Cystinosis Treatment Market Business Opportunities: Expanding Role of Specialty Clinics and Rare Disease Treatment Centers

Health |

2026-05-28 12:32:15

PW Consulting’s new market intelligence briefing on the Fixed Drone Hangar market equips senior executives and infrastructure planners with the strategic line of sight needed for 2026. Built on a consolidated historical window (2020–2025) and a forward-looking forecast (2026–2032), the analysis projects a robust industry expansion — a market growing from USD 1,542.4 Million in the 2025 base year to USD 4,629.12 Million by 2032, implying a compound annual growth rate (CAGR) of 17.0% over the forecast period. This preview explains why that trajectory matters to buyers, integrators, and investors, outlines the practical tools included in the full report, and highlights competitive and regulatory dynamics that will shape procurement and deployment decisions in 2026.

Fixed Drone Hangar Market

Regulatory inflection: 2026 will be the first full year when many jurisdictions move from experimental BVLOS allowances into routinized approvals. FAA-approved test sites, Partnership for Safety Programs (PSP) frameworks, and EASA/FAA guidance are converging on predictable pathways for fixed installations — hangars that support autonomous deployment, charging, and remote operations are now explicitly within those compliance conversations.

Fixed Drone Hangar Market

Operational scaling pressure: Organizations that validated drone concepts in the previous five years must now design for sustained, unattended operations. That transition elevates hangar attributes such as autonomous docking reliability, integrated charging architectures, environmental resilience, and remote health diagnostics from “nice-to-have” to procurement gatekeepers.

Fixed Drone Hangar Market

Commercial momentum: The market’s growth profile (17.0% CAGR) reflects a shift from experimental pilots to capital investment cycles. This creates windows for early movers to lock supply chains and for later adopters to benefit from maturing standards and competitive product differentiation.

This briefing is a strategic trailer: it demonstrates depth while reserving the full microdata and segment-level breakdowns for the complete report. For teams preparing 2026 investments, the report contains operationally focused assets you can use immediately:

Procurement playbook — an RFP template and supplier scorecard keyed to autonomy, environmental rating, modularity, and lifecycle support.

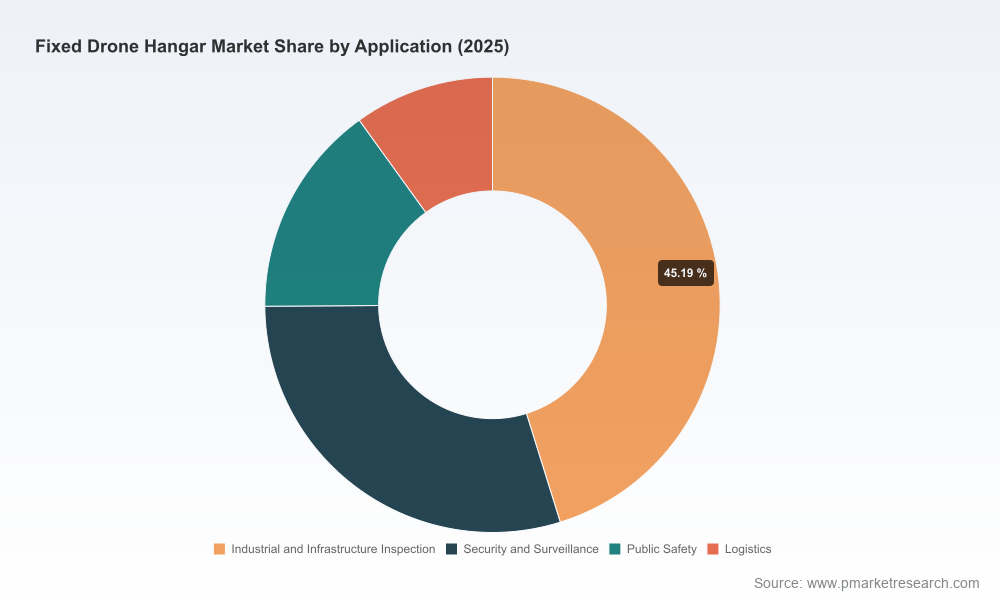

Deployment scenarios — site selection matrices that align hangar class to mission profiles (inspection, security, public safety, and logistics), with phased roll‑out budgets and risk heatmaps.

Technology roadmap — timelines and vendor capability maps for docking solutions, thermal management, fast‑charging subsystems, and integrated comms (5G/ethernet/mesh).

Regulatory pathway checklists — stepwise guides for BVLOS permissions, CE/EU conformity considerations, and FAA/EASA engagement strategies.

Financial models — configurable TCO and ROI calculators (USD, Million-unit basis) with sensitivity analyses for utilization, energy pricing, and service contract terms.

The Fixed Drone Hangar market shows measurable concentration; the top three vendors account for a meaningful share of sales while the top five firms consolidate the majority of visible commercial momentum. That degree of concentration informs partner selection: established vendors increasingly offer integrated stacks (hangar + comms + charging + fleet management), while niche suppliers specialize in fabric structures, rapid-deploy shelters, or modular charging systems.

