Facial Recognition Payment Devices Market: Strategic Imperatives for 2026 — PW Consulting Preview

As merchants, payment processors, hardware OEMs and system integrators prepare budgets and roadmaps for 2026, PW Consulting’s latest market research on Facial Recognition Payment Devices offers a strategic vantage point. The market has transitioned from niche pilots to a commercially scalable payments adjunct; our study quantifies that transition and translates it into actionable guidance for executives who must decide where, when and how to invest.

Facial Recognition Payment Devices Market

Market snapshot: rapid scale-up and clear runway

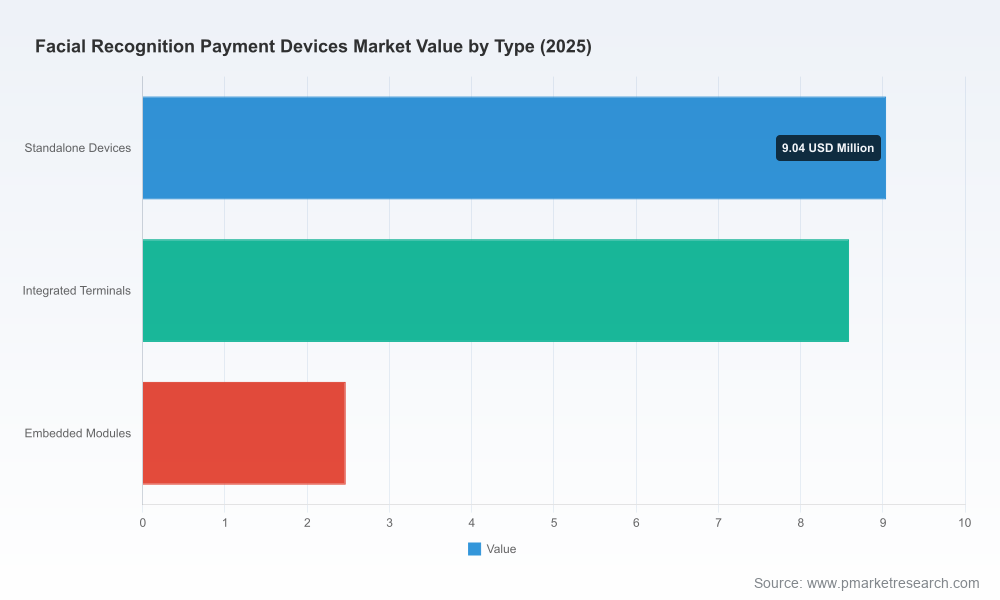

Over the past half-decade the facial recognition payment devices market has moved from early experimentation to commercially deployable solutions. According to PW Consulting’s base-year analysis (2025), the industry expanded from a modest base in 2020 to above USD 20 million in 2025. Momentum accelerates into the forecast window: the market is projected to grow meaningfully in 2026 and beyond, closing the forecast period with strong expansion. PW’s modeling shows a compound annual growth rate of 19.85% across the forecast horizon, underscoring both fast-paced adoption and meaningful unit economics improvements as hardware, sensing modules and biometric stacks mature.

Facial Recognition Payment Devices Market

This growth is not concentrated in a single vendor or geography. Market concentration metrics indicate a moderately consolidated vendor landscape—enough scale among leaders to enable enterprise-grade procurement, yet sufficient fragmentation to preserve competitive innovation and partnership opportunities for new entrants.

Facial Recognition Payment Devices Market

Why 2026 is a pivot year for enterprise decision-makers

- From proof-of-concept to procurement cycle: Technology proofs and small pilots that dominated 2020–2024 are giving way to multi-site rollouts and vendor consolidation decisions. 2026 is when board-level capital allocations will determine which pilots scale and which remain isolated experiments.

- Hardware-software coalescence: Rapid improvements in depth-sensing, edge AI and payment integrations are shifting value from standalone algorithms to vertically integrated hardware–software stacks, changing procurement considerations (warranty, lifecycle, upgradeability).

- Regulatory compliance as a cost center and differentiator: New regulatory regimes and compliance obligations are already shaping product design and GTM strategies; in 2026, companies that bake privacy, governance and explainability into their devices will gain early access to large procurement pipelines.

Key market dynamics and drivers

- UX and throughput gains: Retail and quick-serve use cases prioritize frictionless checkout. Facial recognition that reduces transaction time without compromising authentication accuracy is the primary adoption lever.

- Edge compute and multimodal sensing: Edge AI reduces latency and privacy exposure; multimodal stacks (face plus liveness/depth/behavioral layers) materially improve fraud resistance and merchant confidence.

- Integration with payment ecosystems: Native integrations with payment processors and SDK-friendly POS platforms shorten time-to-revenue for merchant deployments.

- Commercial models evolving: SaaS, device-as-a-service and transaction-revenue-share models are emerging to lower adoption barriers for merchants and to align vendor incentives with transaction volumes.

Regulatory landscape — risk and opportunity

Regulation is no longer background noise; it is a primary commercial variable. Two recent policy milestones are particularly material for 2026 planning:

- China’s Security Management Measures for Facial Recognition Technology (effective June 1, 2025) tightens requirements around necessity justification, bans mandatory biometric-only access when alternatives exist, and triggers registration requirements for processors handling facial data at large scale. For vendors targeting China or Chinese enterprises, built-in compliance features and auditability are procurement table stakes.

- The EU AI Act’s high-risk obligations for biometric systems (in force from August 2025) introduce mandatory risk assessments, transparency provisions and limits on certain uses (e.g., emotion scoring). For solutions intended for the EU market or global enterprises with EU exposure, demonstrating compliance-ready architectures will materially shorten procurement cycles.

