Car Mounted Ceiling Screen Market: Size, Key Developments and Forecast Report 2026-2034

Other |

2026-06-01 10:51:00

PW Consulting’s latest market research on PVDF-TrFE resin—anchored on a 2025 base year and a 2026–2032 forecast horizon—shows an industry in rapid ascent. The global market value rose from USD 172.5 Million in 2020 to USD 312.45 Million in 2025, and our projection points to nearly USD 698.65 Million by 2032, representing a compound annual growth rate (CAGR) of 12.18% across the forecast window. These headline figures understate the strategic complexity beneath: a high degree of market concentration, specialized manufacturing economics, and material-feedstock volatility are creating both asymmetric risks and outsized opportunities for first movers.

PVDF-TrFE Resin Market

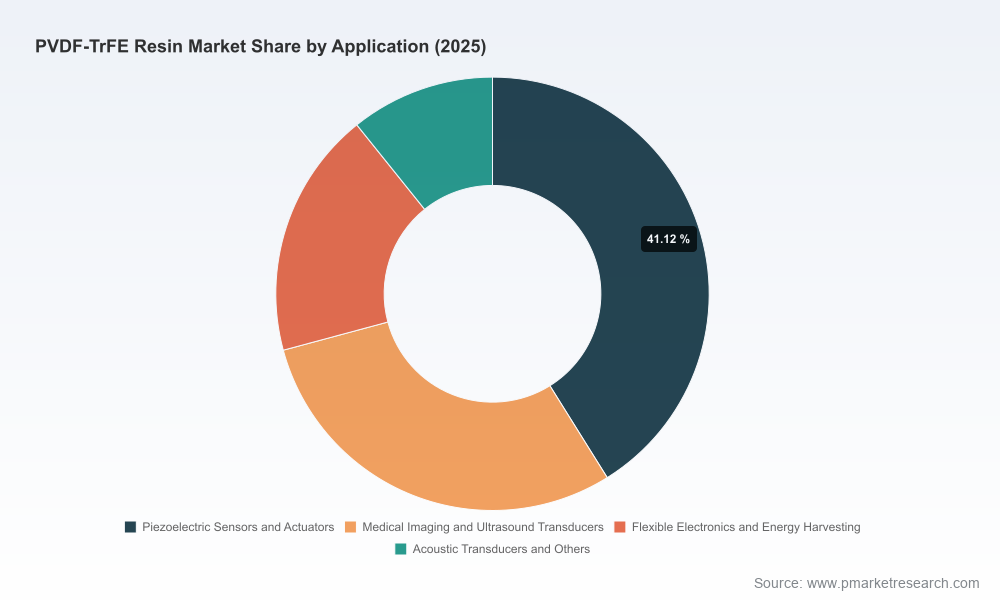

Timing and scale: With the market roughly doubling over the coming half-decade under base-case assumptions, 2026 is the inflection point for capex, capacity commitments, and supply agreements. Decisions taken in 2026 will lock in cost structures and access to advanced grades of PVDF-TrFE at a time when demand from piezoelectric, medical imaging, flexible electronics and energy-harvesting applications is accelerating.

PVDF-TrFE Resin Market

Concentration dynamics: Top-tier suppliers account for the majority of production capacity, creating supplier power that affects price, lead-times and technology roadmaps. Understanding concentration metrics and supplier strategy is critical for procurement and M&A planning.

PVDF-TrFE Resin Market

Upstream exposure: The market’s economics are tightly coupled to the vinylidene fluoride (VDF) monomer price and the incremental complexity of PVDF-TrFE polymerization. Our modelling shows that volatility in VDF and the specialized process premium materially shift producer margins and product pricing—so procurement strategies must be forward-looking, not reactive.

Executive dashboards: concise, CEO/CPO-ready summaries of market trajectory, key inflection points by year, and recommended action windows for 2026–2028.

Dynamic market model: an integrated, scenario-enabled demand/supply model built in an editable format for internal stress-testing. The model allows users to toggle VDF price paths, capacity additions, and adoption curves for target applications to produce P&L and cash-flow sensitivity outputs.

Cost and margin decompositions: granular techno-economic analysis of the PVDF-TrFE value chain, including polymerization cost premiums relative to standard fluoropolymers and the sensitivity of unit economics to feedstock swings and energy costs.

Supply chain and supplier maps: supplier scorecards, disruption-resilience assessments, and a tiered sourcing framework that executives can use to qualify partners or evaluate insourcing alternatives.

Commercial playbooks: go-to-market templates for differentiated product grades (e.g., powders, films, inks), channel strategies for industrial and medical OEMs, pricing playbooks and sample contract clauses to mitigate raw-material pass-through risk.

