-efficiency metrics will become negotiation levers.

Data residency and sovereignty: Regions are tightening requirements, meaning enterprise deployments will need granular controls for where conversational data is processed and stored. This favors platforms with flexible regional deployment options and hardened compliance tooling.

Labor economics and automation ceilings: Conversational platforms can materially reduce agent workloads, but the economics vary by use case and geography. Realistic modelling of agent redeployment and upskilling costs is essential to capture net benefits.

Procurement: Build RFx processes that require vendors to disclose compute and energy cost exposure and to offer options for fixed-price or indexed pricing tied to sustainability KPIs.

Architecture: Favor modular, API-first architectures that allow switching LLM providers and deploying workloads selectively across clouds and on-premises regions to meet latency and residency constraints.

Governance: Institute a vendor governance council with legal, security, cloud ops, and business stakeholders to monitor model drift, compliance, and performance against outcome KPIs.

People and operations: Combine automation with a reskilling roadmap for contact center agents to handle exception management and higher-value interactions; model net labor savings conservatively.

Sustainability: Include energy efficiency and carbon accounting as first-class procurement criteria—not an afterthought.

Immediate actions: Run a 90-day vendor discovery sprint using the report’s evaluation framework and RFP templates to short-list platforms against your performance, compliance, and sustainability constraints.

Medium-term program: Execute a six- to twelve-month pilot that tests agentic actions (task execution), LLM cost measures, and hybrid deployment architectures under real traffic.

Long-term planning: Integrate conversational AI roadmaps into broader digital transformation and workforce strategies, using the report’s scenario models to stress-test budgets and timelines.

To preserve the report’s role as a strategic decision-making asset, this public preview emphasizes trends, vendor positioning, and operational recommendations while omitting granular regional and vertical revenue breakdowns, detailed vendor market shares, and per-segment pricing benchmarks. Those core tables, price modeling spreadsheets, and reproducible forecast scenarios are available in the full report and accompanying data package.

For executives preparing procurement, integration, or transformation programs in 2026, this research brief provides the strategic context and the operational playbook. Access to the complete dataset and vendor benchmarking tools will enable precise TCO calculations, regional residency comparisons, and contract negotiation playbooks tailored to your organization’s risk profile.

PW Consulting stands ready to support tailored vendor selection workshops, architecture reviews, and procurement negotiation support informed by the full report.

For detailed analysis of this topic, please visit the official page:Web Conversational Ai Platform Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com