Coal Tar Pitch Market 2026: Strategic Briefing from PW Consulting

As companies recalibrate value chains and capital plans for 2026, PW Consulting’s latest Coal Tar Pitch Market report delivers the strategic intelligence executives need to make informed, defensible decisions. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the study synthesizes market sizing, competitive positioning, regulatory trajectories, feedstock dynamics, and actionable playbooks—while deliberately reserving granular segment tables and price models for subscribers. This briefing highlights the report’s most consequential insights and explains how senior leaders can use them to shape procurement, technology, and M&A strategies in the coming 12–18 months.

Coal Tar Pitch Market

Market Snapshot: Growth Profile and Concentration

The coal tar pitch market is returning to a steady, mid-single-digit expansion after a period of volatility. Our 2025 market estimate establishes the industry’s scale, with projections underpinned by a 4.85% compound annual growth rate across the 2026–2032 forecast window. That trajectory incorporates both cyclical demand from primary aluminum and steel electrode segments and secular shifts driven by battery, specialty graphite, and refractory uses.

Coal Tar Pitch Market

Consolidation remains material: the top three industry players account for a majority share of global supply, while the five largest producers control well over two-thirds of the market—an important structural reality that amplifies the strategic importance of long-term off-take, capacity investments, and regional supply corridors.

Coal Tar Pitch Market

Why This Report Matters for 2026 Decision-Making

- Capital allocation and greenfield timing: Our models quantify the lead times and break-even sensitivities for new distillation and pitch-processing capacity under multiple regulatory scenarios, allowing CFOs to evaluate whether to accelerate projects or defer investment.

- Sourcing resilience: Procurement teams will find a practical framework to assess supply risk, factoring in feedstock availability, EAF-driven shifts in tar generation, and emerging maritime/export corridors.

- Regulatory and compliance planning: Legal and sustainability leaders can use our scenario analyses to prepare for tightening PAH-related controls in mature markets and anticipate incremental compliance costs across legacy grades.

- M&A and JV playbooks: Strategic buyers and private equity can prioritize targets by a blended score that combines technology fit, customer concentration, compliance posture, and optionality to serve growth applications.

Report Contents — Practical and Operative

The full study is structured to support executive and operational action. Key deliverables include:

- Market sizing and 7-year forecasts (2026–2032) with scenario runs across high/medium/low demand cases and sensitivity to oil/coal feedstock price swings.

- Portfolio-level playbooks for producers, consumers (aluminum smelters, electrode makers, specialty graphite manufacturers), and traders—each with prioritized tactical moves for 12–24 month horizons.

- Compliance roadmap detailing anticipated PAH and emissions regulation impacts across major jurisdictions and recommended mitigation investments.

- Supply-chain mapping and chokepoint analysis highlighting logistics, port access, and storage constraints that can create regional pricing divergence.

- Valuation and transaction comps tailored to coal tar pitch assets—covering distillation facilities, pitch upgrading units, and liquid pitch export hubs.

- Primary interviews and benchmarking from leading producers and industrial consumers to validate operational assumptions and reveal procurement behaviors.

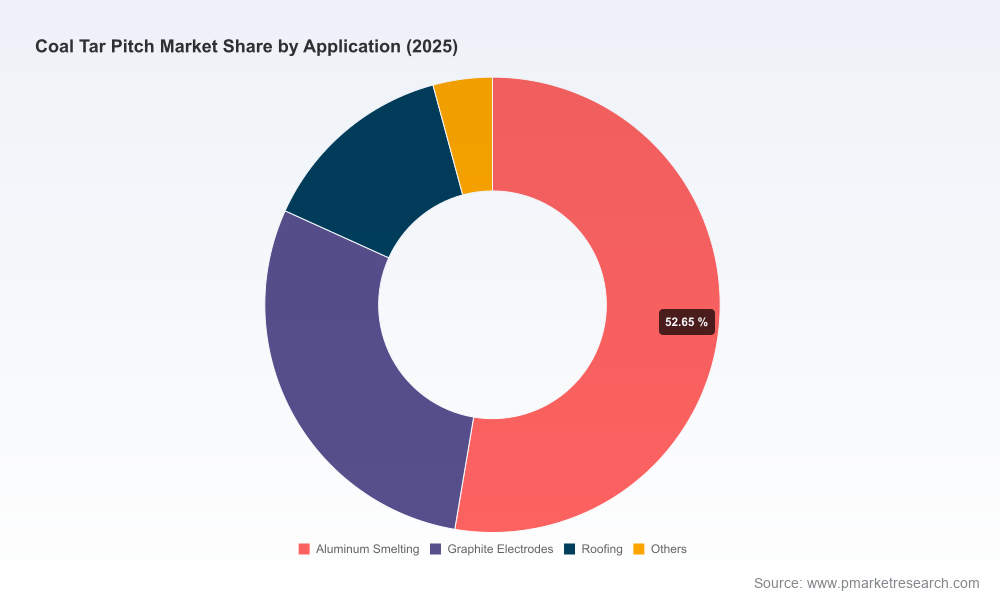

Note: To preserve competitive advantage for report subscribers, this press briefing intentionally omits the granular regional and application split tables. These are accessible exclusively via the full report.

