Fully Automatic Snow Blower Market: Strategic Preview for 2026 — Why Leaders Must Reassess Product, Channel and Supply-Chain Choices Now

PW Consulting’s new market brief on the Fully Automatic Snow Blower market positions 2026 as a decisive year for companies and investors shaping the next generation of snow-clearing solutions. Our study shows a market that expanded from roughly USD 258 million in 2020 to approximately USD 541 million by 2025, and which is forecast to sustain a robust compound annual growth rate (CAGR) of 16.22% through our 2026–2032 horizon. With total market size projecting materially higher across the forecast period, the window for capturing durable share — and defining standards for performance, safety and serviceability — is narrow but clear for proactive players.

Fully Automatic Snow Blower Market

Why 2026 is an Inflection Point

- Technology convergence: Improvements in RTK-GPS, LiDAR, AI vision stacks and battery systems are enabling genuinely autonomous residential and light-commercial clearing. Proof points from live demos and viral deployments have shifted buyer perceptions of reliability and safety.

- Operational strain in incumbent models: Labor shortages and seasonal workforce variability are accelerating demand for automation. Industry reporting indicates that a substantial share of snow-removal contractors face workforce gaps during peak months, reinforcing interest in technologies that reduce manual dependence.

- Input-cost and supply considerations: Steel and other commodity dynamics remain a planning priority — prices have fluctuated meaningfully in recent quarters, and U.S. steel levels are trading in a range that requires active input hedging and supplier diversification for new-capex programs.

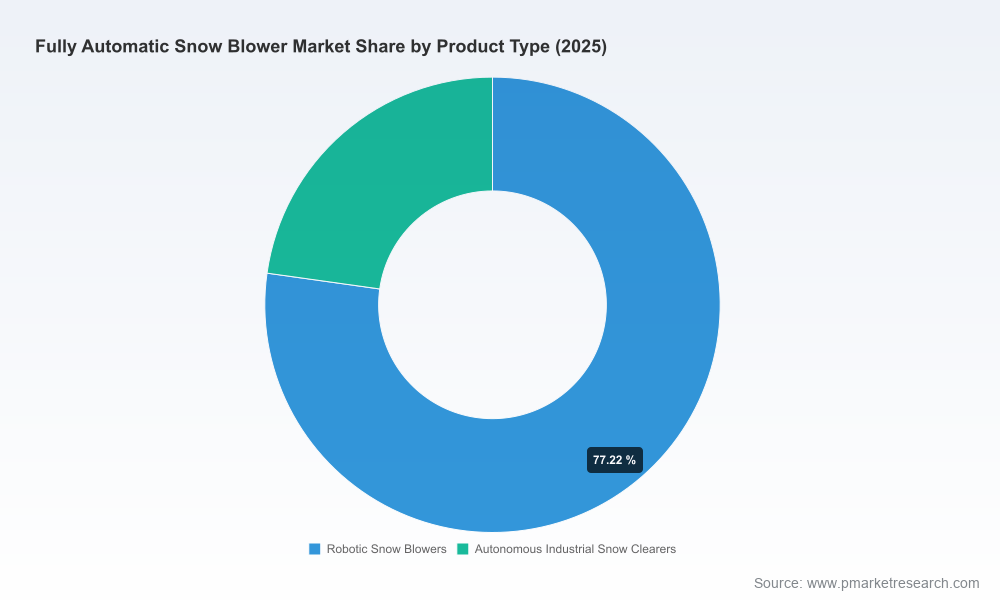

- Market concentration and consolidation potential: Current market concentration shows leading firms holding meaningful share, but the sector’s technological bifurcation (autonomous residential robots vs. industrial snow-clearing systems) opens multiple corridors for both organic scale and bolt-on M&A.

What PW Consulting’s Report Delivers (Practical, Executable Intelligence)

- Validated market sizing and topline forecast for 2020–2032 with transparent methodology and sensitivity scenarios that isolate technology adoption curves, pricing trajectories and replacement cycles.

- Commercial models and go-to-market playbooks tailored for distinct buyer segments (residential adopters, managed-property portfolios, municipal & airport operators), including decision trees for subscription vs. ownership frameworks.

- Supply-chain risk matrix and an input-cost toolkit that models steel price volatility and labor-cost pressures — designed for procurement and financial planning teams to stress-test capex and margin scenarios.

- Competitive positioning maps and vendor assessment frameworks that evaluate not only product performance (clearing depth, autonomy level, cold-start reliability) but also durability, modularity for multi-season use, and software/service monetization potential.

- Commercial KPIs and pilot design templates for rapid field validation — how to structure seasonal pilots, measurement criteria, safety validation and customer feedback loops to accelerate commercialization without over-indexing on scope creep.

Market Dynamics: Tailwinds, Headwinds and What They Mean for Strategy

The market’s strong CAGR reflects a blend of tangible drivers: demonstrable improvements in autonomous navigation; buyer economics that increasingly favor mechanized or robotic options over episodic labor; and rising expectations for continuous, weather-triggered clearing. At the same time, raw material exposure — notably steel — and seasonal labor frictions inject complexity into manufacturing economics. Recent market intelligence shows steel trading in the low thousands of local currency units per tonne in international markets while U.S. prices have normalized into the low-to-mid hundreds of dollars per short ton, pressures that must be modeled into BOM assumptions and supplier contracts.