HEISHA Technology Co., Ltd. (Shenzhen) — HEISHA’s V330 and D300 VTOL smart hangars emphasize precision docking (reported >99.8% accuracy), integrated charging, and fleet management capabilities tailored to industrial inspection and emergency response. Their product launches through 2025 signal aggressive productization for unattended VTOL fixed‑wing operations.

Skycharge (Germany) — Offering CE‑certified, weatherproof hangar and charging systems designed for BVLOS operations, Skycharge’s platform focuses on rugged operating envelopes (wide temperature range, IP protection), 360° adaptive docking, dual‑battery fast charging, and modular scaling — features that appeal to operators prioritizing standards compliance and cross‑platform compatibility.

JOUAV (Chengdu) — JOUAV’s VTOL automatic hangar systems (including upgraded VTOL hangar models) are positioned for unattended medium‑ to long‑duration missions with automated charging, integrated inspection workflows, and data uplink capabilities, reinforcing their strength in large‑scale inspection and logistics deployments.

mb+Partner (mbptech) (Germany) — Distinguishes itself through a systems approach that includes mobile runway elements, hangar gates, 5G comms, and environmental sensing — appealing where remote runway integration and fully automated ground handling are required.

Rubb (United Kingdom) — Specializes in custom fabric‑clad, semi‑permanent and permanent hangars with options for thermal insulation and rapid deployment. Their offerings are frequently chosen for civil and military applications that value rapid installation and configurable protection.

China Xinxing, Liri Structure, ALTUS LSA — These suppliers populate the market’s structural and rapid‑deployment tiers. Their product sets range from large-capacity storage hangars to demountable fabric structures and off‑grid rapid-deploy systems, giving buyers options across the capex/opex spectrum.

Recent product activity — including multiple HEISHA launches in 2025 and JOUAV’s hangar upgrades — underscores an intensifying technology refresh cycle. Buyers must weigh near-term performance gains against integration and lifecycle support commitments when selecting partners.

Operational approvals for BVLOS are increasingly tied to fixed installations: regulators expect standardized approaches to safe storage, charging, and automated deployment. The industry is responding with CE‑aligned products and documentation to streamline BVLOS certification pathways in Europe, while U.S. states and federal agencies formalize test sites and PSP frameworks.

Infrastructure choices — from custom fabric cladding with specified U‑values to hardened metal structures — have direct implications for thermal management, energy consumption, and compliance with local building and aviation safety codes.

Leaders will approach 2026 with disciplined criteria that separate speculative pilots from scalable operations. Practical guidance:

Define the autonomy threshold: require objective docking accuracy and uptime SLAs. Autonomous docking performance is a binary gate for unattended operations.

Require standards alignment: products that are CE‑certified or demonstrate a clear path to regulatory acceptance reduce program risk and shorten approval timelines.

Architect for modularity: choose hangars that permit staged deployment (pilot → regional cluster → national scale) and allow incremental CAPEX while retaining commonality of parts and service contracts.

Embed energy strategy: fast‑charging architectures and thermal controls materially affect TCO. Run sensitivity analyses on energy price and duty cycle — templates for these are included in the report.

Lock service and data contracts: beyond hardware, the value accrues from fleet management, predictive maintenance, and uptime guarantees. Negotiate software and analytics ownership up front.

Our methodology blends primary interviews, technical validation, on‑site assessments, and a proprietary market model that aggregates technology adoption curves, regulatory milestones, and capital deployment trends. The full report contains the granular datasets, supplier scorecards, and scenario models that senior teams use to:

Set procurement timelines and budget windows consistent with expected regulatory progress and vendor roadmaps;

Develop competitive sourcing strategies that balance vendor concentration risk against integration benefits (the market’s leading three and five firms account for a significant portion of revenue, a dynamic we unpack in the report);

Quantify TCO and build scalable operational playbooks that incorporate service level metrics for autonomous docking, charging uptime, and environmental protection.

This release is intentionally directional — it surfaces the strategic signals, vendor moves, and compliance inflection points that will determine procurement success in 2026. For the full market model, detailed regional and application splits, supplier-level revenues and share analysis, and downloadable operational templates (including RFPs, ROI calculators, and compliance checklists), please refer to the PW Consulting Fixed Drone Hangar Market report on our website. The full dataset is designed to be directly actionable for procurement, engineering, and corporate strategy teams preparing capital and operational plans for the coming growth cycle.

Contact PW Consulting to schedule a briefing with our senior analysts. In an environment where the market is accelerating at a double-digit CAGR and regulatory clarity is improving, being early, precise, and standards‑aligned will determine which programs achieve sustained, autonomous operations versus those that remain constrained to pilot status.

For detailed analysis of this topic, please visit the official page:Fixed Drone Hangar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com