ALAD Porphyria Treatment Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-12 10:32:19

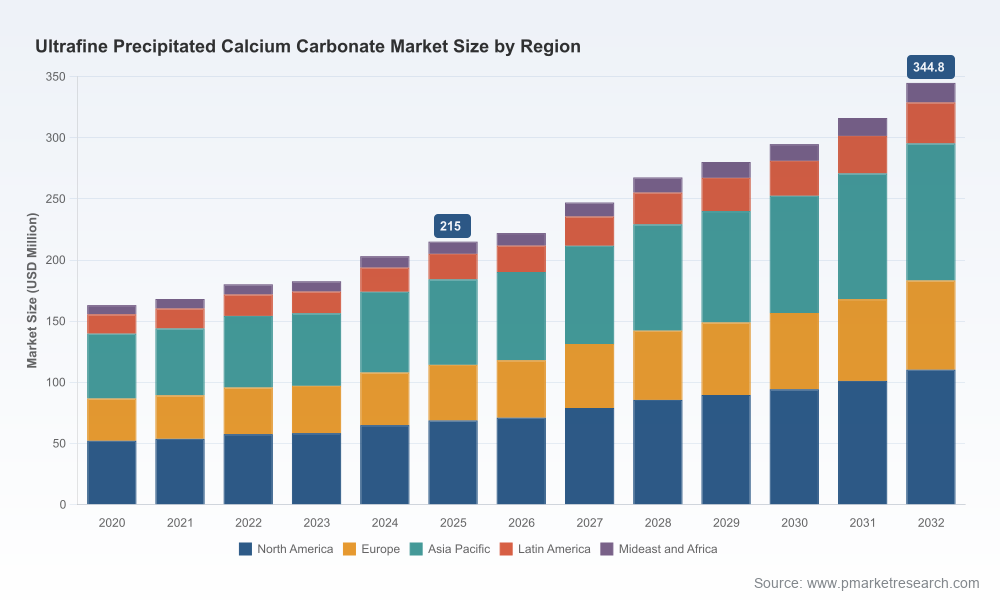

PW Consulting’s latest market intelligence into the Ultra Fine Precipitated Calcium Carbonate (PCC) market synthesizes five years of historical observations (2020–2025) with a forward-looking forecast (2026–2032) to equip executive teams for decisive action in 2026. The market has demonstrated steady expansion through 2025, with an observed uplift into the base year and a compound annual growth rate (CAGR) of approximately 6.98% across the forecast window. Our scenario-driven outlook shows continued demand momentum through 2032, underscoring the need for tailored commercial, operational, and regulatory responses by manufacturers, suppliers, and downstream users.

Ultra Fine Precipitated Calcium Carbonate Pcc Market

Acceleration from specialty applications: Demand for ultra fine PCC is increasingly tied to higher-performance formulations — whether to improve reinforcement in sealants and plastics, to modify rheology in coatings, or to tune optical and tactile properties in high-end composites. That shift favors suppliers that can deliver consistent ultrafine grades and technical support.

Ultra Fine Precipitated Calcium Carbonate Pcc Market

Cost and input volatility: Raw material dynamics and purchasing cycles are less predictable. In North America, for example, calcium carbonate pricing showed a notable month-on-month uptick in mid-2026, reflecting tightened upstream supply and shorter inventory buffers. Procurement teams must adopt more agile hedging and supplier diversification strategies.

Ultra Fine Precipitated Calcium Carbonate Pcc Market

Regulatory and compliance pressure: Tighter chemical safety frameworks in the EU and updated occupational exposure limits in North America have elevated compliance costs and operational constraints across production sites. These trends accelerate adoption of cleaner production processes, drive investment in emissions and water controls, and shift the cost curve for legacy assets.

Fragmentation and opportunity: The competitive structure remains fragmented — leading players account for a modest portion of the market. This fragmentation creates opportunities for regional consolidation, targeted premiumization, and strategic partnerships between feedstock producers and specialty processors.

The report was built to be a decision-making tool. It goes beyond top‑line forecasting and offers operationally relevant modules that executives can apply in 90–180 day planning cycles:

Robust market sizing and trend decomposition — base year 2025 validation and an 2026–2032 forecast built on demand drivers, substitution risk, and end-user elasticity assumptions.

Price-sensitivity and margin impact models — stress-tested against raw material volatility, energy cost scenarios, and tariff/currency swings common to cross-border PCC trade.

Regulatory risk maps and compliance playbooks — granular guidance on the implications of recent REACH tightening and North American workforce safety updates, including compliance CAPEX estimates and timeline impacts for plant modifications.

