Asia-Pacific Functional Gummies and Jellies Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-15 09:46:33

PW Consulting’s latest market study on Three Dimensional Topological Insulators (3D TIs) synthesizes technological nuance, supply‑chain realism, and market finance into a single decision‑grade briefing designed to inform corporate strategy for 2026 and beyond. The market is transitioning from a research‑led niche toward commercially meaningful deployments, and our report frames the opportunity with quantitative rigor (historical 2020–2025 benchmarking, 2026–2032 forecasts) and practical, executable guidance for industrial and investor stakeholders.

Three Dimensional Topological Insulator Market

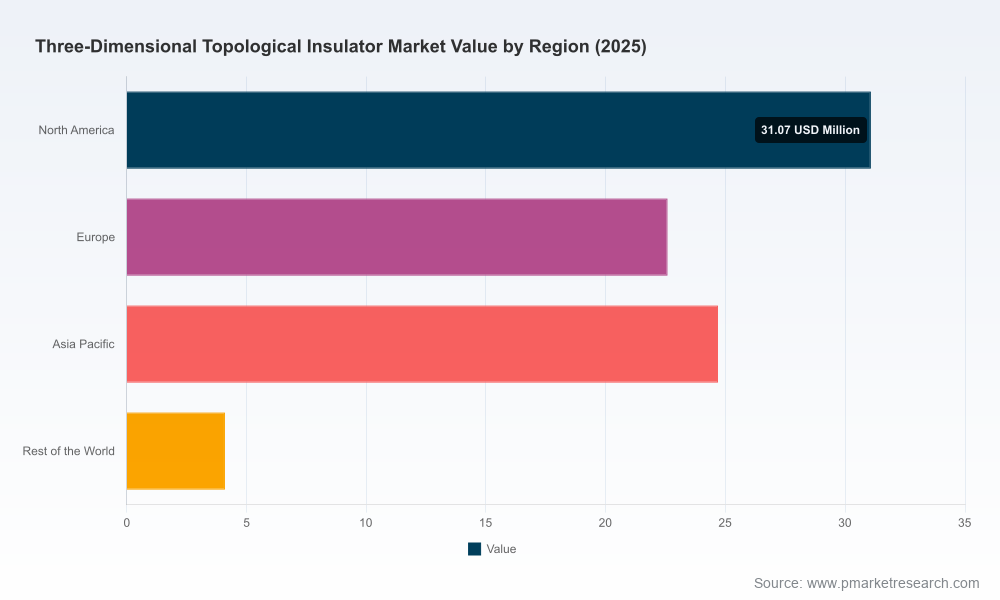

Strong growth trajectory: PW Consulting’s model shows the global 3D TI market expanding from roughly USD 34.12 Million in 2020 to USD 82.45 Million in 2025, with a projected CAGR of about 22.46% across the forecast window. The market is projected to climb to approximately USD 97.51 Million in 2026 and to reach an estimated USD 340.54 Million by 2032 under our base case assumptions.

Three Dimensional Topological Insulator Market

Commercialization catalysts align in 2026: increased device‑level demonstrations in quantum computing and spintronics, maturing thin‑film deposition routes, and growing availability of engineering‑grade materials collectively push the technology from lab demonstrations toward first‑wave commercial uses.

Three Dimensional Topological Insulator Market

Material and policy shocks: raw‑material price volatility and export licensing regimes in 2025 have already reshaped supplier risk profiles — factors that will materially influence sourcing, pricing, and go‑to‑market timing in 2026.

Proprietary market sizing and scenario analysis: transparent methodology with historical calibration (2020–2025) and three forward scenarios (conservative, base, accelerated) through 2032. The report provides volumes, revenue pathways, and sensitivity tables so executives can stress‑test investment decisions against price shocks and adoption rates.

Supply‑chain and raw‑material playbooks: supplier mapping, qualification checkpoints, minimum viable inventory strategies, and a tactical supplier‑audit checklist designed for materials such as bismuth and tellurium chalcogenides.

Technology and IP landscape: side‑by‑side assessment of dominant material chemistries, deposition and crystal growth techniques, and translational risk for scaling from research wafers to manufacturing substrates.

Commercialization timelines and go‑to‑market templates: decision gates for prototype to pilot transition, recommended performance milestones for device integrators, and suggested partnership structures (licensing, toll‑manufacturing, joint development) tailored to 2026 execution windows.

Regulatory and procurement playbook: practical guidance on export license timelines, due diligence on origin chains, and contractual clauses to mitigate supply interruptions and price escalation.

Investor and corporate finance appendices: valuation sensitivities for early‑stage suppliers, capex phasing for pilot fabs, and contracting strategies that preserve optionality while managing cash burn.

Procurement and supplier strategy must become proactive. With raw‑material dynamics tightening in 2025, we recommend establishing multi‑tiered supply agreements, implementing material hedging where feasible, and qualifying at least two independent suppliers for critical chalcogenide precursors before committing to large‑scale pilot runs.

CapEx timing should be staged around technical milestones, not calendar targets. The report’s staged investment profiles allow firms to align plant upgrades or pilot fabs with demonstrable device yields and supply reliability metrics, reducing stranded capital risk.

