Economic Impact on the Cardiac Microcatheter Market: Trends and Future Forecasts for 2034

Other |

2026-06-09 14:47:36

As demand for precision surface finishing and high-throughput web processing converges with renewed industrial investment, the global roll coating machine market stands at a strategic inflection point for 2026. Our new PW Consulting market study — built on a rigorous 2020–2025 historical baseline and a 2026–2032 forecast model — shows steady expansion at a mid-single-digit compound annual growth rate (CAGR) and meaningful upside driven by advanced coating technologies, automation, and localized supply-chain responses to raw material volatility and trade policy shifts.

Roll Coating Machine Market

Capital allocation: OEMs and tier-1 suppliers planning 2026 capex cycles need a forward-looking lens on demand velocity and technology premiumization to prioritize lines that will deliver the fastest payback.

Roll Coating Machine Market

Product strategy: R&D and product roadmap teams must reconcile investments in precision deposition (sub-micron coatings, slot-die, microgravure) with market appetite for higher value-added processes such as metallization and electrode coating.

Roll Coating Machine Market

M&A and partnerships: Private equity and corporate development teams will use our forecast framework to size bolt-on opportunities and assess consolidation levers in a market that remains relatively fragmented.

Risk management: Procurement and operations leaders require scenario-tested guidance on steel and coil cost exposure, tariff-driven localization, and spare-part resilience to maintain throughput and margins.

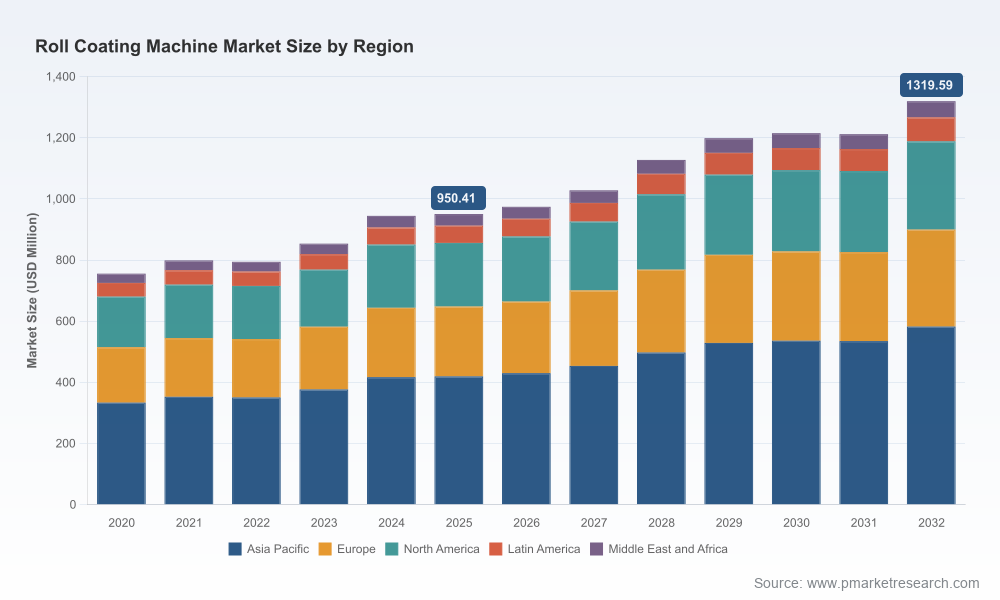

Measured from a robust 2025 base, the roll coating machine market is modeled to expand at a 4.8% CAGR through the 2026–2032 forecast window. Our market model produces a seven-year outlook that illustrates both secular growth and cyclical inflections linked to end-market refreshes in packaging, woodworking, automotive coil coating, and advanced materials. This pace of growth supports selective capacity investments and targeted product premiumization rather than broad-brush volume expansion.

Proprietary demand model calibrated to macro instrumentation, end-market throughput, and investment cycles — enabling scenario testing for conservative, base, and accelerated demand paths.

Price and margin sensitivity matrices that link raw material inputs (notably steel coil dynamics) and logistics cost to machine-level gross margins and total cost of ownership for end-users.

Go-to-market playbooks for OEMs and system integrators, including segmentation of service and aftermarket revenue levers, digital upgrades, and retrofit packages that accelerate recurring revenue.

Technology maturity maps for key coating processes (gravure, slot-die, roller, metallization) with recommended R&D focus areas and investment thresholds by company archetype.

Detailed supplier and buyer heatmaps (regional build vs. buy economics) and a due-diligence checklist for M&A exercises.

Stress-tested scenario planning templates addressing raw material shocks, tariff regimes, and labor constraints — ready to drop into 2026 strategic planning cycles.

