Amber Ampoules Market Growth Forecast with 7.5% CAGR by 2031

Other |

2026-02-18 10:07:10

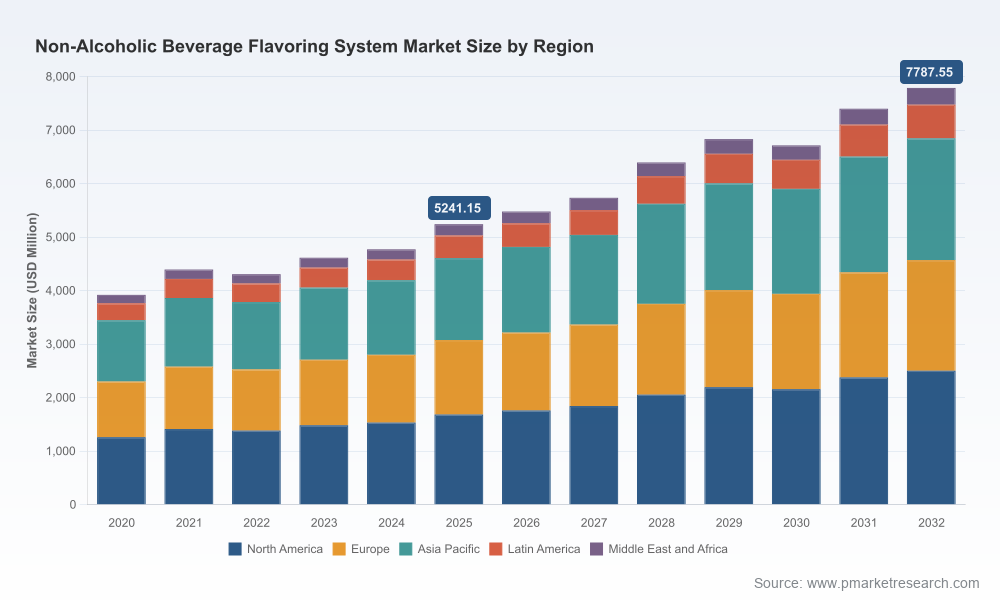

PW Consulting’s latest market study on the Non-Alcoholic Beverage Flavoring System market (base year 2025; forecast period 2026–2032) synthesizes quantitative trend analysis with pragmatic, action-oriented guidance for commercial and R&D leaders planning their 2026 strategies. The market has expanded from a 2020 baseline and reached approximately USD 5,241.15 Million in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of about 5.82% through 2032, reaching an estimated USD 7,787.55 Million by 2032. Our analysis shows a market that is neither atomized nor monopolistic: the leading three suppliers account for roughly two-fifths of the market while the top five control just over half, creating both scale advantages and meaningful space for mid-size innovators.

Non Alcoholic Beverage Flavoring System Market

Investment prioritization: with steady mid-single-digit growth expected across 2026–2032, firms must choose between capacity investments, targeted product innovation, or M&A to capture above-market returns.

Non Alcoholic Beverage Flavoring System Market

Product strategy inflection points: consumer preference shifts—toward reduced sugar, botanical complexity, and clean-label declarations—are compressing product development cycles and reweighting the value of natural and advanced delivery chemistries.

Non Alcoholic Beverage Flavoring System Market

Supply and regulatory risk: raw-material concentration dynamics (e.g., citrus-derived flavor inputs) and a continuing wave of labeling mandates mean procurement strategies and supplier diversification are now strategic priorities.

The market’s trajectory between 2020 and 2025 demonstrates resilience alongside episodic volatility; our modeling attributes this pattern to commodity-driven cost swings, faster-than-expected adoption of plant-based and functional beverages, and new product introductions anchored in health claims. Over the 2026–2032 forecast horizon, growth is driven by three converging vectors:

Health-driven reformulation: sugar reduction and functional fortification push beverage developers to adopt taste-modulation and flavor delivery systems that preserve sensory profiles while improving nutritional perceptions.

Flavor complexity and botanical premiums: demand for layered, botanical-inspired notes (elderflower, yuzu, lemongrass, lavender) has elevated the role of extraction technologies and specialized blends—favoring suppliers with botanical supply chains and R&D depth.

Production and packaging innovation: encapsulation, micro-emulsions, and cold-fill compatible systems enable new categories (e.g., transparent functional beverages, premium low-calorie mixers) and influence sourcing and co-manufacturing decisions.

R&D and portfolio rebalancing — Prioritize scalable natural systems and taste modulation platforms. Firms should map current SKUs against “clean-label readiness” and establish fast-track reformulation pilots for top-volume SKUs that face regulatory or retailer pressure on sugar and labeling.

Procurement hedging and supplier partnerships — Build supply-risk heatmaps for critical botanicals and citrus derivatives. Given commodity valuation pressures in adjacent raw-material markets, organizations that combine long-term offtake agreements with diversified extraction partners will reduce margin volatility.

