U.S. Artificial Sweeteners Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-22 09:35:19

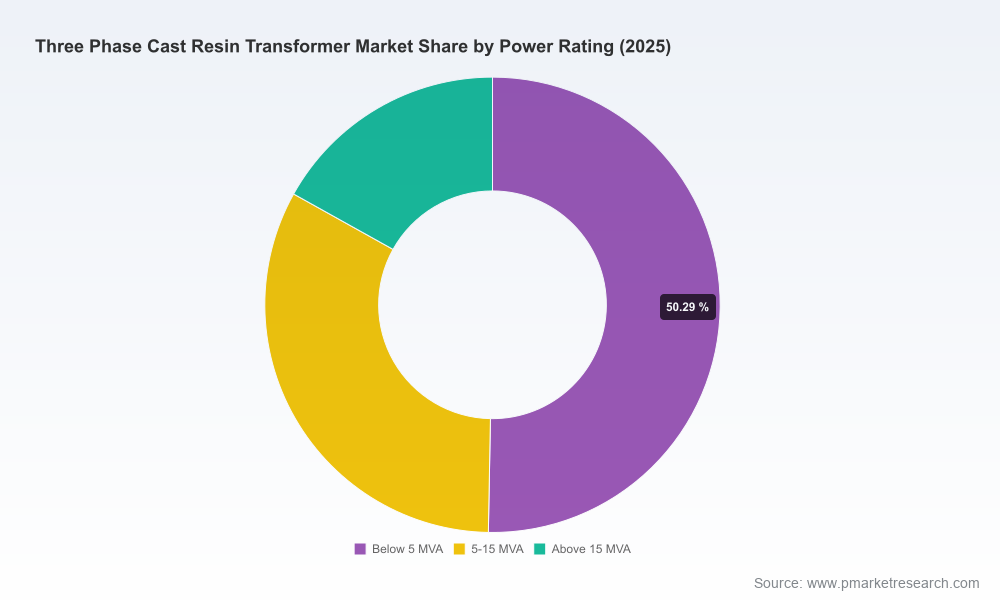

PW Consulting’s Three Phase Cast Resin Transformer Market study provides a decision-oriented preview for corporate leaders preparing strategies in 2026 and beyond. At a market size of USD 4,200 Million in the report’s base year (2025) and an expected compound annual growth rate (CAGR) of 6.85% through the 2026–2032 forecast window, the sector is entering a period of steady, structurally supported expansion driven by urbanization, renewable integration, and tightening efficiency and safety regulations. Our analysis synthesizes historical performance (2020–2025), a seven-year forecast (2026–2032), supply-side dynamics and competitor manoeuvres to deliver practical guidance — while reserving the granular segmented tables for readers who download the full report.

Three Phase Cast Resin Transformer Market

Momentum: The market has grown from a clearly measurable base in 2020 to USD 4.2 billion in 2025, and the modeled outlook reaches roughly USD 6.68 billion by 2032 under the central-case projection. This trajectory implies meaningful investment windows across product development, production capacity and aftermarket services.

Three Phase Cast Resin Transformer Market

Structural drivers: Three durable trends underpin demand — densification of distribution networks in urban and industrial nodes, higher deployment of renewables requiring compact and fire-safe medium-voltage solutions, and electrification of industrial loads that favor dry-type, cast resin designs for safety and footprint constraints.

Three Phase Cast Resin Transformer Market

Risk-return balance: The CAGR near 7% signals attractive top-line growth, but manufacturers and buyers must navigate raw-material volatility, evolving efficiency regulations and moderate market concentration (CR3 ≈ 28.5%; CR5 ≈ 42.1%) that leaves room for both incumbent expansion and targeted new entrants.

Capacity and localization: With selective capacity expansions already announced by tier‑1 players, supply chain localization and regional footprint optimization will be decisive. Firms should prioritize capacity options that shorten lead times for high-growth end-markets while preserving flexibility for demand swings.

Product roadmap and standards compliance: New and pending efficiency regulations (for example, U.S. DOE amendments and EU ecodesign requirements) will make lower-loss designs table stakes. Roadmaps must incorporate low-loss core materials, refined cooling approaches and verifiable testing protocols aligned with IEC 60076-11.

Cost-management and hedging: Epoxy resin is a core input; recent market observations show material price differentials by geography that materially affect unit economics. Procurement strategies should combine long-term agreements, strategic suppliers and inventory policies to mitigate margin erosion.

Services and lifecycle positioning: As installations accumulate, aftermarket services (predictive maintenance, retrofits, and life-extension programs) will provide durable margin pools and differentiation opportunities, especially where clients favor low‑risk, non‑oil solutions for indoor/high-density sites.