Competitive Landscape: Key Players and Strategic Moves

The coal tar pitch arena combines legacy incumbents with aggressive capacity expansion by vertically integrated players. The following firms exemplify the strategic positions shaping 2026 options:

- Koppers Holdings Inc. (Pittsburgh, USA): A vertically integrated producer with deep roots in carbon pitch from coal tar distillation. Koppers’ portfolio centers on binding-grade pitches used across carbon anodes and graphite electrode production—making it a pivotal supplier to aluminum and steel segments.

- Rain Carbon Inc. (Stamford, USA): A global distillation leader that recently announced new processing capabilities in India, targeting graphite, battery, and aluminum markets. Their incremental capacity rollout is a tactical response to regional demand growth and supply diversification needs.

- Himadri Speciality Chemical Ltd. (Kolkata, India): A high-volume, vertically integrated producer with significant export intent. Recent milestones include opening new export corridors for liquid pitch—an important development for buyers seeking alternative sourcing outside traditional hubs.

- Deza, a.s. (Czech Republic): Focused on binder and impregnating grades, Deza’s European footprint and regulatory familiarity position it as a critical supplier for quality-sensitive applications.

- Shree Shyam Chemicals (Bhilai, India): A regional manufacturer supplying industrial grades across aluminum, graphite, and chemical sectors—representing the important role of mid-sized producers in local markets.

Recent industry actions underscore a two-track market response: incumbents upgrading facilities and new entrants or expansions designed to capture differentiated demand (e.g., battery-grade and low-PAH pitches). Notable developments include Rain Carbon’s facility initiative in Andhra Pradesh and Himadri’s inaugural liquid pitch export corridor—both of which point to strategic de-risking of supply and growing importance of maritime export hubs. Separately, commercial supply arrangements—such as reported long-term MoUs for liquid pitch with major smelters—reflect contracting trends that will shape availability in 2026.

Market Dynamics and Regulatory Headwinds

Two, often competing, forces are redefining the market.

- Supply-side volatility: Coal tar feedstock availability remains sensitive to shifts in steelmaking routes (notably the rise of electric-arc furnaces) and to the economics of tar recovery. These dynamics can compress the feedstock pool, raising raw material cost and incentivizing investment in alternative feedstocks or increased recycling of pitch residues.

- Regulatory tightening: Authorities are increasingly focused on polycyclic aromatic hydrocarbons (PAHs). Jurisdictional examples include longstanding prohibitions in some U.S. states on coal-tar-based sealants and evolving proposals in others that seek stricter PAH limits. In parallel, EU REACH-related controls are elevating compliance costs for legacy grades and accelerating the development of low-PAH products.

For 2026, the intersection of constrained feedstock and rising compliance costs suggests that premium will accrue to producers that can demonstrate low-PAH specifications, robust emissions controls, and flexible logistics. Buyers should assess supplier compliance roadmaps as a de facto component of total cost of ownership.

Strategic Playbook for 2026: Prioritized Actions

- For producers: Prioritize investments that improve feedstock flexibility and emissions performance. Consider modular upgrades enabling graded product conversion to capture specialty markets such as battery and specialty graphite.

- For consumers (smelters and electrode makers): Lock in medium-term supply via flexible offtake arrangements that include quality covenants and optionality to shift grades; evaluate nearshoring or joint-venture processing in key consumption geographies to reduce exposure to export bottlenecks.

- For investors: Target assets with integrated distillation and upgrading capability, demonstrable compliance investments, and access to export infrastructure—these attributes materially de-risk revenue under tightened PAH scenarios.

- For policy and sustainability teams: Embed regulatory scenario analysis into procurement contracts, and finance pilot projects to validate lower-PAH formulations—both to maintain market access and to preempt future phase-outs.

Risk Matrix: What Could Alter the Forecast

- Accelerated decarbonization of steelmaking: A faster-than-expected shift to EAFs could reduce coal tar generation and tighten pitch feedstock availability.

- Regulatory escalation: Aggressive PAH limits or broader bans on certain pitch grades in large markets would compress the addressable market absent compliant alternatives.

- Logistics shocks: Port constraints or trade policy shifts can create short-term regional shortages with outsized price volatility.

- Technological displacement: Breakthroughs in non-tar-based binders or alternative electrode technologies could change demand patterns incrementally over the forecast period.

How Executives Should Use This Intelligence in 2026

Leaders facing 2026 choices should treat this report as a decision-support toolkit rather than a passive market brief. Specific next steps we recommend:

- Run a supplier resilience audit against the report’s supply-chain risk matrix and prioritize remediation where single-source or long-route dependencies exist.

- Stress-test planned capital outlays in a high-compliance-cost scenario to determine the minimal viable investment that preserves market access.

- Negotiate contract clauses that share compliance upgrade costs with strategic suppliers, preserving optionality without outright capital commitment.

- Initiate targeted collaborations with producers that are investing in low-PAH or battery-grade capability to secure first-mover advantage in emerging segments.

Conclusion and Next Steps

PW Consulting’s Coal Tar Pitch Market report provides a pragmatic, scenario-driven foundation for strategic decision-making in 2026. By combining validated market sizing, a clear read on competitive concentration, and an operational playbook tailored to short- and medium-term contingencies, the study enables leaders to protect margins, secure supply, and selectively invest for growth. For practitioners who require the full dataset, detailed segmentation, and proprietary price and cost models that underpin our forecasts, the full report and supporting Excel deliverables are available through our publication portal.

Contact PW Consulting to arrange a briefing with our industry leads and to obtain the complete report and client-only annexes that disclose the granular segmentation and modeling outputs referenced here.

For detailed analysis of this topic, please visit the official page:Coal Tar Pitch Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com