Supply‑chain and sourcing archetypes — from vertically integrated miners to toll‑processing arrangements — with decision criteria matrices to choose the right model for scale and risk appetite.

Commercial playbooks for premiumization — routes to capture margin via grade differentiation, value‑added coatings, and co‑development with downstream formulators, along with go‑to‑market KPIs.

M&A and partnership screening tools — priority capability maps and valuation heuristics to identify bolt‑on targets, strategic JV partners, or divestiture candidates.

Interactive scenario models — downloadable, editable workbooks that allow management teams to re-run forecasts under custom assumptions and to stress-test capital investment decisions.

The report includes focused company profiles and benchmarking of the most commercially active participants. Rather than disclosing granular market share splits in this preview, we surface the strategic positions and recent moves that matter for 2026 planning:

Calcite GmbH (Germany) — positions itself as a technology-led supplier for specialty ultrafine grades. Their strategic emphasis is high consistency and process control, selling into European specialty formulators that prioritize regulatory conformity and traceability.

20 Microns Nano Minerals Limited (India) — a vertically integrated player expanding technical product breadth. In late 2025 they launched Micron PCC 500, a specially engineered ultrafine grade aimed at improving reinforcement, rheology, surface finish and durability in sealants and high-performance formulations. The SKU launch highlights a playbook focused on rapid time-to-market for differentiated grades.

Guangdong Qiangda New Materials Technology Co., Ltd. (China) — competes on scale and regional supply reliability, investing selectively in functionalization capabilities to capture margin in coatings and plastics. Their strategy is to pair competitive cost structures with incremental product value-adds rather than competing solely on price.

Fujian Sanmu Nano Calcium Carbonate Co., Ltd. (China) — emphasizes downstream customization and technical service, reflecting a common regional play where customer co-development is a key differentiator in crowded local markets.

EZ Chemicals Inc. (China) — notable for its focus on niche grades and regional partnerships; their activity signals an industry trend toward specialization rather than undifferentiated capacity expansion.

Together, these profiles indicate an industry where technological differentiation, regulatory compliance, and supply reliability are as important as cost. Our concentration analysis shows the market remains relatively fragmented, which favors nimble entrants and creates acquisition targets for players pursuing scale or capability gaps.

Based on our multi-scenario analysis and supplier benchmarking, PW Consulting recommends executives prioritize the following:

Immediate review of procurement strategy: incorporate short‑term hedging, multi-sourcing, and strategic safety stocks for critical feedstocks. Rebaseline TCO models to include likely increases in compliance and utility costs driven by environmental regulations.

Fast-track product portfolio rationalization: identify 1–2 premium ultrafine grades where investment in R&D and customer co-development can yield outsized margins, and sunset low-margin, high-variability SKUs.

Prioritize compliance and worker safety CAPEX in 2026: timeline and cost impacts from REACH and updated occupational exposure rules require proactive plant upgrades; delaying these investments risks market access and potential retrospective fines.

Evaluate alliances with regional converters and formulators: partnership models that embed PCC suppliers into downstream R&D reduce customer switching and create sticky demand streams.

Use M&A selectively to acquire capability, not just capacity: target assets that bring functionalization know-how, quality control technology, or regulatory-ready footprints rather than raw tonnage.

Invest in digital quality-control and traceability: ultrafine PCC requires strict control of particle characteristics; digital QC improves yield, reduces rejects, and is a commercial differentiator in regulated end-markets.

The report is designed as a playbook for quarterly and annual planning: use the downloadable scenario models to quantify CAPEX payback under base, upside, and downside demand paths; employ our supplier risk matrix in sourcing decisions; and leverage the regulatory playbook to sequence compliance investments in a cost-optimal manner. Importantly, while this insight brief outlines strategic direction and operational levers, the full report contains the granular datasets, segmentation analyses, and downloadable financial models that corporate strategy and business-unit leaders will need to finalize budgets and investment approvals for 2026.

If your organization is evaluating capacity investments, product development roadmaps, or M&A in the ultrafine PCC space, PW Consulting’s full report is engineered to shorten decision cycles and reduce execution risk. We invite decision-makers to review the complete dataset and scenario workbooks on our report landing page, where you can also request a tailored briefing with our industry team to map the report’s insights to your specific portfolio.

PW Consulting — turning market intelligence into executable strategy for a higher‑performance 2026.

For detailed analysis of this topic, please visit the official page:Ultra Fine Precipitated Calcium Carbonate Pcc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com