Precision Measurement Revolution: Global Profilometer Market Poised to Reach $544.2 Million by 2031

Other |

2026-05-07 08:59:29

PW Consulting’s latest market intelligence brief on the PWM DC Motor Speed Controller market furnishes senior executives, product leaders, and corporate strategists with the decision-grade insights they need to act confidently in 2026. Built on a rigorous historical window (2020–2025) and a forward-looking forecast (2026–2032), the study quantifies growth, maps competitive dynamics and supply-risk vectors, and translates data into executable go-to-market and technology plays.

Pwm Dc Motor Speed Controller Market

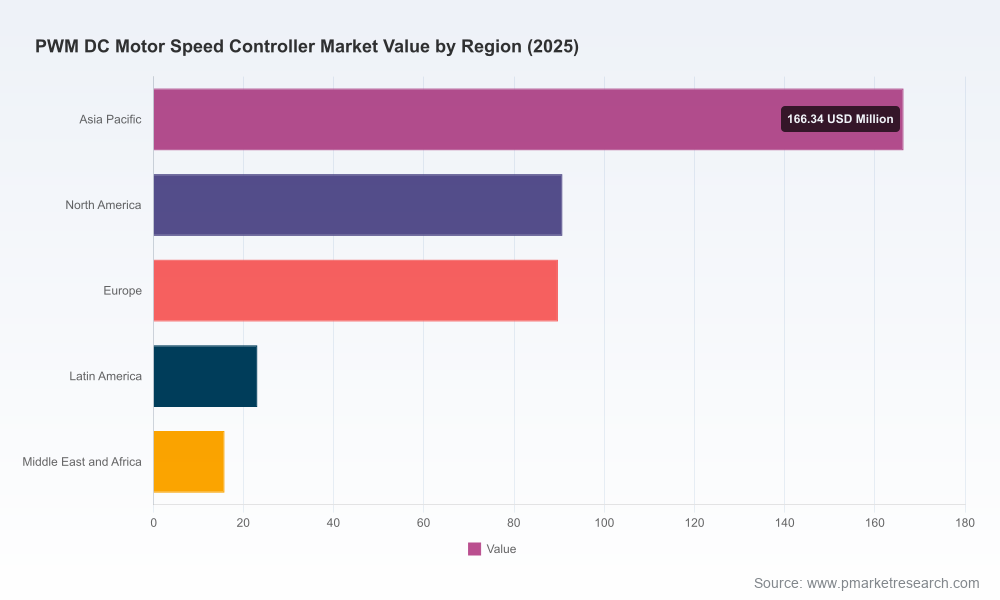

Measured momentum: The market’s trajectory—anchored to a 2025 base and projected forward at a 6.42% CAGR—signals sustained demand expansion across industrial automation, transportation electrification, robotics, and consumer power-management segments. This is not cyclical noise; it is structural demand that will reshape supplier economics and platform strategies through 2032.

Pwm Dc Motor Speed Controller Market

Concentration and competitive tension: With leading suppliers accounting for a notable share of market revenues, the ecosystem sits between fragmented component suppliers and a handful of platform leaders. That mix creates acquisition windows for system integrators and pricing leverage opportunities for component incumbents seeking scale.

Pwm Dc Motor Speed Controller Market

Operational urgency: Raw-material volatility, new functional-safety standards, and tightening regulatory compliance are converging in 2026—forcing firms to prioritize resilient supply chains, modular product architectures, and faster certification roadmaps.

Base year and coverage: The analysis uses 2025 as the base year, with the most recent historical series covering 2020–2025 and forecasts extending to 2032.

Growth expectation: The market is forecast to grow at a compound annual growth rate (CAGR) of 6.42% across the 2026–2032 projection horizon.

Competitive concentration: Market concentration metrics highlight a competitive landscape where the top three and top five vendors hold meaningful but not dominant shares—creating room for challenger strategies and targeted consolidation.

Standards and safety: Compliance requirements have sharpened. Recent functional-safety guidance demands adjustable PWM speed control in many industrial motor-drive applications, elevating the certification burden (and the value of compliant IP and reference designs).

Material and component cost pressure: Power semiconductor supply chains are experiencing pricing stress—silicon wafer prices for MOSFET production rose materially due to constrained capacity, and copper price volatility is increasing the cost base for inductors and magnetics. These cost inputs are compressing margin for component makers and are driving supply-chain hedging strategies among OEMs.

Regulatory constraints: Updates to electronic-substance legislation in major markets have tightened allowable lead content in solder and increased the certification work required for CE marking—making design-for-compliance an early-stage product decision rather than a late-stage checkbox.

Thermal and reliability engineering: High-current PWM controllers above certain thresholds are now recognized as requiring rigorous thermal management and MOSFET junction-temperature mitigation to avoid catastrophic failure modes—raising BOM and design complexity for high-power SKUs.