The market is led by large diversified power-equipment manufacturers and specialist transformer firms. The competitive picture is a mix of scale players expanding capacity, engineering-focused specialists optimizing performance envelopes, and agile manufacturers pushing product miniaturization and compliance. Highlights from the last 18 months illustrate strategic playbooks:

Siemens Energy (Munich, Germany) — continues to invest in capacity and broad product breadth. A major investment announced in 2025 underscores a bet on scale and integrated offerings across oil-filled and dry-type technologies.

ABB (Zurich, Switzerland) — maintains a strong presence in mission-critical segments like data centers and urban infrastructure with established dry‑type ranges and an emphasis on safety and reliability.

SGB‑SMIT Group (Regensburg, Germany) — positions as a high‑reliability specialist with product lines up to substantial MVA ratings and attention to environmental classes for demanding industrial and renewable settings.

Regional and technology specialists — TMC Transformers, Fuji Electric, Schneider Electric, Eaton, Hitachi Energy, Hyosung, Toshiba, Efacec, Pearl Electric and others — are pursuing differentiated strategies from compact designs to localized production and compliance-focused variants. Notable recent moves: Hitachi Energy’s 2025 expansion in North America and Fuji Electric’s early‑2026 compact model launch, both indicative of market segmentation between volume/scale and product innovation plays.

Raw-materials and manufacturing inputs are key control points. Epoxy resin — the encapsulant that provides fire resistance and moisture protection central to cast resin transformers — has shown price dispersion across geographies. These input dynamics flow directly into pricing, procurement strategies and margin sensitivity. Manufacturers should model sensitivity scenarios that reflect short-term price shocks and medium-term commodity normalization. Vertical integration of resin supply is rarely economical for many players, so strategic offtakes, diversified suppliers and pass‑through pricing clauses are practical mitigants.

Regulation is shaping product design choices. The EU Ecodesign framework and tightened U.S. DOE efficiency levels are accelerating adoption of lower-loss transformer designs and raising the bar on lifecycle and lifecycle-cost arguments. IEC 60076‑11 remains the cornerstone technical standard, defining performance and environmental/climatic classes that many buyers now mandate. For commercial leadership, aligning product certification roadmaps with these normative frameworks — and communicating verified performance in procurement tenders — will be a source of competitive advantage.

PW Consulting’s full report goes beyond high-level narrative and contains ready-to-use deliverables for executives and strategy teams, including:

Validated market-size series (historical 2020–2025; forecast 2026–2032) and scenario-based sensitivity models to test price, regulation and demand shocks;

Supplier and competitor scorecards that blend technical capability, geographic footprint and go-to-market posture;

TCO and lifecycle cost templates for procurement teams comparing cast resin variants against alternative technologies under regionally differentiated loss and service-cost assumptions;

Capex planning matrices and factory-utilization playbooks that translate market growth into required manufacturing investments with payback illustrations;

Regulatory compliance checklists and testing-roadmap templates keyed to IEC and major regional rules;

Deal playbooks for M&A or strategic alliance activity, including valuation levers for bolt-on manufacturing assets and service platforms.

These elements are designed to be immediately actionable in 90–180 day strategic sprints while supporting longer-term portfolio decisions.

For CEOs and corporate strategy teams: Assess where you want to compete on scale versus specialization. The medium-term market path supports both expansion and focused premium plays — clarity of ambition and resource alignment will matter.

For product and engineering leaders: Prioritize designs that balance low-loss performance, compactness and class‑compliant fire ratings. Rapid prototyping of modular platforms reduces time to market for localized variants.

For supply‑chain and procurement heads: Implement multi-sourcing strategies for critical resins, embed price‑adjustment mechanisms in contracts and consider near‑shoring for strategic end-markets.

For commercial and aftermarket teams: Build service portfolios and performance guarantees; aftermarket revenue will be a durable margin contributor as installed bases grow.

The Three Phase Cast Resin Transformer market presents a clear growth runway into 2032 underpinned by regulatory tightening, electrification trends and safety-driven demand for dry-type solutions. Yet, the path is neither homogeneous nor frictionless: raw-material volatility, compliance timelines and concentrated supplier moves create both threats and opportunities.

PW Consulting’s full Three Phase Cast Resin Transformer Market report contains the detailed segmentation, regional breakouts, vendor-level benchmarking and downloadable financial models that corporate teams need to convert this strategic preview into executable plans. For executives preparing capital allocations, product roadmaps or M&A screens in 2026, the report is designed to be a practical companion to rapid decision cycles — showing you what to prioritize and how to stress-test assumptions without waiting months for bespoke consulting work.

To review the complete dataset, segmentation tables, and tactical templates referenced here, please visit the PW Consulting publications page and download the Three Phase Cast Resin Transformer Market report. The full deliverable unlocks the granular breakdowns that support the high-level guidance in this preview.

For detailed analysis of this topic, please visit the official page:Three Phase Cast Resin Transformer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com