France and Benelux Advanced Tires Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-22 05:33:43

PW Consulting’s Silicon 28 Market report, part of the Silicon 28 Market — Silicon 28 Market research series, equips corporate leadership, procurement teams, and technology strategists with the market intelligence required to make high-stakes supply, investment, and product roadmap decisions in 2026. The stable‑isotope silicon sector is transitioning from an R&D niche into a commercially actionable market: our base-year analysis (2025) positions the global market at USD 32.45 Million and our forecast shows sustained expansion through 2032 to USD 108.0 Million at a compound annual growth rate (CAGR) of 18.74% (forecast period 2026–2032). Critically, the market is highly concentrated — the top three suppliers control the overwhelming majority of commercial supply — creating both commercial leverage and supply fragility for buyers.

Silicon 28 Market

Time-sensitive supply decisions: With commercial production ramps and first large-scale contracts moving into deliveries in early 2026, organizations planning product launches, pilot fabs, or quantum device scale-up must crystallize supplier selection, qualification pathways, and inventory strategies now.

Silicon 28 Market

High concentration, few sources: Market concentration metrics indicate a supply base dominated by a handful of specialized providers. Buyers need playbooks for dual-sourcing, long‑lead agreements, and technical acceptance criteria to mitigate single‑supplier risk.

Silicon 28 Market

Cost and input volatility: Feedstock and downstream raw‑material dynamics (including silicon intermediates and polysilicon spot price volatility) directly affect landed cost models for isotopically enriched silicon. Our report translates these inputs into scenario-based cost envelopes for procurement and product-margin planning.

Technology and purity differentiation: Sub‑percent differences in isotopic enrichment translate into measurable performance delta in quantum and advanced semiconductor applications. Technical procurement specifications, test protocols, and acceptance thresholds must be embedded in contracts.

Our bottom‑up market sizing starts from 2020 historicals through the 2025 base year and models adoption curves across quantum technologies, semiconductor research, metrology, and adjacent industrial applications. The outcome is a clear trajectory: the market expands from a niche in the low tens of millions (base year 2025) to triple‑digit millions by 2032 under our central case, driven by commercial productization cycles, capacity additions, and diffusion into high‑performance thermal and quantum applications.

PW Consulting’s forecast scenarios include sensitivity to supplier ramp rates, conversion bottlenecks (material form conversion into SiH4/silane where required), and policy/regulatory interventions. We quantify these scenarios in the report, but provide summary guidance here: companies should model procurement windows in 6–18 month buckets, maintain buffer inventories for pilot-to-production transitions, and structure contracts with performance‑based milestones tied to purity and delivery cadence.

The supplier ecosystem is a mix of technology-led newcomers, national industrial players, and specialty isotope houses. Key strategic archetypes we analyze in depth are:

Technology disruptors leveraging novel separation approaches (e.g., aerodynamic or membrane-based separators) that enable rapid scale and high enrichment levels while remaining commercially nimble.

Established centrifuge and adapted gaseous‑diffusion operators that repurpose high‑reliability isotope infrastructure and scale for greater output continuity.

Specialty isotope service providers offering flexible, custom enrichment runs and conversion pathways for research customers and standards labs.

Representative companies profiled in the report and summarized here include providers employing aerodynamic separation processes, centrifuge-based enrichment, and other adapted isotopic technologies. These firms vary in geographic footprint, vertical integration (from precursor supply through enriched product conversion), and commercial go‑to‑market models (long‑term contracts, spot samples, or toll enrichment partnerships).

Commercial ramp announcements: One aerodynamic‑separation provider began commercial production at a second facility and publicly signalled shipments under multiple contracts moving into early 2026. For buyers this means new commercial sources are available but will be allocated via contractual prioritization — early engagement is crucial.

Capacity and purity milestones: Recent facility upgrades across suppliers reflect a meaningful lift in annual output capacity at high enrichment grades. Procurement teams must ensure technical acceptance criteria align with delivered enrichment and material form requirements (e.g., silane versus elemental or oxide forms).

National players and safeguards: Some production sites operate under international safeguards and national isotope programs, which affects inspection regimes, export controls, and lead times. Compliance and supply‑chain transparency considerations must be embedded into supplier due diligence.

We designed the report to be operationally actionable for decision-makers. Highlights of the practical deliverables include:

A procurement decision matrix that maps use‑case to required enrichment grades, acceptable material forms, test protocols, and contract clauses to protect buyers against purity non‑conformance.

Supply‑risk heatmaps and mitigation templates: scenario-based runbooks for single‑supplier failures, conversion bottlenecks, and logistical delays (including export-control contingencies and inspection scheduling with international agencies).

Financial modeling tools: embedded templates and sensitivities that translate supplier lead‑time, feedstock price variance, and purity yield into P&L and unit cost outcomes for pilot and production volumes.

Technical qualification checklists and test-plan templates for lab acceptance, wafer‑level validation, and device performance correlation studies.

A roadmap for strategic partnerships, including options for toll‑enrichment arrangements, joint‑development agreements, and sample‑to‑production pathways.