Strategically, compliance should be reframed from a cost center to a competitive advantage: privacy-by-design architectures, layered consent mechanisms and auditable logging become differentiators in enterprise RFIs.

Competitive landscape — who to watch and why

The vendor ecosystem spans device OEMs, biometric middleware specialists and sensing module suppliers. PW Consulting’s competitive analysis focuses on firms that combine payment-grade hardware with mature biometric stacks and payment integrations.

- Newland NPT (Fuzhou, China) — Known for smart POS terminals with integrated facial recognition; positions itself toward retail and unattended deployments where secure, compact terminals are required.

- Telpo (Guangdong, China) — Offers payment terminals equipped with 3D-depth sensing cameras aimed at financial-grade authentication and self-checkout use cases; its designs emphasize durability and banking certification paths.

- PAX Technology (Shenzhen, China) — A major Android smart POS manufacturer moving into multimodal biometric integrations via partnerships, enabling persona-driven payments on widely deployed POS platforms.

- NEC Corporation (Tokyo, Japan) — Brings proven biometric expertise and enterprise integration experience; recent demonstrations and deployments underscore its strategic push into hands-free, in-store payments via partnerships with payment processors.

- VisionLabs (Amsterdam, Netherlands) — Focuses on biometric algorithms and SDKs for payment hardware, making it a partner-of-choice for integrators wanting vendor-agnostic software stacks.

- PopID (Pasadena, USA) — Specializes in quick-serve and retail payment flows with a strong focus on UX and speed of transactions.

- PayByFace B.V. & Intema S.A.R.L. — European specialists offering complete face-payment solutions and hardware tailored for contactless biometric transactions and localized compliance needs.

- Orbbec Inc. — A key supplier of 3D sensing modules and cameras commonly integrated into payment terminals; sensor selection materially affects liveness detection and false-accept/reject trade-offs.

Recent industry moves illustrate the trend toward ecosystem partnerships and live deployments. NEC showcased a hands-free payment experience integrated with a major payments terminal at a global fintech event late in 2025, while NEC also deployed recognition systems for Expo environments earlier that year. PAX Technology’s late-2025 partnership to integrate multimodal biometric authentication into its POS terminals underscores OEMs’ strategic shift toward persona-powered payments.

Strategic playbook for 2026 corporate decisions

Executives should approach facial recognition payment initiatives through a staged set of strategic choices aligned to their balance-sheet posture, customer risk tolerance, and regulatory footprint. PW Consulting recommends a prioritized playbook:

- Define the business case before the technology: Quantify throughput, basket uplift and labor-cost offsets at target sites. Use short pilots to validate uplift assumptions and to measure real-world FRR/FAR under local lighting and crowding conditions.

- Favor modular investments: Choose architectures that separate sensing hardware, inference engines and payment integration layers so each can be upgraded independently as sensors and algorithms improve.

- Embed compliance and consent into UX: Design opt-in flows, clear consent dialogs and fall-back authentication paths from day one. This reduces legal exposure and builds customer trust—especially in regulated jurisdictions.

- Procure through outcome-based contracts: Where possible, shift to outcome or usage-based commercial models to align vendor incentives with transaction growth and to lower upfront CAPEX.

- Invest in field operations: Plan for a higher-than-usual service footprint in early rollouts; device calibration, lighting optimization and staff training materially affect performance and perception.

- Build partnerships, not one-vendor lock-ins: Prioritize vendors with open APIs and proven payment integrations. Ecosystem partnerships (POS OEMs, acquirers, processors) accelerate go-to-market and reduce integration risk.

What PW Consulting’s report delivers — practical content for 2026 action

The full market study includes a suite of operational and strategic deliverables designed to support procurement cycles, product strategy and M&A diligence:

- Historical and forecast market sizing with scenario analyses and sensitivity tests for macro and regulatory shocks.

- Go-to-market playbooks for merchants, acquirers and hardware OEMs, including channel strategies and sample commercial terms.

- Vendor benchmarking across technology, certification, integration readiness and service capabilities, plus due-diligence checklists for RFPs.

- Technical roadmaps detailing sensor options, edge-inference trade-offs, multimodal fusion approaches and SDK evaluation matrices.

- Compliance and governance frameworks aligned to China regulations and the EU AI Act, with sample data protection impact assessments and consent templates.

- Pilot design templates, rollout playbooks and TCO/ROI models tailored by deployment archetype.

To respect confidentiality and to drive full-service engagement, PW Consulting’s public executive summary surfaces strategic implications and select macro metrics; the full report includes proprietary segmentation tables, granular regional demand curves, and vendor-specific scorecards.

Conclusion — positioning for competitive advantage in 2026

As facial recognition payment devices move into a growth phase, 2026 will be decisive for organizations that need to convert technical feasibility into commercial value. The market’s strong CAGR and expanding total addressable base create opportunities for value capture—but only for firms that combine user-centric design, compliance-first architectures and pragmatic commercial models.

PW Consulting’s research provides the market sizing, vendor intelligence and playbooks necessary to make those decisions with confidence. For procurement teams, product leaders and investors preparing 2026 strategies, the right mix of pilots, modular investments and compliance capabilities will determine who leads the next wave of biometric payments.

Next steps

- Download the executive summary from PW Consulting or contact our industry team to authorize a full briefing and tailored decision-support package.

- Use our pilot design template to run a rapid, statistically powered test across representative sites before committing to multi-site rollouts.

For detailed analysis of this topic, please visit the official page:Facial Recognition Payment Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com