Human Milk Oligosaccharides (HMOs) Market: Size, Share, and Future Growth

Other |

2026-05-27 11:48:41

PW Consulting’s latest market study on the global Elevator and Elevator Control Market provides a strategic compass for corporate leaders making investment, M&A and product roadmap decisions in 2026. The market has demonstrated resilient expansion through the early 2020s and is expected to continue growing at a mid-single-digit compound annual growth rate (CAGR) over the 2026–2032 forecast period. Our integrated view — combining top‑down macro modelling with vendor-level intelligence and scenario stress‑testing — is designed to convert industry noise into decision-ready options without exposing the proprietary segmentation tables that subscribers obtain in the full report.

Elevator And Elevator Control Market

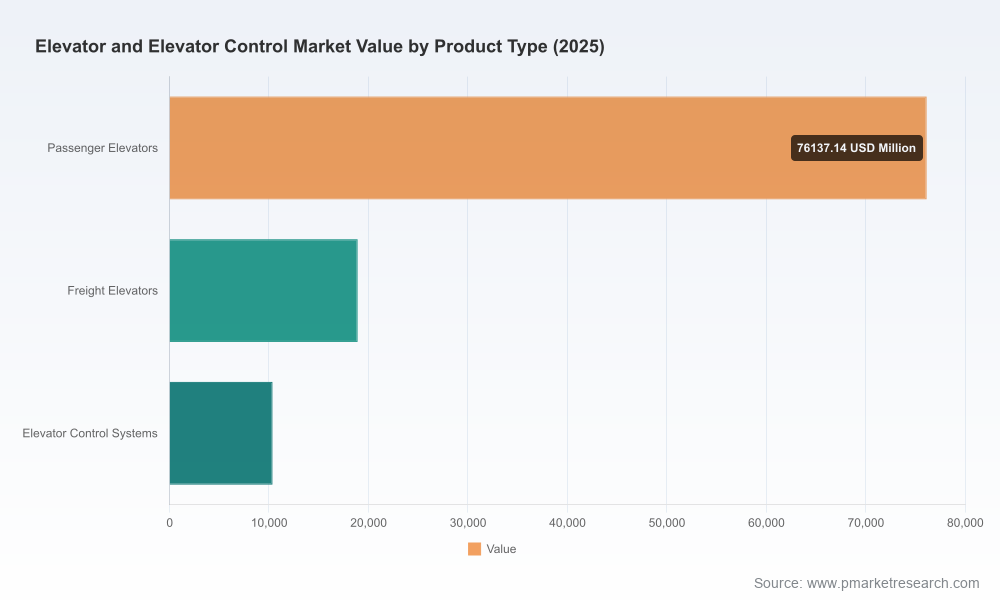

Momentum and scale: After recovering from pandemic-era disruptions, the global market approached a major structural inflection by 2025. PW Consulting’s base-year analysis shows a multi-year progression that culminates in a strong addressable market going into 2026, providing the scale at which strategic initiatives—such as electrification, smart controls and modernization—become commercially material.

Elevator And Elevator Control Market

Predictable growth vector: Our forecasts incorporate a 5.51% CAGR for the forecast window, enabling CFOs and strategy teams to model multi-year returns on capital for new product launches, service network expansions and selective acquisitions with greater confidence.

Elevator And Elevator Control Market

Concentration and competitive economics: Market concentration is meaningful — the top three global players collectively control a substantial portion of market value, and the top five command an even larger share. That concentration creates differentiated competitive dynamics for incumbents and entrants alike: incumbents can leverage scale in installation and service; challengers must pursue niche specialization, component-level innovation or geographic focus.

Prioritize modernization and services as margin multipliers. As installed bases age and regulatory standards update, modernization and maintenance services offer higher margin, recurring revenue opportunities than new equipment sales alone. Our report maps realistic service revenue trajectories under three adoption scenarios and quantifies required field-force investments and digital tooling.

Make smart controls a product and business model bet. Energy-efficiency mandates, regenerative drives, and IoT-enabled building management integrations are rapidly moving from value-add to expectation. Companies that bundle hardware, software and analytics in modular subscription formats will capture outsized lifetime value; the report provides playbooks for packaging, pricing and partner ecosystems.

Embed regulatory change into product roadmaps. The international standards landscape is shifting: new ISO standards scheduled around 2026 and updated North American safety codes require product and testing adjustments. Compliance timelines are non-trivial and should be front‑loaded in R&D planning to avoid late-stage rework.

De-risk raw‑material exposure and supply chains. Steel price volatility and upstream iron‑ore dynamics continue to influence manufacturing cost structures. The study includes hedging and sourcing scenarios — from localized vertical integration to long‑term supplier agreements — that align with different capital intensity profiles.

Use M&A to accelerate capability rather than scale alone. Given market concentration, bolt‑on acquisitions that provide control electronics, IoT platforms, or regional service footprints can materially shorten time‑to‑market. The report screens opportunistic targets by capability, revenue profile and integration complexity.