The market’s upstream and regulatory context materially alters supplier choice and contract design:

Raw‑material context: Prices and availability of silicon intermediates and polysilicon matter to conversion economics. Recent industry data shows meaningful variability in feedstock markets; procurement teams must build dynamic sourcing strategies that account for quarter‑to‑quarter price swings.

Safeguards and export controls: Some enrichment facilities operate under international safeguards and national isotope programs. These regimes can impose inspection timelines and paperwork that add to lead time unpredictability; our report contains a compliance checklist tailored to corporate procurement teams.

Public-sector supply programs: National programs supplying isotope products for research and strategic applications influence commercial allocations and R&D supply access. Corporates should include public‑program engagement in their stakeholder and sourcing strategies.

Start supplier engagements now: Early technical audits, sample qualification phases, and parallel negotiating tracks with two or more suppliers reduce allocation risk and shorten time to production.

Lock in technical acceptance criteria: Define enrichment, impurity ceilings, material form, and conversion responsibilities in SOWs and acceptance tests before committing capital to process changes.

Model supply shocks: Use our scenario tools to simulate shipment delays and purity shortfalls; hold contingency inventories aligned with product launch criticality.

Invest in conversion capabilities smartly: For companies with sustained demand, evaluate captive conversion versus long‑term tolling agreements — both paths have tradeoffs covered in our cost and time‑to‑production analysis.

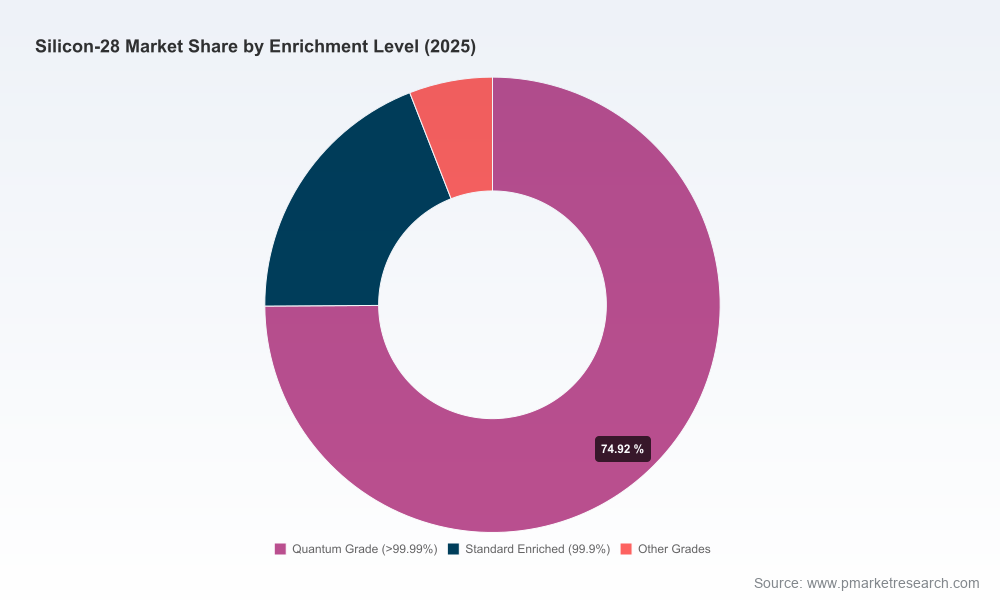

Consistent with the “trailer” approach of this market briefing, we have deliberately omitted granular regional percentage breakdowns, application‑level market shares, and tabled contract values to preserve the commercial integrity of suppliers and to ensure readers visit the full report for detailed procurement intelligence. The full Silicon 28 Market report contains those region- and application-level segmentations, supplier capacity tables, price forecasts by material form, and downloadable procurement templates.

CTOs and head of product for companies developing quantum processors or thermal‑management devices where isotopic composition impacts device physics.

Head of procurement and supply‑chain leaders planning secure sourcing and inventory strategies for 2026–2028 production ramps.

Investment and corporate development teams evaluating supplier partnerships, M&A targets, or joint‑venture structures in stable isotope and semiconductor materials.

For organizations that need to operationalize 2026 decisions, the Silicon 28 Market report delivers the full data tables, supplier scorecards, contractual templates, and scenario models necessary to act with confidence. To access the complete research, supporting datasets, and interactive modeling tools, please consult the Silicon 28 Market page on PW Consulting’s website or contact your PW Consulting account lead for an executive briefing.

PW Consulting will also be hosting a webinar series in Q2 2026 that walks through the report’s scenario models and procurement playbooks; registration details are available through our client portal.

The window for securing advantaged positions in the Silicon‑28 supply chain is narrow. Between supplier capacity expansion, nascent commercial contracts, and evolving regulatory overlays, companies that translate market intelligence into binding procurement and qualification programs in 2026 will materially reduce launch risk and capture the first‑mover technical benefits. PW Consulting’s Silicon 28 Market report is designed to be the operational guide for making those high‑stakes decisions.

For detailed analysis of this topic, please visit the official page:Silicon 28 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com