Our vendor analysis combines product-architecture mapping with channel reach and IP depth. The report profiles all major players—from broad-based semiconductor houses to niche motor-controller specialists—and benchmarks them on technical breadth, application fit, certification readiness and channel strategies.

Tier-1 semiconductor platform providers: Companies with broad analog and power portfolios bring integrated PWM driver ICs and MOSFETs that simplify system design for automotive and industrial customers. Their strengths are scale, established quality systems, and roadmaps for platform-level integration.

Pure-play motor-driver specialists: Smaller, focused suppliers offer market-ready motor controller modules that accelerate prototyping and reduce time-to-market for robotics and hobbyist applications. Their differentiation is speed of implementation and form-factor optimization.

Representative firm highlights (selected profiles):

Infineon Technologies AG: Offers MOSFETs and integrated PWM motor-driver ICs targeted at automotive and industrial DC motor control, and continues to invest in industrial-grade Motor Control ICs showcased at leading trade events.

STMicroelectronics N.V.: Provides PWM driver families and low-voltage drivers tailored for battery-powered devices and has expanded its low-voltage portfolio with recent product introductions.

Texas Instruments Incorporated: Supplies H-bridge and PWM driver ICs with integrated sensing that support precise speed regulation and higher-current topologies.

Analog Devices, ON Semiconductor, ROHM, Toshiba, NXP and Microchip: Each brings differentiated strengths—whether in precision control, automotive certification, high-efficiency drivers, sensorless control, or flexible microcontroller integration.

Specialist module and controller vendors: Pololu, Cytron, and Dimension Engineering serve fast-growing niches for ready-to-use motor controllers—important for robotics, education, and small-scale automation.

Recent vendor moves underscore the pace of innovation: new low-voltage PWM drivers for battery devices, higher-peak-current dual H-bridges for precision motion, AEC-level automotive certifications and product demonstrations at major electronics trade shows. These developments illustrate both incremental product evolution and strategic investments in application-specific certifications.

Market model and scenarios: A built-for-strategy demand model (2020–2032) with scenario toggles for raw-material shocks, accelerated electrification, and regulatory tightening—enabling CFOs to stress-test capital allocation choices.

Competitive vendor matrix: Comparative scorecards across technical metrics (current handling, sensing, integrated protection), commercial attributes (OEM design wins, channel coverage) and regulatory readiness.

Go-to-market playbooks: Route-to-market strategies tailored to semiconductor vendors, module suppliers, and system integrators—complete with target ICPs, pricing levers, and partnership archetypes.

Supply-chain risk map: Node-level risk assessment for critical inputs (silicon, copper, magnetics), with recommended mitigation tactics—dual-sourcing frameworks, long-lead procurement triggers and vertical-insulation options.

Product and R&D roadmaps: Recommended architecture choices (sensorless vs. sensored, integrated current-sense, galvanic isolation) informed by field failure modes, thermal engineering constraints and certification timelines.

Financial implications: ROI benchmarks for product feature sets and a pricing sensitivity matrix that quantifies margin impact under different material-cost scenarios.

Prioritize compliance-enabled product lines: Make regulatory and functional-safety readiness a gating criterion for 2026 product launches. Early investment in compliant reference designs reduces time-to-market for enterprise customers and creates pricing premium opportunities.

Lock in critical inputs: Execute staged long-lead commitments for silicon and magnetics and consider strategic inventory buffering for high-value production windows—especially where wafer pricing and copper volatility threaten margins.

Modularize to win broader TAM: Offer modular controller platforms with scalable current ratings and firmware-configurable safety levels—this lowers customer integration costs and expands addressable applications without full redesigns.

Seek targeted M&A or alliances: For companies below top-tier scale, acquiring complementary IP (thermal management, regenerative braking) or partnering with module vendors can accelerate access to high-growth OEM programs.

Commercial cadence: Build channel incentives and system-level bundles for industrial OEMs and robotics houses, while maintaining low-friction SKUs for hobbyist and small-automation segments that drive volume and developer mindshare.

Beyond the market report, PW Consulting offers tailored consulting engagements that translate insight into outcomes: buy-side due diligence for strategic acquisitions, product-portfolio optimization workshops, supplier negotiation playbooks, and certification-roadmap management. Our analysts can co-develop a 90–180 day action plan that aligns R&D priorities with near-term revenue opportunities identified in the market model.

This press summary highlights the strategic intelligence contained in the full PWM DC Motor Speed Controller market study while intentionally withholding granular segment tables and regional/application revenue splits. These core figures are reserved for subscribers and report purchasers to preserve competitive value and enable confidential strategic planning.

To access the full dataset, vendor scorecards, scenario-model files and the two-page executive playbook for 2026, please visit our report landing page—or contact PW Consulting to schedule a briefing with the lead analyst. In a market defined by increasing technical complexity and supply-side volatility, timely, disciplined strategy development will determine who captures the next wave of durable value.

For detailed analysis of this topic, please visit the official page:Pwm Dc Motor Speed Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com