Partnerships will outpace pure organic builds in 2026. Joint development agreements and co‑located pilot lines accelerate time‑to‑market for device manufacturers while sharing the burden of high‑purity materials qualification.

Regulatory intelligence is a competitive advantage. The 2025 experience with export licensing for tellurium highlights the need for pre‑emptive compliance roadmaps — the report includes a regulatory checklist to shorten approval cycles and to document acceptable end‑use to licensors and customs authorities.

Scenario planning is essential. Given the market’s projected compound expansion (CAGR ~22.46%), companies must plan for scaling demand while maintaining flexibility to contract back if adoption follows a more conservative pathway.

Our analysis integrates 2025 supply shocks that have direct operational consequences for 2026 procurement. Tellurium price spikes and tightened export licensing introduced measurable cost and delivery volatility for tellurium‑containing compounds commonly used in both thermoelectric and topological insulator research pathways. Separately, our concentration analysis shows a market that is moderately consolidated — cumulative revenues for the top firms point to an environment where a small group of suppliers exerts meaningful influence over availability and terms. For new entrants and device OEMs, this combination implies realistic counterparty risk that must be mitigated through contractual and operational safeguards.

HQ Graphene (Groningen, Netherlands | https://www.hqgraphene.com) — Specialist supplier of high‑quality single crystals and prototypical 3D TI materials. Strengths: R&D‑grade crystals, strong academic ties. Considerations for buyers: ideal for early‑stage device R&D but may require augmentation for production volumes.

American Elements (Los Angeles, USA | https://www.americanelements.com) — Broad manufacturer of high‑purity bismuth and tellurium compounds across multiple forms (powders, crystals, sputtering targets). Strengths: scale and product breadth. Considerations: pricing exposure to raw‑material cycles and mixed end‑market exposure.

Stanford Advanced Materials (SAM) (Lake Forest, USA | https://www.samaterials.com) — Offers CVD films and engineered crystals targeted at device developers. Strengths: film deposition expertise and translational materials. Considerations: supply continuity for larger pilot runs should be validated.

Kurt J. Lesker Company (KJLC) (Jefferson Hills, USA | https://www.lesker.com) — Established provider of deposition targets and evaporation materials used in thin‑film fabrication. Strengths: integration into vacuum‑processing supply chains and productization for fabs. Considerations: product lead times can stretch under surging demand.

MSE Supplies LLC (Tucson, USA | https://www.msesupplies.com) — Distributor servicing academic and industrial research; helpful for rapid prototyping. Strengths: distribution agility and access to diverse material lines. Considerations: distributors are useful for prototyping but may not meet volume or consistency needs for production runs.

2D Semiconductors / Nuevogen LLC (Phoenix, USA | https://2dsemiconductors.com) — Focused on guaranteed‑property single crystals and layered chalcogenides. Strengths: well‑characterized crystals with quality guarantees; attractive for device validation. Considerations: scaling capability needs verification for high‑volume device programs.

Collectively, these suppliers illustrate the market’s split between specialized research suppliers and broader materials manufacturers. PW Consulting’s competitive maps and supplier scorecards in the report give procurement teams the tools to rank and qualify partners against criteria that matter most for 2026 execution: purity, reproducibility, lead time, regulatory provenance, and contractual flexibility.

Price shock scenario: rapid upstream price increases propagate to BOM cost. Mitigation: multi‑source contracts, pass‑through clauses, forward contracts for critical precursors, and strategic stockpiles sized to pilot run needs.

Export control scenario: licensing delays impact delivery timing. Mitigation: prequalification of alternate origins, contractual obligations for advance notice, and embedding compliance workstreams within commercialization plans.

Technology risk scenario: lab‑scale recipes fail to scale. Mitigation: phased pilot stages with clearly defined yield and performance gates, and supplier co‑development agreements that allocate IP and risk.

Board level: use the report’s scenario matrices to stress‑test capital allocation for pilot fabs and to frame strategic partnerships and M&A timelines.

Procurement: adopt the supplier due diligence templates and scorecards to de‑risk sourcing decisions and to negotiate favorable, flexible commercial terms.

R&D and product teams: align development roadmaps to the report’s commercialization milestones to avoid premature scaling and to prioritize material qualifications that shorten qualification cycles.

Investors and corporate development: leverage the valuation and market concentration appendices to assess target fit and to price acquisition opportunities more accurately.

This briefing is intentionally crafted as a "trailer": it demonstrates the analytical depth, supply‑chain realism, and operationally oriented recommendations contained in PW Consulting’s full Three Dimensional Topological Insulator Market report while preserving the granular segment and contractual intelligence available in the complete study. For executives and investors preparing material decisions in 2026, the full report provides the detailed segment breakouts, supplier scorecards, granular price‑sensitivity tables, and downloadable procurement templates required for immediate action.

To access the comprehensive dataset, scenario models, and ready‑to‑use playbooks, please download the full report from PW Consulting’s website or contact our industry advisory desk to schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Three Dimensional Topological Insulator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com