Manufacturing and capability investments — Decide between buy-versus-build for advanced delivery technologies. Recent capacity expansions by some players signal that regional speed-to-market can become a differentiator; prioritized investments should be aligned with targeted customer segments and co-manufacturing footprints.

M&A and alliance playbook — Seek bolt-on acquisitions to add specialized delivery chemistries or botanical sourcing. Our scenario modelling shows that targeted acquisitions in the natural extract space and micro-encapsulation capabilities can accelerate time-to-market and justify premium positioning.

Commercial and GTM segmentation — Adopt a value-selling approach with beverage OEMs: segment customers by reformulation urgency and openness to co-development. Offer modular solutions—ranging from off-the-shelf blends to bespoke flavoring systems tied to joint consumer testing.

The market balances a set of global flavor houses with regional specialists and emerging ingredient innovators. Strategic leaders combine deep R&D, wide distribution, and sustainability narratives; challengers compete on agility, botanical sourcing, or proprietary delivery technology. Key incumbents we analyze in the report include:

Givaudan — Global leadership with comprehensive natural and sustainable flavor solutions, strong capacity for tailored non-alcoholic beverage systems and an emphasis on clean-label and advanced delivery formats.

International Flavors & Fragrances Inc. (IFF) — Broad portfolio and technical depth in taste modulation and encapsulation technologies, enabling complex applications in sparkling and wellness beverages.

Symrise AG — Robust R&D pipeline and versatility across natural and functional flavor platforms targeted at beverage formulators.

Kerry Group plc — Strength in clean-label and functional flavor systems; known for integrating taste enhancement with nutritional optimization.

Sensient Technologies Corporation — Focus on vibrant natural profiles and nuanced delivery approaches, often favored by premium and craft beverage producers.

dsm-firmenich — Emphasis on sustainable, performance-driven systems and formulation support for low-calorie, functional beverages.

Archer Daniels Midland (ADM), Cargill, Tate & Lyle — Ingredient and systems specialists with strong supply-chain reach and integrated sweetening/taste portfolios suitable for large-scale co-manufacturers and beverage multinationals.

Takasago, MANE, Döhler, Robertet — Regional and specialty players supplying botanical extracts, syrups, and niche flavor systems, often leveraged by product developers seeking provenance and artisanal profiles.

Recent corporate moves underscore strategic priorities: Döhler’s 2025 capacity expansion targeted agility for liquid flavor systems; Robertet’s “Futuring Naturals” platform highlights investment in natural, botanically-driven offerings; and new product lines from niche providers underscore the fast pace of plant-based flavor innovation. These tactical shifts are signals: scale matters for global supply but agility and botanical authenticity can earn premium positioning in growth segments.

Comprehensive market model — An audited market-size model with base-year 2025 benchmarks and scenario-based forecasts through 2032. (Note: detailed segmented tables, region- and application-level line items, and supplier share matrices are available in the full report.)

Strategic heatmaps — Procurement risk maps, technology adoption curves for encapsulation and delivery systems, and an innovation ROI prioritization matrix.

Supplier and capability assessment — Comparative scorecards for incumbent and challenger suppliers across R&D depth, sustainability credentials, delivery tech, and commercial reach.

Operational playbooks — Reformulation playbooks for sugar-reduction and botanical integration; co-development contracting templates; pilot-to-scale manufacturing checklists.

M&A target screen — Criteria-driven shortlists for bolt-on targets across botanical extraction, micro-encapsulation, and regional compounding capabilities, with financial sensitivity scenarios.

Regulatory & claims tracker — A modular dashboard tying labeling trends and national mandates to formulation levers and go-to-market claims.

Case studies and quick-win pilots — Field-tested examples of reformulation and launch pathways that reduced time-to-market and preserved sensory equity.

Short-term (0–12 months): execute reformulation pilots on priority SKUs; secure strategic supply agreements for critical botanicals; initiate one co-development partnership focused on taste-modulation for low-sugar beverages.

Medium-term (12–36 months): evaluate targeted capacity investments or contract-manufacturing partnerships; pursue one bolt-on acquisition if it delivers proprietary delivery technology or botanical sourcing; embed consumption trend monitoring into NPD governance.

Long-term (36+ months): build a platform of differentiated flavor systems (natural + encapsulation + functional claims) that can be spin-licensed to customers or monetized via private-label agreements.

The Non-Alcoholic Beverage Flavoring System market presents a compelling combination of stable aggregate growth and dynamic pockets of premiumization. For leaders plotting 2026 moves, success will come from aligning product innovation with demonstrable supply resilience and strategic commercial models that monetize reformulation needs. PW Consulting’s full report contains the calibrated segment-level models, supplier scorecards, and executable playbooks necessary to convert insight into measurable action. To access the complete data tables, segmented forecasts and our supplier matrix, visit the PW Consulting report page and download the full study.

For detailed analysis of this topic, please visit the official page:Non Alcoholic Beverage Flavoring System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com