M&A and partnership screening: a short-listing methodology to identify attractive targets or JV partners, with prioritised criteria covering technology fit, capacity, regulatory exposure and margin solvency under downside scenarios.

Regulatory and sustainability pathways: compliance risk matrices and decarbonization roadmaps tailored to PVDF-TrFE manufacturing, addressing emerging environmental standards in key jurisdictions.

The PVDF-TrFE supplier base blends chemical majors, specialty fluoropolymer houses, and focused niche producers. Market concentration is high, with leading groups commanding most of the production footprint—an important strategic reality for buyers and investors evaluating bargaining power and supply risk.

Arkema Piezotech (France) — a key player with integrated offerings in powders, inks and films for piezoelectric and ferroelectric applications. Arkema’s recent capacity expansion initiatives underscore how incumbents are converting strong demand into tangible upstream commitments.

Solvay (Belgium) — operating at the intersection of high-performance fluoropolymers and specialty copolymers, Solvay remains relevant where specification consistency and global distribution networks matter.

Kureha Corporation (Japan) — brings deep fluoropolymer manufacturing experience and regional strengths that make it a natural supplier for APAC-based OEMs.

PolyK Technologies (United States) — a nimble supplier oriented to R&D and small-batch production, critical for prototyping and early-stage product development where lead-times and customization are decisive.

Peraglobe (United States) — positions itself on premium PVDF-TrFE grades and piezoelectric films, serving higher-margin medical and precision-electronics applications.

Notably, Arkema announced a capacity expansion in February 2025 at its Kentucky site—an example of incumbents translating demand signals into upstream investments. Such moves matter because they influence spot availability and the timing of new-grade launches.

Feedstock volatility: VDF price fluctuations are a primary source of cost risk. Our scenario analysis illustrates how divergent VDF trajectories can swing operating margins meaningfully; procurement teams should incorporate hedging, long-term offtake pricing and alternative supplier clauses.

Production complexity: the polymerization and processing of PVDF-TrFE carries a measurable cost premium over standard fluoropolymers—our synthesis of industry interviews and plant-level models places this premium in a material band that should be built into project IRRs and pricing models.

Regulatory pressure: stringent environmental rules in several jurisdictions are accelerating investments in cleaner processes and emissions controls. Firms that anticipate regulatory-driven CapEx requirements will preserve margins; laggards will face retrofit costs and potential market access constraints.

Lock strategic feedstock arrangements now: secure multi-year VDF contracts or partner with upstream producers to reduce exposure to short-term spot volatility. Consider blended procurement strategies that balance fixed-price and indexed volumes.

Calibrate capacity choices to demand elasticity: avoid knee-jerk capacity additions without testing demand elasticity across end-markets. Use staged expansion or toll-manufacturing agreements to preserve optionality.

Differentiate via application-specific grades: invest selectively in product grades and processing capabilities that create switching costs for OEM customers (e.g., tuned piezoelectric properties, printable inks, or biocompatible films).

Operationalize sustainability early: incorporate lower-emission process pathways into technology roadmaps. Early movers will gain procurement preference from OEMs facing their own ESG targets.

Use M&A tactically: given the market’s concentration, acquisitions can accelerate access to proprietary grades or capacity. Prioritize targets that improve vertical integration (feedstock to finished film) or open strategic geographies.

Implement a disciplined monitoring set: maintain a short-list of leading indicators—VDF spot/forward curves, capacity announcements, regulatory changes, and OEM adoption rates—for weekly executive review.

This study combines primary interviews, company disclosures, plant-level techno-economic models and bottom-up demand modelling across the 2020–2025 historical window, with scenario-driven forecasts for 2026–2032. We have stress-tested the model against multiple VDF price paths and capacity rollouts. While this news release presents high-level market sizing and trajectories, the report includes the full model, assumptions, sensitivity matrices and supplier scorecards that support investment-grade decision-making.

Commission a rapid feedstock exposure audit and present hedging options to the CFO.

Run the report’s market model under conservative and aggressive adoption scenarios to assess capex timing.

Open discussions with top-tier suppliers to understand capacity reservation options and grade roadmaps.

Prioritize an M&A watchlist based on the report’s screening criteria if near-term vertical integration is a strategic priority.

PW Consulting’s PVDF-TrFE Resin Market report is designed to be operational from day one. This release highlights strategic takeaways and the key dynamics executives must factor into 2026 planning cycles; the full report contains the proprietary segment-level datasets, supplier scorecards and editable models that underpin the recommendations. For access to the complete dataset, scenario models and supplier benchmarking tools, visit our report page to request the full deliverable and a tailored briefing with our analysts.

For detailed analysis of this topic, please visit the official page:PVDF-TrFE Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com