Fully Automatic Snow Blower Market

Practically, executives should expect closer scrutiny from procurement, with a premium placed on dual-sourcing, nearshoring options for high-weight components, and modular designs that limit steel-intensive assemblies. For product teams, the implication is to prioritize architectures that minimize high-cost metal parts with targeted use of advanced polymers and lighter alloy components where durability permits.

Fully Automatic Snow Blower Market

Competitive Landscape: Who’s Leading and How They Compete

- Yarbo International Inc. — A clear early mover in fully autonomous residential and yard robotics. Yarbo’s fully automatic snow blower and modular yard robots combine RTK-GPS, AI vision and weather-API integration for weather-triggered operation, and their recent live demonstrations (from mountain pop-ups to viral heavy-snow deployments) validate the operational promise of 24/7 autonomy. Their modular approach — enabling year-round utility via swappable attachments — is an important model for expanding lifetime revenue per unit.

- Ariens Company — A traditional incumbent known for high-performance two-stage blowers and robust mechanical design. Ariens’ strength lies in durable manufacturing and dealer networks; while not fully autonomous today, their engineering and distribution capabilities make them a credible partner or acquirer for autonomy-enabling technologies.

- The Toro Company — Toro brings breadth in powered outdoor equipment and demonstrated competence building semi-autonomous turf systems. Their pathway is likely to be evolutionary, leveraging battery platforms and connected services for residential and light-commercial adoption.

- Husqvarna AB — With a deep background in autonomous lawn mowers and power equipment, Husqvarna presents a cross-application innovation model where autonomy learnings from lawncare can be transferred into snow applications — particularly around sensor fusion, durability, and large-scale service ecosystems.

- Larue — A specialist in industrial, airport-grade systems, Larue occupies the high-capacity end of the market. Their engineering emphasis on heavy-duty rotary systems and robust components positions them for continued relevance in large-scale municipal and aviation contracts, even as lighter autonomous units penetrate residential and last-mile commercial niches.

Across these profiles, there is a discernible split: some players are moving from mechanical superiority to systems integration (sensors, software, telematics), while others are layering autonomy onto proven platforms. For 2026, strategic winners will be those that pair field-validated autonomy with rigorous service models and modular hardware that mitigates seasonal revenue downturns.

Strategic Imperatives for 2026 Decision-Makers

- Define your autonomy playbook: Decide early whether to build, buy or partner for autonomy stacks. The choice should be informed by timetables for RTK and AI maturity, existing dealer capabilities, and aftermarket service economics.

- Re-architect cost to win: Integrate commodity-price scenarios into product roadmaps. Favor modular subassemblies that allow late-stage regional sourcing and reduce exposure to single-supplier interruptions.

- Lock in pilot lanes and use cases: Run season-length pilots across contrasting climates and property types to create credible performance datasets. Use those datasets to support regulatory engagement, insurance underwriting and commercial warranties.

- Monetize software and services: Consider subscription models (remote monitoring, automated dispatching, predictive maintenance) that convert one-time hardware sales into recurring revenue and lock in customer relationships through service guarantees.

- Plan for channel evolution: Traditional dealer networks remain valuable for installation and service, but new channels — direct-to-consumer digital sales, managed-service providers, and municipal procurement platforms — will demand distinct margins, logistics and support models.

- Use M&A tactically: With market concentration at modest levels among leaders, strategic tuck-ins (sensor suppliers, telematics platforms, specialized OEMs) can accelerate capability acquisition without disrupting core manufacturing footprints.

How to Use This Report in 2026 Planning

- Inform board-level strategy and FY2026 budgets with scenario-weighted revenue and margin outcomes that reflect autonomous adoption timelines.

- Prioritize R&D and capex investments where ROI windows close fastest: autonomy sensors, battery thermal management for cold-weather operation, and modular mounting interfaces.

- Shape commercial pilots and reference accounts to accelerate validation, enabling faster channel conversion and premium positioning for early adopters.

- Map acquisition targets and partnership priorities using our vendor assessment framework to identify capability gaps that threaten go-to-market timelines.

PW Consulting’s full study contains the granular segmentations, regional and application breakdowns, company scorecards and downloadable financial models that underpin the insights summarized here. In this preview we have intentionally surfaced strategic logic, competitive direction and operational implications while withholding detailed segment-level numbers and proprietary scoring to drive decision-makers to the full dataset and model package.

Next Steps

Senior leaders preparing 2026 plans should use our findings as a checklist for immediate actions: finalize autonomy sourcing decisions, re-run BOMs under current steel-price scenarios, and launch at least one cross-climate pilot before the next winter cycle. For access to the complete dataset, interactive financial model, and a tailored briefing for executive teams, please visit the PW Consulting report page. The full report provides the granular segmentation and proprietary company scoring necessary to convert the strategic narrative above into executable programs and investment decisions.

For detailed analysis of this topic, please visit the official page:Fully Automatic Snow Blower Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com