The market remains dispersed: the top-three vendors account for under one-fifth of global revenue, and the top-five do not cross the one-third threshold. This concentration profile signals a competitive landscape where regional specialists, niche technology providers, and service-focused players can sustain meaningful positions without being immediately displaced by heavyweight global OEMs. For 2026 strategy, this means both consolidation opportunities (for buyers seeking scale) and defensible niches (for specialists leaning into premium applications).

Our vendor analysis combines capability profiling, recent activity, and technology positioning to produce forward-looking strategic insights. Highlights include:

Black Bros. Co.: Continues to reinforce leadership in woodworking and lamination systems while emphasizing maintenance best practices — a reminder that aftermarket intelligence and operator training are low-friction levers for margin enhancement (Corporate updates, April 2026).

Bobst Group: Product innovation remains central to retaining business in flexible packaging and film — their next-generation automated metallization solution launched in late 2025 signals upward pricing power in high-value film lines (Announcement, Nov 2025).

Yasui Seiki / MIRWEC: A strong play in precision, sub-micron roll-to-roll coating for medical, energy, and optics — strategic for firms targeting high-margin, technology-differentiated segments.

Coatema and Roth Composite Machinery: Positioned for advanced materials and electrode coating where process control and material handling define competitive advantage.

Regional builders (e.g., BARBERAN, Dubois Equipment, Cefla Finishing): Continue to capture application-specific demand through localized service and specialized process capabilities — shown by trade-show visibility and product launches that emphasize digital workflows and wider web-handling (drupa 2024 coverage).

Converters and integrators (e.g., Davis-Standard, The Bronx Group): Compete on system integration, speed-to-market, and turnkey delivery for high-mix production lines.

Black Bros. Co. — strong activity in early 2026 underlines the importance of operational readiness and maintenance intelligence as a competitive differentiator (Apr 2026).

Bobst’s EXPERT K5 — points to a growing premium sub-market for integrated metallization and process expertise (Nov 2025).

BARBERAN’s RCM Jetmaster presence at drupa 2024 — confirms sustained investment by select OEMs in digital roll-to-roll printing and broader web-processing capabilities (May 2024).

Three contextual vectors will materially influence planning for the coming fiscal year:

Raw material and input cost volatility — steel and hot-rolled coil prices, along with regional tariff measures, have increased incentive for localized sourcing and inventory strategies. Procurement teams must model pass-through mechanics and consider hedging or long-term supplier agreements to stabilize machine BOM costs.

Regulatory and trade pressures — steel import measures and carbon compliance costs are reshaping supply chains, often prompting investment in domestic capacity and preferring OEMs with localized service footprints.

Technology premiumization — higher-performance coatings (from sub-micron optical films to conductive battery electrodes) reward tight process control, integrated metrology, and enhanced digital controls. Companies that bundle process expertise with equipment will command higher margins.

Prioritize retrofit and aftermarket programs: Shorter sales cycles and higher margin capture make service-led growth a near-term priority.

Invest selectively in digital twins and predictive maintenance: Small investments in condition monitoring (e.g., roller wear detection) yield outsized uptime improvements and spare-part revenue.

Hedge raw material exposure and localize critical supply: Build supplier scorecards that incorporate tariff risk, carbon fees, and delivery lead time to inform dual-sourcing decisions.

Differentiate through process expertise: Packaged process recipes (e.g., metallization + curing + web handling) reduce customer adoption friction and create high barriers to entry.

Target high-growth verticals with tailored value propositions: Advanced materials, flexible packaging, and instrumentation-grade coatings justify premium pricing for precision equipment.

Calibrate M&A to capability gaps: Acquire for missing process know-how or service footprint rather than headline production capacity if aiming for rapid ROI.

OEM leadership: Use the pricing and margin matrices to set product tiers and to prioritize R&D investments where returns on technology will be greatest.

Plant operators: Leverage the total cost of ownership templates to validate upgrade vs. replacement decisions and to justify retrofit budgets to CFOs.

Investors and corporate development: Apply the concentration and vendor heatmaps to identify consolidation targets and to size integration synergies.

Procurement teams: Adopt the scenario-tested supplier playbooks to negotiate long-term contracts that reduce exposure to coil pricing and tariff swings.

PW Consulting’s Roll Coating Machine Market study combines primary interviews, plant-level benchmarking, and a granular demand model covering types, applications, and geographies. The report includes regional, type, and application splits alongside supplier-level profiles and a detailed forecast through 2032. In keeping with our “trailer” approach, this executive brief surfaces strategic conclusions and practical recommendations while preserving the report’s granular tables and proprietary segmentation data for report subscribers.

For 2026 planning cycles, stakeholders who move from strategy to execution with speed will capture the disproportionate share of near-term gains. PW Consulting’s full report provides the underlying data, sensitivity models, and vendor scorecards required to operationalize the recommendations in this brief. Visit our report page to access the complete dataset, downloadable modeling templates, and a detailed vendor playbook to inform your 2026 decisions.

For detailed analysis of this topic, please visit the official page:Roll Coating Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com