We profile global OEMs, major component suppliers and fast‑growing regional challengers. Our vendor analysis focuses on strategic positioning, product roadmaps, service economics and technology differentiators.

Otis Worldwide Corporation — Continues to lead on breadth of offering and service scale. Recent product launches aimed at mission‑critical applications (including a heavy‑duty range for data centers) and modular modernization packages illustrate a two‑track approach: defend large institutional contracts while monetizing retrofit cycles. Tactical takeaway: incumbents should evaluate partnerships for mission‑critical applications and accelerate modular modernization SKUs.

KONE Corporation — Positions itself on energy efficiency and smart controls. Dual‑channel safety controllers and energy‑optimized platforms are symptomatic of a platform approach to building systems integration. Tactical takeaway: prioritize interoperability and software‑defined differentiation to extract premium positioning in new installations.

Schindler Group — Emphasizes sustainability and urban mobility. The firm’s investment in IoT and smart mobility solutions signals a strategy focused on long‑term urban projects and integrated building services. Tactical takeaway: target public‑private partnerships and smart city frameworks to scale pilots into municipal programs.

TK Elevator — Advances eco‑efficient platforms for low‑ to mid‑rise buildings. The focus on reduced life‑cycle emissions dovetails with corporate decarbonization programs and green building incentives. Tactical takeaway: manufacturers should incorporate life‑cycle cost narratives into bidding and financing conversations.

Mitsubishi Electric, Hitachi, Fujitec, Hyundai, Toshiba — These firms retain strengths in high‑speed, reliability and regionally tailored solutions. Hitachi’s expanded development facilities and Mitsubishi’s modernization focus show continued R&D and product investment. Tactical takeaway: monitor product roadmaps for migration paths into higher‑value segments (data centers, high‑rise) and seek collaboration opportunities for shared platform components.

Component suppliers (Inovance, NIDEC, Shanghai STEP) — Control systems, motors and drive components are strategic choke points. Supply of advanced drives and safety‑certified controllers creates bargaining power for specialists and represents an M&A target class for OEMs seeking vertical integration. Tactical takeaway: evaluate strategic minority investments or long‑term supply contracts to secure component roadmaps.

Standards and compliance: The calendar for ISO 8100 series and updated North American safety codes requires companies to revalidate design, testing and documentation workflows. Delays in compliance adaptation carry financial and reputational risk; companies must plan regulatory projects as multi‑quarter initiatives.

Raw materials and cost pressure: Steel and iron‑ore price movements remain a cost lever. Manufacturers should model both spot‑price sensitivity and hedged procurement strategies into product costing to protect gross margins under different demand scenarios.

Urbanization and sustainability drivers: Demand for energy‑efficient and connected vertical transportation is increasingly policy‑driven. Regenerative drives, permanent magnet motor recycling and lifecycle emissions accounting are shifting from differentiators to expectations.

Service and digitalization: IoT platforms and predictive maintenance are moving from proof‑of‑concept to scale. Firms that can operationalize sensor‑to‑service processes will convert data into new service tiers and improved asset uptime.

The study is intentionally practical. It equips executive teams with the following deliverables to accelerate decision cycles:

Transparent market model (base‑year, historical trend and forecast scenarios) with downloadable datasets for financial planning.

Scenario‑based demand dashboards that stress test growth under regulatory, raw‑material and urbanization variants.

Vendor strategic profiles and competitive heatmaps highlighting capability gaps and acquisition candidates.

Product and services playbooks — including go‑to‑market routes, pricing frameworks, and field‑service redesign templates.

Regulatory compliance roadmap and testing matrix aligned to ISO and ASME timelines.

Supply‑chain and procurement levers with recommended hedging and supplier strategies by risk appetite.

M&A screening methodology and a short list of targets by capability and integration complexity (detailed targets and valuations available in subscription files).

Run a rapid profitability assessment that treats modernization, digital services and component integration as distinct business units. Use the report’s revenue and margin scenarios to prioritize capital allocation.

Start compliance‑driven product rework programs now. Allocate R&D sprints to meet new ISO and regional code requirements with sufficient testing cycles before market enforcement dates.

Map the installed base for service conversion. The largest, near‑term operational upside lies in converting legacy consumables and inefficient units to subscription‑style service contracts.

Hedge raw‑material exposure and secure strategic supplier relationships for key control and motor components; consider minority investments in critical component makers to stabilize supply lines.

Use targeted M&A to acquire control systems, software stacks or regional after‑sales networks rather than seeking scale alone—this accelerates time‑to‑capability in a concentrated market.

This preview highlights the strategic vectors that PW Consulting’s Elevator And Elevator Control Market report translates into concrete plans for 2026. We deliberately present the high‑value, decision‑oriented insights here while preserving the proprietary segmentation, vendor scorecards, and downloadable financial models for subscribers. For the full dataset, vendor valuations, and bespoke scenario runs tailored to your balance sheet and strategic priorities, visit our report page or contact PW Consulting’s industry practice to arrange an executive briefing.

For detailed analysis of this topic, please visit the official page:Elevator And Elevator Control Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com