Sprinkler Irrigation Market 2033: Opportunities Across Regions

Other |

2026-04-09 10:11:43

PW Consulting today publishes an executive-level briefing accompanying our full Nitroguanidine Market research report (base year 2025). This briefing distills the report’s strategic takeaways designed to inform board-level and commercial decision-making in 2026, while preserving the granular datasets and segment-level models for subscribers. Our goal: equip executives with actionable priority signals — supply risks, regulatory inflection points, and competitive moves — that should shape procurement, product allocation, and investment decisions in the coming 12–18 months.

Nitroguanidine Market

Nitroguanidine sits at an uncommon intersection of markets: energetic materials (defense and propellants), agrochemical intermediates, and selected specialty chemical applications such as automotive inflator propellants and pharmaceutical intermediates. These end markets follow divergent demand drivers — defense procurement cycles, regulatory action on crop protection chemistries, and automotive safety standards — producing a marketplace where strategic timing and supply-security decisions materially impact cost of goods sold and revenue stability.

Nitroguanidine Market

Our 2026 advisory emphasizes three themes for executive action: (1) managing upstream feedstock and captive-production risk, (2) reading regulatory and public-health signals that alter agrochemical demand trajectories, and (3) positioning capacity and offtake arrangements to benefit from asymmetric pricing during short supply episodes.

Nitroguanidine Market

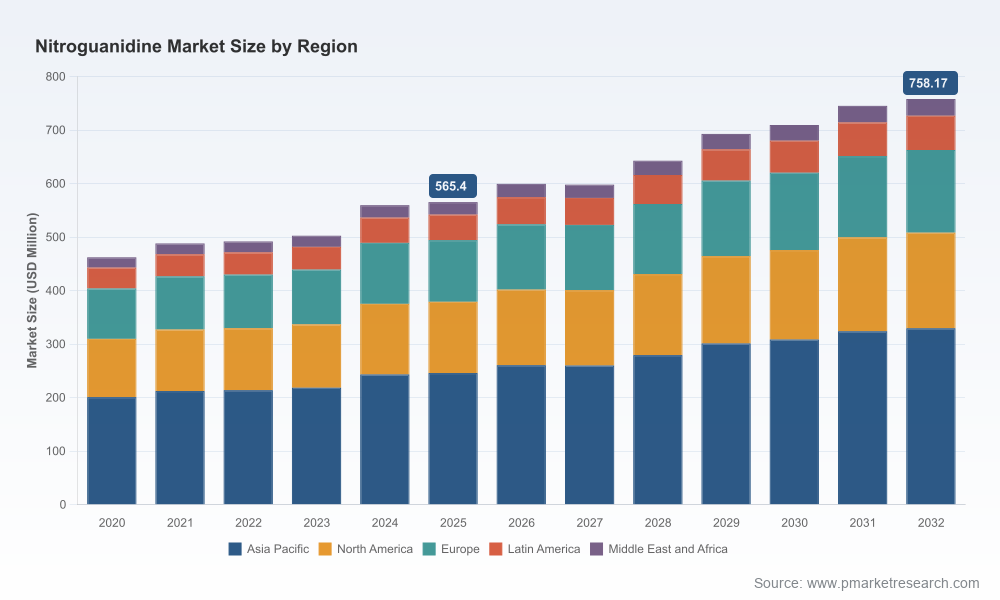

These headline figures indicate steady, mid-single-digit growth rather than rapid commoditization or collapse. Nonetheless, growth is uneven by end use and geography — a pattern that amplifies strategic value in targeted supply arrangements and product development. For 2026 decision-making, the takeaway is clear: volume growth alone will not insulate participants from price volatility; control of feedstock and reliable access to qualified product grades will be the primary short-term differentiators.

Nitroguanidine’s principal upstream precursor is guanidine nitrate, commonly produced from urea and ammonium nitrate through catalytic processes. That dependency creates two pragmatic vulnerabilities:

Recent corporate activity reinforces these constraints. One leading European producer announced a major capacity expansion (largest investment in its history) with new guanidine nitrate and Nitroguanidine capacity slated to come online in H2 2026; construction progress updates in early 2025 confirm project momentum and customer-backed financial structures. Practically, that capacity will alleviate pockets of tightness in European supply chains but will not fully neutralize global imbalances — particularly where logistics, qualification, and regulatory approval slow trans-regional flows.

Regulatory action in key jurisdictions has already altered demand composition for Nitroguanidine as an agrochemical intermediate. Neonicotinoid-related regulatory frameworks targeting pollinator exposure have introduced constraints on certain nitroguanidine-substituted insecticides in parts of the market. While these restrictions do not eliminate agricultural demand for Nitroguanidine globally, they reallocate volumes and increase uncertainty for producers heavily exposed to agrochemical contracts.

For 2026 planners this means two critical implications:

The Nitroguanidine market demonstrates moderate concentration. The top three firms account for a majority share of market supply, and the top five approach a high concentration threshold — a structure that favors incumbents with integrated feedstock positions and established certifications in defense and automotive channels.

Competitive implications for 2026:

The full PW Consulting Nitroguanidine Market report is built for operational use by procurement, business development, and corporate strategy teams. Practical deliverables include:

To preserve competitive value for report subscribers, we intentionally withhold granular segment tables and product-level revenue splits in this release. Those datasets — including regional and application-level breakdowns and vendor-level share details — are available through our subscription gateway.

The full report (base year 2025) delivers a commercial-grade toolkit for 2026 decision cycles: market sizing and forecasting to 2032, supplier profiles and recent development tracking, scenario models, and actionable procurement playbooks. We combine primary interviews, plant-level capacity mapping, and proprietary demand modeling calibrated to observed end-use cycles. The report also includes an industry events timeline and a list of certificates and approvals relevant to defense and automotive procurement.

Executives seeking to operationalize the insights summarized here can access the complete dataset, supplier scorecards, and the interactive scenario model via PW Consulting’s research portal. The full report contains the segment-level outputs and company-specific exposure analysis that underpin the high-level recommendations presented in this release.

The Nitroguanidine market in 2026 will be characterized by steady macro growth but acute micro-level friction: capacity additions that relieve some tightness, regulatory pressures that reallocate volumes, and incumbents doubling down on integration and credentialing. For corporate leaders the strategic question is not whether the market grows — it does, at a mid-single-digit CAGR — but how to convert that growth into durable profit margins and secure supply chains. PW Consulting’s report arms executives with the scenario-tested playbook to make those choices with confidence.

For access to the complete report, datasets, and subscription inquiries, visit the PW Consulting research portal or contact our market intelligence team directly. (Full segmentation tables and vendor-level exposure data are available only in the subscriber edition.)

For detailed analysis of this topic, please visit the official page:Nitroguanidine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com